|

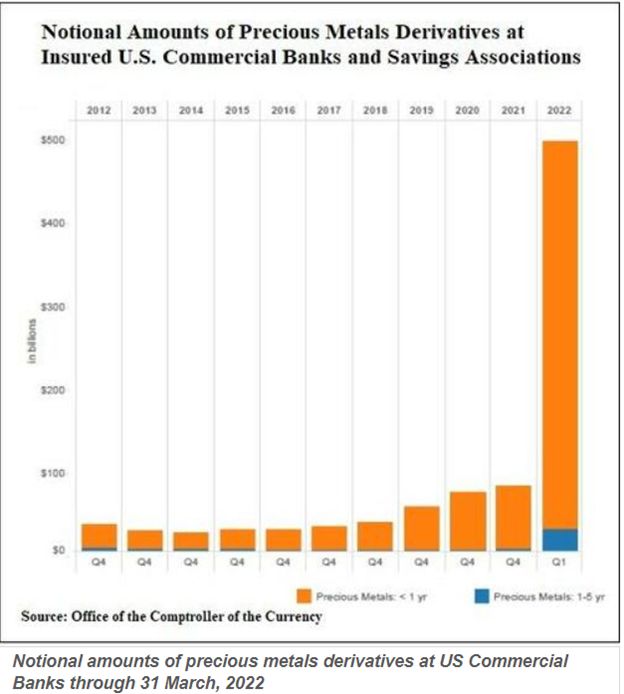

The current and open fraud regarding the paper gold price in the COMEX market is now as plain to see as the open desperation in the global financial system, which is unravelling in real-time all around us. As risk assets tumble foreseeably into bear territory before a headwind of deliberately rising rates, precious metals have seen headline-making falls as well. Tracking the Paper Gold Price —The Standard Answer In prior reports, we’ve noted that precious metals typically behave sympathetically when markets tank; thereafter, gold then surges north. We saw this pattern in October of 2008 and March of 2020. Furthermore, when a Hawkish Fed pursues a temporary yet face-saving policy of rate hiking and quantitative tightening, this makes the USD the relatively stronger horse in the global currency glue factory. And a relative rise in the USD, of course, is a headwind to gold. Explaining the Paper Gold Price —The Rigged Answer But let’s get to the real heart of the matter, namely: Legalized paper gold price manipulation (i.e., fraud) in the COMEX market, a topic we’ve addressed more than once. As we’ve openly argued for years, nothing embarrasses an otherwise discredited fiat currency like a rising gold price. As I’ve described it, rising gold prices are a middle finger to debased currencies whose declining purchasing power are the DIRECT result of the failed and drunken monetary policies (i.e., mouse-click trillions) of a central bank near you. Or as Ronan Manly more distinctly observed: “Gold to central bankers is like sun to vampires.” And that, folks, is precisely why the big banks (under the direction of the BIS) are deliberately (and if law school serves me correctly) as well as fraudulently manipulating the paper gold price. Facts vs. Manipulation In the first quarter of 2022, we saw record high purchases of ETF gold, physical gold and central bank gold. Even Goldman Sachs’ head of commodity research was targeting $2400 gold this year. Instead, the gold price has been falling as gold demand has been rising. Huh? It reminds me of 2008 when mortgages were defaulting en masse yet the ABX index for sub-prime mortgages was rising. In short, complete (and temporary) manipulations were going on behind the curtains of a few wayward banks, including Morgan Stanley. Today’s gold behavior (i.e., surreal manipulation) is no different and no less of an insult to the natural forces of supply and demand, which central bankers have attempted to destroy for well over a decade. But the jig will soon be up on these masters of open fraud and Wall Street socialism. The Paper Gold Price & The Horse’s Mouth For now, and in case you fear I’m just acting as a “gold bug” apologist, let’s go straight to the horse’s mouth and examine the confessions and facts of open price manipulation in the precious metal markets. And I swear, you really can’t make this stuff up, it’s just that obvious and distorted. In a recent article by Peter Hambro published by the British news site, Reaction, a 3rd generation gold insider (Petropavlovsk, Bank Hambros) made the open secret of paper gold price manipulation abundantly clear and incontrovertible. It’s also worth adding that Mr. Hambro’s entire career was that of an heir to a banking dynasty all too familiar with the insider machinations of the London bullion markets and London Stock Exchange. In short, when Mr. Hambro discusses gold price manipulation, it’s worth listening. A Chart Says a Trillion+ Words More importantly, and for those who prefer facts over human confessions or “gold bug whining,” the following chart from the U.S. Office of the Comptroller of the Currency (OCC) clearly reveals the extreme extent by which just a handful of highly pocketed (and central bank supported) banks like JP Morgan and Citi can use extreme turns of derivative-based leverage to short (i.e., keep a permanent boot to the neck of) the paper gold price:  That rising bar on the far right is nothing more than crime scene evidence. As Hambro remarks, a long history of media and bank supported mis-information has tried to keep a lid on the desperate attempts by just a small number of BIS minion banks like JP Morgan and Citi to effectively prevent free market price discovery on the paper gold price. Despite thousands of daily long contracts (i.e., buy orders) in the OTC forward contract markets, if just 7-8 banks wish to use massive leverage (rising bar on the right) to short the same metal, they can effectively fix the gold price via artificial manipulation of derivatives contracts, to which only a small number of banks have access. All of this open yet legalized fraud is managed by the central-banks central bank, namely the Swiss-based Bank for International Settlements. The Jig (Rig) is Up We may be a bit jaded and realistic, but that doesn’t make us naive. Gold will get the last and honest laugh over such a corrupt and dishonest “policy.” As central banks continue to lose more and more credibility, and as investors become more and more fluent in, and aware of, the absurdity of the lies that have been sold to us for years by central bankers and MMT midgets who claim that a debt crisis can be solved with more debt, which is then paid for with trillions created out thin air, the system unwinds. As the inevitable inflation crisis emerges from precisely such absurd “policies,” the central bankers can no longer blame the obvious and long-dated/repressed inflationary consequences of their drunken monetary policies on a virus or Putin. Nor can they continue to peddle the lie that inflation was merely “transitory,” a fact we made clear long before Powell confessed it was not so. Stated otherwise, more and more folks are catching on to the fraud. The math plainly shows that expanding the broad money supply (and central bank balance sheets from $6T to $36T in just over a decade) is the real cause of the inflation in your neighbourhood and the debasement in your wallet.  The First Cracks & the Last Straws

Geopolitical shifts, assassinated prime ministers, fired prime ministers, angry truck drivers, stormed capitals and Sri Lankan protestors are just the first tragic cracks in a growing social unrest driven by declining wealth and growing wealth disparity, all classic and historic symptoms and patterns of when a debt crisis leads to a political crisis, and sadly (and ultimately) more centralized controls over our markets and lives. But as even Hambro observes, eventually the last straw breaks the back of a rigged camel, and the “straws blowing in the wind are often said to presage great tempests and I believe that {the chart above] shows just such a straw.” Years of distorted, rigged and entirely reckless debt-and-print polices have made global economies and currencies weaker, not stronger. Dying Faith, Rising Gold After years of profligate central bank policies, the so-called “developed economies,” which are now little more than glorified banana republics, are losing credibility, options and most importantly public faith. This is critical. In the end, when faith in a system ends, so does its currency. We’ve written before how impossible it is to market time “the end of faith,” but charts like the one featured herein help to point out the rigging and hence accelerate the inevitable end to derivatives-based fraud, centralized price-fixing and, eventually, the OTC casino in particular. Meanwhile, the current buy window for repressed precious metals is remarkable, and once central banks cripple the markets to their deflationary pain points, chaos will return, along with the inflationary money printers—all of which will send precious metals higher and fiat currencies and markets to their mean-reverting lows. Thanks to Matthew Piepenburg

0 Comments

Like anything in the central bank gold world, there is no transparency into the claimed gold of any of these central banks nor any independent physical audits of the gold bars they claim to hold, so when talking about relative rankings, we will just have to go with the figures of the IMF / World Gold Council. Just Outside Lisbon The Banco de Portugal maintains that just over 45% of its total gold reserves, or 127.6 tonnes (5,549,238 ozs), is held in the form of gold bars in its vault in Carregado, and it was these gold bars which the Portuguese reporters and photographers were briefly shown in what the Reuters report about the visit called a ‘Rare Glimpse'. But apart from Reuters, a whole host of Portuguese media seemed to be present for the tour of the vault, judging by the extensive coverage this gold vault ‘tour’ received in the Portuguese media. So it is these reports of the Portuguese media which we turn to get more details about the Carregado vault and what the media saw. And since there were photographers present, quite a few photographs of the gold were taken, a selection of which are included below.  Heavy security and guard dogs near the entrance to the Garregado compound The Banco de Portugal’s Carregado Complex is a 67,000 square metre compound in an industrial part of the town which is surrounded by high walls and barbed wire, and which is guarded by machine gun toting members of Portugal’s National Republican Guard, and their four-legged friends, German Shepherds. As well as the gold vault, this Carregado Complex, built in 1995, is where the Portuguese central bank prints Euro banknotes, so there are said to be more than 200 bank employees working in this operational centre. Apart from the 172.6 tonnes (45%) of Portuguese gold in the Carregado vault near Lisbon, the Banco de Portugal maintains that another 186.4 tonnes (48.7%) of its gold is stored in the Bank of England in London, with an additional 20 tonnes (5.2%) stored with the Bank for International Settlements (BIS), and the remaining 3.7% tonnes (1%) now stored at the Banque de France in Paris after having been moved in 2021 from the vault of the Federal Reserve Bank of New York (FRBNY). So overall, the split is 45% of Portugal’s gold is supposedly stored in Portugal, with the remaining 55% stored abroad.  Vault door in the Banco de Portugal’s Carregado Comple  In the last few weeks we’ve seen most gold and silver dealers with ‘out of stock’ signs on their storefront. That’s what the vast majority of silver bullion consumers have been getting since the end of January. Stories have been surfacing online about Silver bullion dealers seeing a rise in demand, one of the biggest they’ve seen in their lifetime. Everyone is buying, and no one is selling the physical metal in the United States. Bullion Dealers are requesting 35% premiums…and that’s if you can get your hands on some.

And yet less than a year ago when pandemic took the world by it’s grip, Gold or silver bullion dealers were nearly completely sold out within a matter of days. In some cases silver premiums reached historic highs, near 100% of spot prices. With the inception of the new #silversqueeze hype inspired by an army of retail investors on Reddit, silver has traded at an 8-year high, as demand was exploding. Silver’s given back $2 since its $29 peak on Feb. 1. But it’s still up 20% since late November, and has gained 125% since its March lows according to Kitco news. To add to that, silver stocks in the United states have been surging. It’s all related to the now infamous WallStreetBets calls to action, the latest of which targeted silver. It was enough to cause Comex to raise silver margins by 18% after just two up days. But silver’s story is still in its early days. Dramatically higher silver prices are still squarely ahead. The silver market has been largely under-owned and underinvested until 2020, when silver began its bull rally and outperformed gold. According to John Feeney from Guardian Vaults: Silver is looking more and more like the metal of the future and a substantial investment for 2021. The big driver that is here to stay is a global move into renewable energy, he said. "Under the Biden administration, we will see a lot of money getting moved into solar panel production. That is happening globally too. If you look at the solar market, the outlook for the next 5-10 years is very bullish for silver." Also, there is an argument to be made for the start of the commodity supercycle. "A lot of analysts think that we are at the beginning of it. There has been a lot of underinvestment in commodities over the last few years. A lot of capital moved into the tech sector and hardly any capital in comparison moved into the commodities sector," Feeney said. Gold and silver as a whole are considered safe haven assets - an investment that’s expected to hold their value during market turbulence. However people are often skeptical about whether to invest in gold or silver! They often think of investing in these metals as a long term yet reliable opportunity. So today we're going to break down in depth: how much gold and silver will be worth if the U.S Dollar collapses? Is it wise to invest in gold and silver or are there other options? Considering gold and Silver is considered are considered safe haven assets as we’ve mentioned above, that makes it a likely choice for investors during political and economic upheavals because they have intrinsic value, carry no credit risk, and cannot be inflated. That’s why either gold or silver, investing in precious metals is one of the best types of investments you can make in 2021. Owning just a small percentage of precious metals diversifies your portfolio, and therefore reduces volatility and risks. It can also protect your future buying power. Even in today’s cryptocurrency dominated world of investing, gold and silver hold a prominent place in the stock market. To briefly summarize this article, I firmly believe silver and gold both are good resources for future investments and something you should own even when the U.S dollar collapses.  The head of China’s central bank is calling for countries to replace the U.S. dollar as an international reserve currency with something called SDRs. Created by the IMF way back in 1969 for that purpose, SDRs never caught on. While SDRs may be declared an official international reserve asset today, they are not likely to become the world’s key international currency anytime soon. In the meantime, countries in China’s current predicament—acquiring more dollars than they think prudent—could avoid such risks in the future by allowing their currencies to appreciate.

Yi Gang, governor of the Bank of China, wants a new international reserve currency, one that is “disconnected from economic conditions and sovereign interests of any single country.” He claims that credit-based national reserve currencies, like the dollar, are inherently risky, facilitate global imbalances, and foster the spread of financial crises, but China’s concerns may also be a bit more parochial. The country holds a huge portfolio of dollar-denominated assets that could incur valuation losses, if recent U.S. actions to limit financial turmoil and stimulate the economy generate inflation and dollar depreciation. The People’s Bank of China has offered a fix to the dollar problem. They recommend supplanting the reserve-currency role of the U.S. dollar with Special Drawing Rights (SDRs), a composite currency issued by the International Monetary Fund (IMF). Others, including Nobel Prize winner Joseph Stiglitz and a U.N. panel of experts, have endorsed the idea. Adopting the SDR as an official international reserve asset may be technically feasible and it could conceivably occur fairly quickly, but substituting the SDR for the dollar more broadly as the world’s key international currency will not happen anytime soon. People reap substantial economies from conducting cross-border commerce in dollars, and until the SDR matches these benefits, central banks will still need dollars. In the interim, countries that want to limit their exposure to credit-based reserve currencies, like the dollar, might simply allow their currencies to appreciate. Something Old, Something New Complaints about the dollar and a fascination with SDRs are not new. The IMF created SDRs as an international reserve currency in the late 1960s to solve problems, similar to Dr. Zhou’s concerns, which rose out of the Bretton Woods fixed-exchange-rate system. Although Bretton Woods was at its heart a gold-based currency arrangement, the U.S. dollar quickly emerged as the key international currency, both for financing international commerce and as an official reserve currency. Today, as during Bretton Woods, countries accumulate foreign exchange when they prevent or limit the appreciation of their currencies in the face of persistent trade surpluses and foreign financial inflows. Once acquired, official reserves then provide these countries with a buffer stock that they can draw down to mitigate the disruptive economic effects of unexpected trade shortfalls and temporary outflows of foreign funds. Absent such reserves, these countries would either have to allow their currencies to depreciate or quickly tighten their monetary policies, but such abrupt adjustments could be disruptive and might not be compatible with these countries’ current goals for inflation or real economic growth. At its heart, the desire to acquire and hold official foreign-exchange reserves reflects a desire to prevent, or at least limit, exchange-rate adjustments. About 15 years into the Bretton Woods era—just like today—many countries began to view their holdings of official U.S. dollar reserves as excessive, and they worried that the United States might be forced to devalue the dollar. A dollar devaluation would saddle these countries with foreign exchange losses, since a devalued dollar would buy less abroad. As the situation unfolded, some countries, led by France, sought to replace the dollar with a reserve currency unrelated to a single national currency, if not solely related to gold. The IMF—then the guardian of the Bretton Woods parity grid—came up with the SDR. The IMF initially defined the SDR in terms of a fixed amount of gold, then equal to one dollar, and allocated 9.3 billion SDRs between 1970 and 1972 to member countries in proportion to their quotas in the IMF. Before the SDRs even hit the shelf, however, President Nixon threw a wrench in the Bretton Woods works. He closed the U.S. gold window on August 15, 1971, refusing thereafter to convert dollar reserves into U.S. gold. Countries holding dollars were stuck. By March 1973, the large developed countries had all allowed their currencies to float against the dollar, ending their need to acquire dollar reserves. With the advent of floating exchange rates, the IMF redefined the SDR as a weighted average of the U.S. dollar, the British pound, the Japanese yen, and the currencies that eventually comprised the euro. The dollar has the largest weight, currently about 40 percent, so changes in the dollar impact the SDRs more than similar changes in the pound, yen, or euro. Because of its construction, however, the SDR will likely be more stable relative to other currencies than the dollar; so, holding a portfolio of SDRs is liable to present a country with less exchange-rate valuation risk than holding dollars. While many in the late 1960s and early 1970s believed that the SDR would supplant reserve currencies and possibly even gold in official portfolios, the SDR basically died at birth. The IMF made a second allocation of 21.4 billion SDRs between 1979 and 1981, again in proportion to member countries’ quotas, but the SDR quickly devolved for the most part into a unit of account, primarily on the IMF’s books, as the large developed countries accepted floating exchange rates as the norm. If countries are willing to allow their exchange rates to adjust freely to trade flows and to cross-border movements of financial funds, they do not need official foreign-exchange assets. Despite the widespread acceptance of floating exchange rates, however, no country—including the United States—has completely tossed out their portfolio of foreign-exchange reserves. They keep some around just in case they may sometimes want to support their exchange rates. In doing so, they accept that the exchange value of these reserves will fluctuate from time to time. The Dollar The reserve currency of choice is the dollar (figure 1). The IMF estimates that 64 percent of the world’s official foreign-exchange reserves are held in dollar-denominated assets. The euro, the second most widely held international reserve currency, lags well behind, followed by the British pound and Japanese yen. These currencies’ rankings as official reserves parallel their status in international commerce more generally. This correlation should be of no surprise. Why hold a currency that no one uses? |

Thank you for choosing to make a difference through your donation. We appreciate your support.

Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed