Bridgewater Associates, the world's largest hedge fund with $150 billion in assets, is planning to invest in crypto assets for the first time, CoinDesk reported on Tuesday, citing its sources. Two insiders told the media that Ray Dalio’s company is considering backing an external vehicle that is linked to the price of Bitcoin, while another source said Bridgewater Associates has no current intention of directly investing in crypto assets. Bitcoin broke through the $42,000 mark on the news, with the price of the top digital currency surging over 4% to $42,864 as of 12:22 GMT on Tuesday.

A Bridgewater spokesperson told CoinDesk in February the firm “continues to actively research crypto but is not currently planning on investing in crypto.” The statement came despite four people saying the hedge fund giant was due to enter the space by mid-2022.

0 Comments

The White House will unveil a comprehensive set of regulations targeting cryptocurrency on Wednesday, President Joe Biden has revealed. The president called it “the first ever whole-of-government approach to addressing the risks and harnessing the potential benefits of digital assets and their underlying technology.” Among other measures, the order includes a 180-day deadline for several reports on “the future of money” – presumably referring to digital currencies like the one his administration has asked the Fed to step up its research and development of. For now, around 100 other countries are also working on so-called central bank digital currencies (CBDCs).

There is “significant momentum” behind the idea of a CBDC, which is essentially a cryptocurrency without the privacy implied by the term “crypto,” controlled by (and accessible by) the Fed, according to a source who spoke to Reuters about the matter earlier this week before the White House’s statement was made public. The language used in the announcement – which carefully avoids discussing ‘cryptocurrencies’ as such, preferring the vaguer blanket term “digital assets” – is unlikely to have any immediate effect on how crypto is regulated in the US, the administration claims. Instead, the order directs agencies like the Treasury Department and the Securities and Exchange Commission to “assess risks and opportunities involved in cryptocurrency use” and issue regulations from there. The administration hopes to have all government agencies on the same page regarding how they handle crypto and other digital assets both legal and otherwise. The aim of the new policy, Biden’s office said, is to keep the US in the centre of both technology and the global financial system. The US’ dollar hegemony has wobbled in recent years as the national debt and inflation skyrocket and other countries worry about being tied to an ever-shrinking ‘reserve currency’ whose orbit they can’t leave. As the price of gas soars due to sanctions on Russian energy imports, the petrodollar alliance that has held since the US left the gold standard in the 1970s appears more fragile than ever.  Virtual chain restaurant provider Rocket Kitchens has unveiled the first Dogecoin-inspired cryptocurrency burger joint in Dubai. The restaurant named Doge Burger will also allow payments through Bitcoin, Ethereum, BNB, CRO, XRP, USDT, and Shiba Inu, local outlet Time Out Dubai reports. On the menu, the restaurant will offer a beef burger, chicken burger, mushroom Swiss burger, a char cheese, and garden burger alongside hot dogs. Customers can place orders through the restaurant’s website, where the cost of the burgers will range from Dhs35 to Dhs50. According to the founders, the initial capital used to open the restaurant is from profits emanating from early Dogecoin investments. The restaurant seeks to capitalize on the growing shift towards cryptocurrency payments across the United Arab Emirates. Notably, businesses have been accepting crypto payments in UAE as early as 2014, and more operators have been setting up shop in the region, launching various crypto-related products.

DOGE records more adoption The launch of Doge Burger highlights the impact of DOGE’s meteoric rise in value over the past year. Although the token was criticized for lacking utility, DOGE as a payment mode is likely to drive more adoption. As reported by Finbold, Tesla (NASDAQ: TSLA) CEO and crypto proponent Elon Musk revealed the electric vehicle manufacturer will start accepting DOGE payments for its merchandise. Notably, Musk has stated that DOGE has better qualities than Bitcoin. Following the rise in value witnessed in 2021, most countries are warming up to DOGE, mainly inspired by the prospects of embarking on another bull run in the near future. In this line, the United States emerged as the most pro-Dogecoin nation globally as of 2021, with 31.6% of cryptocurrency owners in the U.S. holding the meme cryptocurrency. Australia emerged second at 29%, followed by Norway at 27.4%. DOGE’s price By press time, DOGE was trading at $0.13, dropping by almost 10% over the last seven days. The tokens have experienced widespread market volatility that has accelerated in 2022. Despite the correction, DOGE continues to attract interest within the crypto community, with investors looking for the token’s next all-time high. Following developments like increased utilization as a payment option, DOGE might hit the $0.5 mark by the end of 2022.  According to a report published by German cryptocurrency media outlet BTC-ECHO, the European Parliament, one of the legislative branches of the European Union, has moved to ban Bitcoin and other proof-of-work (PoW) cryptocurrencies. The final draft of the Markets in Crypto-Assets (MiCA) framework, the much-anticipated package of cryptocurrency regulations, includes a provision forbidding the “environmentally unsustainable” consensus mechanism. This means that Bitcoin could become illegal within the European Union starting from Jan. 1, 2025. Businesses would be prohibited from offering any services associated with proof-of-work cryptocurrencies.

Stefan Berger, the center-right rapporteur behind the framework, told the outlet that the proposal was “very likely” to be greenlit. It was pushed by centre-left Social Democrats, the Greens and the Left Party. Some Christian Democrats and right-wing conservatives opposed the addition of the Bitcoin ban, but it was a deal-breaker for the parties that supported cracking down on proof-of-work. The European Commission, the executive branch of the European Union, will be engaging in a trialogue with the member states and the Parliament before reaching a final decision later this year. Patrick Hansen, head of growth and strategy at decentralized finance start-up Unstoppable Finance, described the proposal as “suicidal,” predicting that it would kill the entire crypto industry in the EU.  The government and central bank in Russia have reached an agreement on how to regulate cryptocurrencies, according to a Tuesday announcement. Russia’s government and central bank are now working on a draft law that will define crypto as an “analogue of currencies” rather than digital financial assets set to be launched on Feb. 18. Cryptocurrencies would function in the legal industry only if they have complete identification through the banking system or licensed intermediaries.

Kommersant noted that Bitcoin (BTC) transactions and possession of cryptocurrency in the Russian Federation are not prohibited; however, they must be done through a “digital currency exchange organizer” (a bank) or a peer-to-peer exchange licensed in the country. The report also highlights that cryptocurrency transactions of more than 600,000 rubles (roughly $8,000) would have to be declared; otherwise, it could be considered a criminal act. Those who illegally accept cryptocurrencies as payment will incur fines. This news comes after months of speculation about how the Russian government will handle digital currencies. While it is still unclear what this decision will mean for businesses and citizens in Russia, it seems that the country is slowly warming up to the idea of cryptocurrencies. In January, the Bank of Russia called for a nationwide crypto ban in a report that warned about the speculative nature of the industry. The bank also stated that financial firms should not facilitate crypto transactions as part of that proposal to ban digital assets. However, the proposal generated opposition from the Russian Ministry of Finance. A few days after the central bank’s call for a ban, Ivan Chebeskov, a ministry official, said that the government should regulate crypto rather than prohibiting it entirely. He warned that a total ban might result in Russia falling behind in technology. Reports have also emerged that President Vladimir Putin supports efforts to regulate the country’s crypto mining sector.  For a long time, China has been the promised land for bitcoin miners and much of the network's hashing power has been on Chinese soil. However, this year the Chinese government has launched a manhunt for bitcoin miners and the industry has almost completely disappeared from the country. In recent days, the story suddenly came out that China is considering revising and possibly lifting the ban on bitcoin mining. However, if we look at the source in question, none of that seems to be true. The National Commission for Reform and Development (NCHO) has published a notice that does not say anything about lifting the ban on bitcoin mining. The only thing in the notice regarding bitcoin mining is that the NCHO plans to add “crypto mining” to the list of undesirable industries.

List should help entrepreneurs in the country The idea of the list of undesirable industries is to give entrepreneurs insight into the policies of the Chinese government. So, “Crypto mining” is now likely to be on this list as an industry that the government intends to eliminate. That at least gives entrepreneurs the information they need to determine whether it's a good idea to invest in the industry in question. Contrary to what we heard in the media, China does not seem to be considering lifting the ban on bitcoin mining at all. It is purely about adding “crypto mining” to the list of undesirable industries. The NCHO has given the public until November 21 to respond to the plans. Interestingly, the NCHO has already tried the same with regard to “crypto mining” in 2019 and that it failed to get the industry on the list at the time due to the reluctant mining sector. Now that it has almost completely disappeared from China, it seems unlikely that there will be much opposition to the NCHO's plans. The public consultation on this idea therefore appears to be a formality. Biggest geopolitical blunder of the 21st century Contrary to what we have been able to read in the media in recent days, the ban on bitcoin mining in China does not seem to be up for discussion at all. With which the country can easily write the biggest political blunder of the 21st century. Bitcoin continues to grow and the mining industry is more profitable than ever. If bitcoin is indeed the money of the future, then having a large part of the mining industry in your country is a huge advantage. That has been the case for years, but after the ban earlier this year, all companies with the northern sun have left and a large part has settled in the United States. If bitcoin continues to grow in the same way it has over the past twelve years, China has given the United States a huge gift. Even if China does decide to lift the ban on bitcoin mining, it remains to be seen to what extent miners will come back. Doing business in a climate where those in power can change their point of view at any time is also not attractive. It seems that China has shot itself in the foot with this.  China's central bank on Friday announced a ban on all cryptocurrency payments and services, escalating its ongoing clampdown on bitcoin and other digital coins as it moves to roll out its own virtual currency.

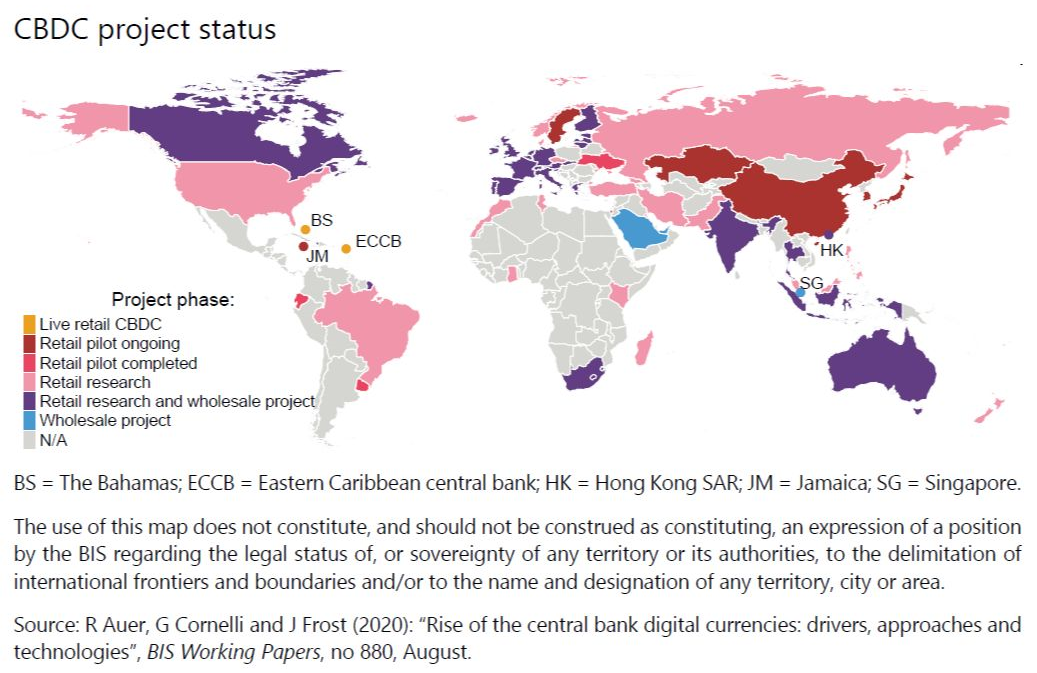

Chinese regulators' latest action "strictly prohibits" exchanging cryptocurrency for legal tender, providing information or pricing services, and trading in cryptocurrency derivatives. The measure also applies to overseas exchanges that provide services online within the country's borders. Violators will face criminal penalties. This marks Beijing's latest ratcheting up of restrictions on what it sees as a vehicle for capital flight and competition for its digital yuan, now set to roll out as early as 2022. The price of bitcoin, the world's leading virtual currency, fell by as much as 9% after the announcement to below $41,000 before paring its losses. The statement, signed by multiple authorities including the People's Bank of China, the Cyberspace Administration of China and the Supreme People's Court said virtual currencies had "disrupted the economic and financial order" and bred money laundering, illegal fundraising and fraud. Virtual currencies do not have the same legal status as legal tender, and may not be circulated in markets as currency, the document stated, naming specific examples including bitcoin and Ethereum. Takahide Kiuchi, executive economist at Nomura Research Institute and a former Bank of Japan policy board member, called the latest move an "extension" of measures to "ban all virtual currencies except central bank digital currency." China in June ordered five state-run banks including Industrial and Commercial Bank of China, Agricultural Bank of China, as well as mobile payments giant Alipay, to cut off cryptocurrency transactions. It also imposed a broad ban on virtual-currency mining that month, driving many miners overseas and slashing the country's share of digital coin creation, once above 80%. Also on Friday, the authorities announced even tougher mining restrictions, barring new operations and accelerating exits from existing projects. Supplying electricity to miners is prohibited, and such projects cannot receive financial, fiscal or tax support. The PBOC plans an official launch of the digital yuan as soon as 2022, following testing at the Winter Olympics. China plans to revise its laws to add it as legal tender and ban private-sector issuance of digital currencies, whose proliferation poses an oversight challenge for regulators. Capital flight is another factor. Cryptocurrencies have been used to circumvent Beijing's capital controls since before the coronavirus pandemic, and regulators have sought to close this loophole. The direct impact of the ban will be limited, as China's influence on virtual currency markets has diminished. But as the U.S. hammers out new regulations and other countries work toward their own digital currencies, market watchers are keeping an eye out for similar moves elsewhere. One of the most potentially far-reaching trends in the financial landscape right now is the imminent roll-out of Central Bank Digital Currencies (CBDCs), and the parallel attacks which central bankers are waging on private digital currencies and tokens as they tee up the launch of their CBDCs. First some clarifications. While the majority of central bank issued currencies (fiat currencies) in existence around the world are already in digital form, a fiat currency held in digital form is not the same as a Central Bank Digital Currency (CBDC).  What is a CBDC? A CBDC generally refers to electronic or virtual central bank (fiat) money that is created in the form of digital tokens or account balances which are digital claims on the central bank. CBDCs will be issued by central banks and will be legal tender. Many CBDCs that are being researched and developed employ Distributed Ledger Technology (DLT), with the recording of transactions on a blockchain. However unlike private cryptocurrencies which use a permissionless and open design, CBDCs that use DLT will use permissioned variants (deciding who has access to the network and who can view and update records in the ledger). Critically, as the name suggests, CBDCs will be centralized and governed by the issuing authority (i.e. a central bank). So, in their design and structure, CBDCs can be viewed as the very antithesis to decentralized private cryptocurrencies and tokens. Central banks have already working on two types of CBDCs, ‘wholesale’ digital tokens that would have access restricted to banks and financial entities to be used for activities like interbank payments and wholesale market transactions, and ‘general purpose’ (retail) CBDC for the general public to be used in retail transactions. It is this ‘general purpose’ CBDC which most people are referring to when they discuss central bank digital currencies, and it is these ‘general purpose’ CBDCs that will be most important to watch when central banks and governments begin to attempt their roll-outs to distribute CBDCs to billions of people across the world either through account-based CBDCs or ‘digital cash’ tokens. As you can guess, account-based CBDCs will be tied to user identities and Digital IDs, and straight off the bat they allow for total surveillance by the State and torpedo any chance of anonymity. For this reason, they are already a favourite among central banks. Given that CBDCs will be centralized ledgers and can be programmable, the ‘digital cash’ token option is not much better in terms of privacy and freedom. Many central banks will probably opt for a hybrid model of both account-based and token based digital cash. As an example, Canada, the one time liberal democracy, perhaps illustrates the account-based vs token based choices best, where Canada’s central bank, the Bank of Canada, in it’s design documentation for CBDCs shows that at the end of the day, it’s about surveillance and control, saying that : “anonymous token-based options would be allowable for smaller payments, while account-based access would be required for larger purchases.” Accelerating rollout CBDCs are not just a buzzword or a hazy innovation that may appear sometime in the distant future. They are actively being developed now, and in widespread fashion. In January 2020, the Bank for International Settlements (BIS) issued the result of a survey on CBDC's that it had conducted in the second half of 2019, and to which 66 central banks had responded. Strikingly, 10% of central bank respondents (which represented a fifth of the world’s population) said that they were likely to issue a ‘general purpose’ CBDC (for the general public) in the near future (within the next 3 years). Another 20% of central bank respondents said they would likely issue a ‘general purpose’ CBDC in the medium term (within 6 years). In August 2020, the BIS published a comprehensive working paper on CBDCs titled “Rise the central bank digital currencies drivers, approaches and technologies" one part of which analysed the BIS database of central banker speeches and found that between December 2013 and May 2020, there had been 138 central banker speeches mentioning CBDCs, with a dramatic increase in CBDC related speeches since 2016, a timeframe which coincided with central banks launching research projects on CBDCs. The same BIS report also highlighted that, (totally coincidentally) the Covid-19 ‘pandemic’ “accelerated work on CBDCs in some jurisdictions."   The central banks of Australia, Singapore, Malaysia and South Africa have announced a joint initiative to trial international settlements using central bank digital currencies (CBDC). The initiative, dubbed Project Dunbar, will prototype shared platforms enabling direct transfers between institutions using digital currencies issued by multiple central banks. The pilot’s findings will be used to inform the “development of global and regional platforms” in addition to supporting the G20’s roadmap for improving cross-border payments. Project Dunbar will be carried out in partnership with the Bank for International Settlements (BIS) Innovation Hub from its Singapore Center. The project will engage multiple partners to develop different distributed ledger technology (DLT) platforms and explore different designs that would enable central banks to share CBDC infrastructure. A joint announcement emphasizes the efficiency savings associated with DLT-based payments, stating: “These multi-CBDC platforms will allow financial institutions to transact directly with each other in the digital currencies issued by participating central banks, eliminating the need for intermediaries and cutting the time and cost of transactions.” Michele Bullock, assistant governor of the Reserve Bank of Australia (RBA), highlighted that “enhancing cross-border payments has become a priority for the international regulatory community,” adding that the RBA is “very focused” on the matter in its domestic policy work. “Project Dunbar brings together central banks with years of experience and unique perspectives in CBDC projects and ecosystem partners at advanced stages of technical development on digital currencies,” said Andre McCormack, head of the BIS Innovation Hub Singapore Centre. He added: “With this group of capable and passionate partners, we are confident that our work on multi-CBDCs for international settlements will break new ground in this next stage of CBDC experimentation and lay the foundation for global payments connectivity.” The RBA has consistently downplayed the need for a domestic CBDC, however, citing the success of the New Payments Platform, which allows instant digital transfers 24-hours a day.

The European Commission is considering a new registry to register all citizens' possessions. This should not only include properties in the form of real estate, land and shares, but also assets such as precious metals, cryptocurrencies, jewelry, works of art, cars and boats. This is evident from a new document entitled 'Feasibility Study for a European asset registry'. According to the European Commission, such a register is necessary to prevent tax evasion and money laundering. It provides the authorities with more information to map out money flows. From the text of the proposal: "Data collection and interconnection of registers is an important tool under EU law to speed up competent authorities' access to financial information and facilitate cross-border cooperation. Several possibilities researched to collect information with a view to establishing an asset register that can then be used for a future policy initiative. It will examine how to analyze information from different sources on asset ownership (e.g. land registers, company registers, trust and foundation registers, central securities depositories, etc.) and how the design, scope and challenges of such an asset register of the Union can look like. It will also be examined whether data on the ownership of other assets, such as cryptocurrencies, works of art, real estate and gold, can be included in the register." Financial repression Although this is only a proposal, this is a very worrying development. It gives governments even more insight into the wealth of citizens, on top of the information they already collect. It is striking that the proposal only focuses on the interests of governments, supervisors, banks and NGOs and does not take into account the interests of European citizens. The proposal also does not clarify why a more detailed registration of assets is necessary. Under the guise of money laundering and terrorism, such a register further affects the freedom and privacy of citizens. Governments use it as an excuse to exercise more control over their own population. The proposal is therefore strongly criticized from various quarters. According to the German politician Markus Ferber, the European Commission is passing its book. "These plans are completely disproportionate. The relationship between the citizen and the state reminds me of China, not EU member states, when these kinds of plans are made." Control State The German newspaper Die Welt concludes that with this register all assets of gold and bitcoins become traceable, while the Austrian newspaper Die Presse reminds of a chapter from Orwell 1984. According to the Austrian Kroner Zeitung, such a registration of assets is impracticable in practice. and also very expensive. According to the German magazine Focus, the EU wants to map the wealth of all people down to the last cent: "If this register were established, the consequences are obvious. For example, for politically unwelcome citizens - and not only criminals - it will be much more difficult in the future to continue their activities. investigative journalists or whistleblowers, who are threatened with more targeted reprisals. Controlling money flows, investments and assets is contrary to human dignity. Under the guise of preventing money laundering, we are all being vetted. Now is the time for civil disobedience. People have to take to the streets, like the yellow vests in France." Capability mapping is the next step in tightening control over citizens. Earlier, the European Commission advocated stricter supervision of cryptocurrencies. She wants to register all crypto addresses, so that anonymous transactions come to an end. The European Commission also issued a directive this summer to ban transactions over €10,000 in cash across the European Union. A worrying development, even for savers who have nothing to hide.

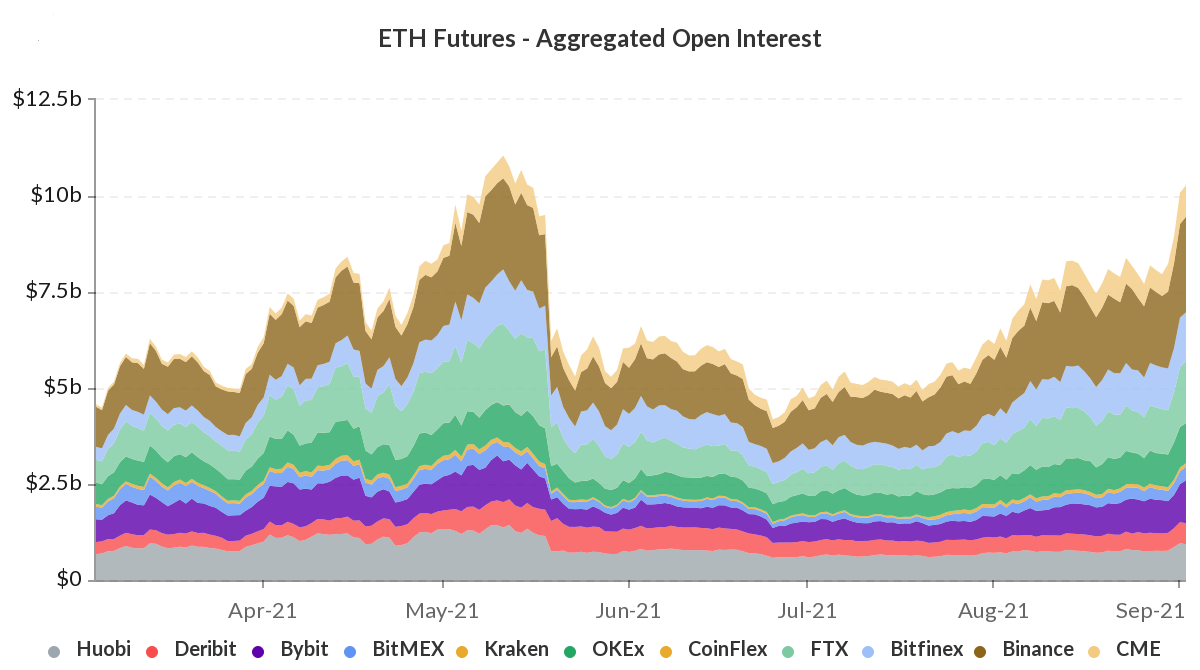

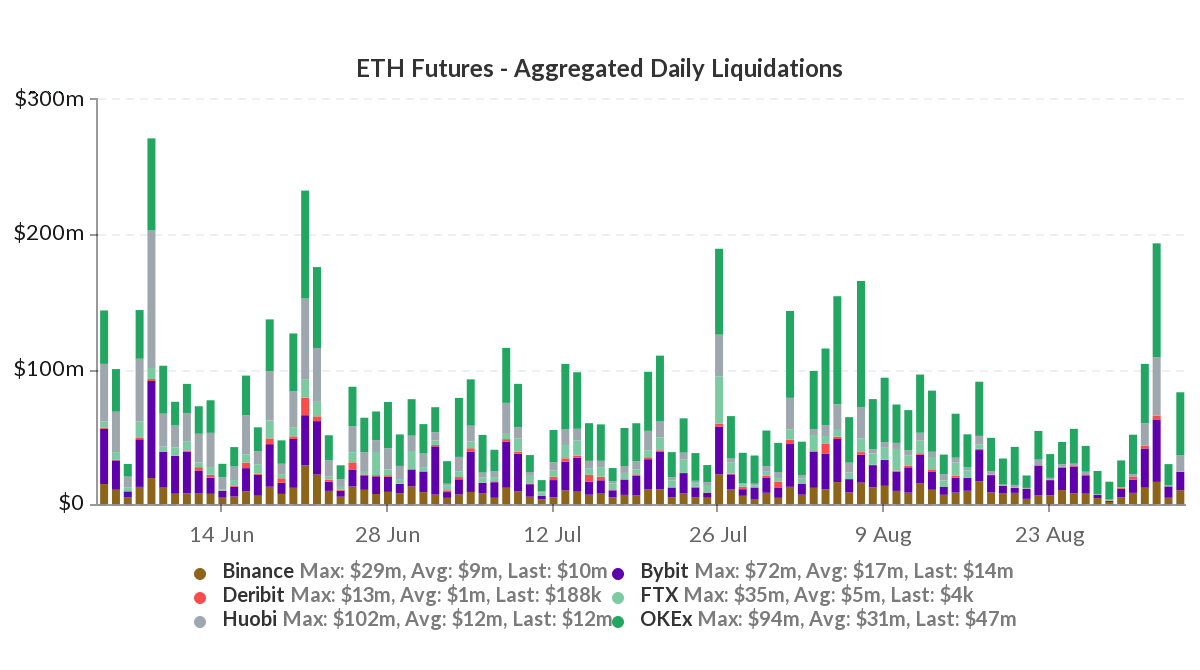

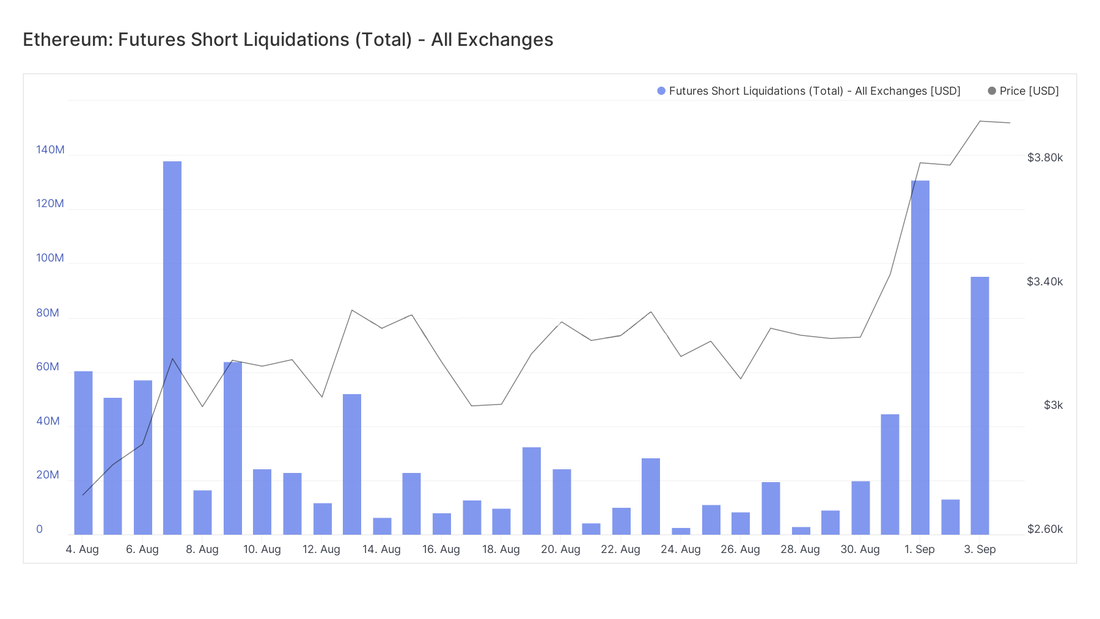

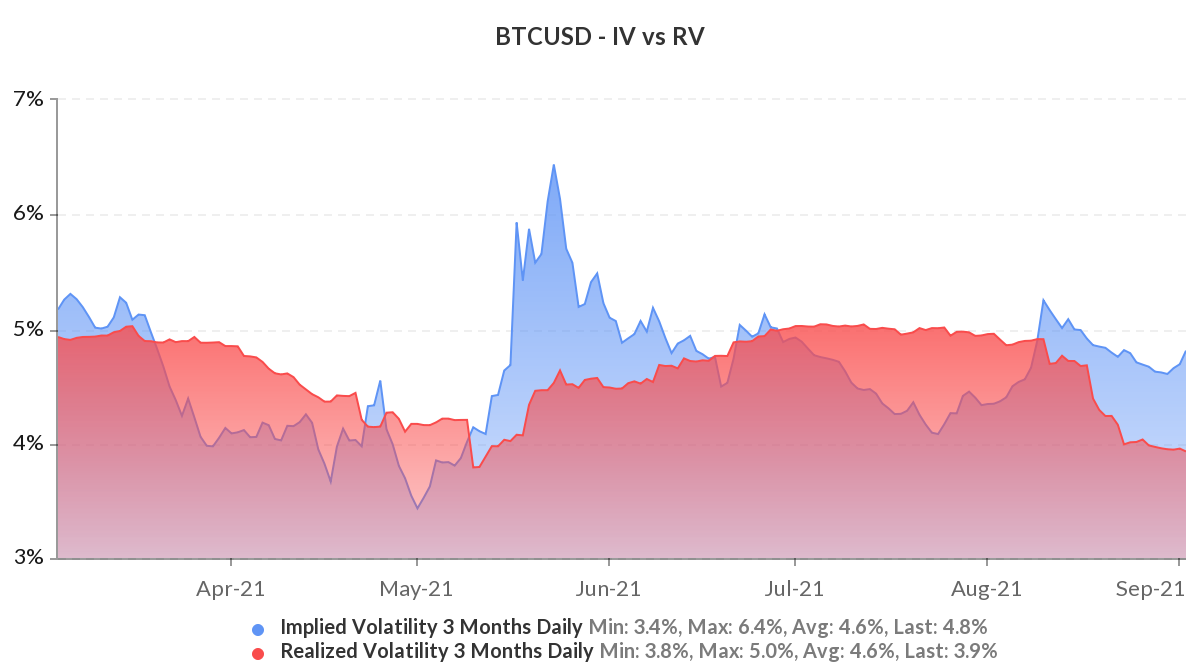

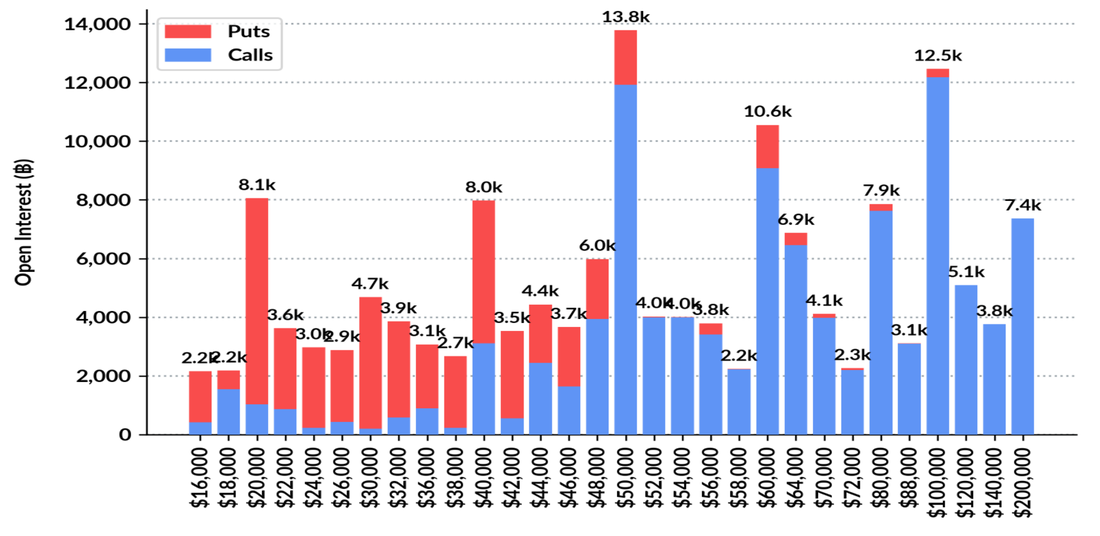

Bitcoin and Ethereum accumulation continues in the spot market as the focus now shifts towards the derivatives market. Here, some interesting observations can be made, each of which shows us how Futures and Options have been affecting the spot market. And vice-versa. Those looking for profits in Bitcoin and Ethereum might find the derivatives market as an alluring opportunity. How does the market look? At the moment, the market is at its best in a long time. Both Bitcoin and Ethereum investors are in a solid spot as the Open Interest [OI] hit new highs today. Futures OI for BTC seemed to be at a 4-month high of $17 billion. The same was the case for ETH, with the OI standing at $14 billion.  That being said, it’s worth noting that the ETH market is in a much different position than the BTC market, varying in many ways. ETH market has been hyper bullish Volumes on 31 August and 1 September were almost close to Bitcoin’s levels of $41 billion. These volumes aren’t usual for ETH as the same mostly remain within the range of $30 billion. Plus, over the same time frame, when ETH volumes were close to BTC’s, daily liquidations touched a 3-month high of $194 million.  However, if you take a closer look, you’ll observe that most of these liquidations came from short contracts. Short liquidations for Ethereum rose to a monthly high of $130 million. This transpired primarily because of ETH’s rally over the last 2 days, a period during which ETH went up by 18.81%. Right now, people are demanding stability from Ethereum’s market.  BTC market has been steadily bullish At the time of this report, daily volumes were still within the normal range of $100 million. Bitcoin OI in Perpetual Futures contracts also hit an 18-month high of $14.157 billion. These are good figures for a market that has been bullish for over a month now. Even the Implied Volatility to Realized Volatility spread seemed to be at its highest level of 0.9%, a level last seen on 30 May.  A huge reason behind this is because the BTC spot market has been rising gradually, with a hike of “just” 4.83% in the last 4 days. Plus, with Bitcoin crossing $50k again, the OI by Strike’s 12k Call contracts for $50k seems to be turning profitable as the 24 September expiry inches closer.  All in all, the derivatives market is in a really profitable state right now.

The Chinese Government has introduced a new rule that will allow minors to play online games for an hour on Friday, Saturday, Sunday and public holidays between 8 PM and 9 PM. It is also working with game developers, teachers and parents to educate children about the ill effects of gaming addiction. After cracking down on cryptocurrency mining operations located within its borders, the Chinese Government's ire is now directed towards gamers in China. Not too long ago, Tencent cut down the number of hours minors could play its flagship Honor of Kings title. That could have been a test run for things to come because the latest regulations cut down on Chinese minors' playtime to three hours per week.

China's state-run Xinhua news agency has laid down new guidelines to be followed by all game publishers in China. For starters, minors can only play online games between 8 PM and 9 PM on Fridays, Saturdays, Sundays and certain holidays. Second, publishers have to ensure that their games ship with a robust anti-addiction mechanism in place that forbids minors from playing outside of the designated hours. Third, all publishers have to work in tandem with the state, teachers, and parents to ensure that children are educated about the ill effects of online gaming. Lastly, no user will be allowed to sign up for a service without providing their real name. Most of the rules mentioned above, including the real name requirements and anti-addiction measures, have existed for quite some time. It'll be interesting to see if these measures meaningfully affect the likes of Tencent and NetEase. Then again, adults tend to spend a lot more time and money on online games, so minors playing for fewer hours shouldn't make any meaningful impact on the revenue stream. Besides, these regulations only apply to online games, and it isn't immediately clear they will also apply to offline, single-player games. Furthermore, one can also use a VPN to bypass the restrictions altogether, but it is has been quite challenging to get a working VPN service in China of late.  The overall sentiment among cryptocurrency enthusiasts is back to “neutral” after the significant gains Bitcoin has posted in the last 12 days. Despite the renewed optimism, BTC needs to reclaim a crucial price level as support to advance further. Bitcoin Must Reclaim $40,000 Bitcoin has enjoyed an impressive 43% rally over the past two weeks, gaining over nearly 13,000 points in market value. Its price went from a low of $29,800 on Jul. 21 to hitting a high of $42,600 over the weekend. The bullish impulse was forecasted by a descending triangle pattern that developed on BTC’s daily chart. Although the technical formation projected a 40.5% advance from the breakout point at $32,600 towards the 200-day moving average at around $46,000, the $40,000 resistance zone has proven challenging to break through. The leading cryptocurrency has retraced by more than 8.6% over the last few hours, dropping below the 100-day moving average at $39,900. Now, Bitcoin must reclaim this crucial support level to continue its upward advance.  IntoTheBlock’s In/Out of the Money Around Price (IOMAP) model reveals that over 750,000 addresses have previously purchased nearly 550,000 BTC at a price of around $40,000. Such a large concentration of addresses “Out of the Money” at this level suggests that any signs of price weakness could encourage them to exit their positions to avoid further losses. Under such unique circumstances, a sell-off would likely push Bitcoin towards the next critical area of support that sits at $36,770 based on transaction history. Nonetheless, a spike in buying pressure that allows Bitcoin to reclaim $40,000 as support could lead to an upswing towards $44,000. The IOMAP model shows no critical supply walls between these price points, crediting the optimistic outlook.

Recently, the Netherlands Authority for the Financial Markets (AFM) warned investors against making decisions based on tips from financial influencers. Those influencers have become very popular, and they not only share knowledge about investing, but also about pensions, student loans and mortgages, for example. What does this advance mean for our financial well-being?

Trend watcher Farid Tabarki distinguishes two trends among financial influencers. "There is a large group that is involved in learning how to handle money properly. That makes me very enthusiastic." That is absolutely necessary, he says. For example, research by Nibud shows that 32 percent of Dutch households are dealing with payment arrears. "People who train each other financially seems to me to be a very positive development." On the other hand, there is a group of financial influencers who focus on making money, the trendwatcher explains. "Investment tips, cryptocurrency… That can be useful, but you never know for sure what someone's motives are for giving those tips. There may be revenue models behind it that are not in your favor." 'Too easy to call everything bad' Media scientist Roel Lutkenhaus can imagine that people are misled by financial influencers. "But I find it too easy to say: 'everything is bad'. There are also many people who give sincere tips. For example, I think the Young Investing podcast is very good. It falls into the category of someone who has stuck in the topic, and the podcast makes it to simply share his tactics and knowledge. I don't see any dark edges in that." But those dark edges are there. A good example of such an influencer is Madelon Vos, who, unhampered by experience and knowledge, provides her followers with one-sided information about Bitcoin in particular via her podcast every week. Week after week, her technical analyzes mislead her followers. Few can see through her chatter and seductive smile. Nor does she take any responsibility for her opinion. She never reflects on what she has said in previous episodes of her podcast. The most shocking part is that she discusses tweets from others and gives her one-sided opinion about them. Everyone wants to be successful, the behavioral scientist explains the popularity of financial influencers. "Making, getting rich, for example through crypto, is popular in youth cultures. People won't just take something from everyone, but certain financial influencers have built a strong relationship with their followers." Research by mobile broker BUX shows that one in five young people obtain investment knowledge from influencers. According to Lutkenhaus, the solution lies mainly in media literacy. "It's up to the government to make people resilient, so that they don't just fall prey to people who may not have the best intentions for their followers." Fishing out the bad apples isn't always easy. "I always tell myself: if it sounds too good to be true, it probably isn't. If people promise you golden mountains based on a few mouse clicks, it's not very credible. Don't take such influencers to seriously."  China is eyeing to further boost the technological application and industrial development of blockchain over the next decade, according to a guideline released by industrial development and cyberspace affairs authorities.

By 2025, the country aims to take the comprehensive strength of its blockchain industry to the most advanced level in the world, said a document jointly released by the Ministry of Industry and Information Technology and the Office of the Central Cyberspace Affairs Commission. The country's blockchain industry and its industrial standard system shall begin to take shape by 2025, with the blockchain technology applied to multiple economic and social fields, the document noted. In the next five years, China shall support the establishment of three to five backbone enterprises with international competitiveness, as well as a number of innovation-driven enterprises and three to five blockchain industrial clusters. By 2030, the blockchain industry shall see further expansion in both comprehensive strength and industrial scale, and deepen integration with next-generation information technologies such as big data and artificial intelligence, the document added. Currently, there are around 75,000 blockchain-related enterprises in China, according to data from corporate information provider Tianyancha. |

Thank you for choosing to make a difference through your donation. We appreciate your support.

Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed