|

In what is an unbelievable and bombshell admission from a US Commodity Futures Markets regulator, the CFTC’s Acting Chairman, Rostin Behnam, was recently caught on record as acknowledging and condoning attempts by Wall Street bullion banks to put a halt to the strong rise in the silver price in early February.

The admission came in an interview of Behman in March, a clip of which can be seen here in the video. This interview was first brought to the world’s attention by Chris Marcus of Arcadia Economics. In the interview, Behman blatantly shows his true allegiance to Wall Street, saying that “the resiliency and the market structure of the futures market was able to tamp down what could have been a much worse situation in the silver market.” Much worse for who? The bullion banks and the US Government of course, none of who want the price of silver to rise. For those who don’t know, ‘tamp down’, means to drive down by succession of blows, to put a check on, to reduce. While its not surprising that Behnam will not be investigated for supporting an attack against the silver price (since the CFTC works hand in glove with protecting the interests of Wall Street banks), it is somewhat surprising that not one reporter in the mainstream financial media sees fit to cover such an important bombshell.

0 Comments

In the last few weeks we’ve seen most gold and silver dealers with ‘out of stock’ signs on their storefront. That’s what the vast majority of silver bullion consumers have been getting since the end of January. Stories have been surfacing online about Silver bullion dealers seeing a rise in demand, one of the biggest they’ve seen in their lifetime. Everyone is buying, and no one is selling the physical metal in the United States. Bullion Dealers are requesting 35% premiums…and that’s if you can get your hands on some.

And yet less than a year ago when pandemic took the world by it’s grip, Gold or silver bullion dealers were nearly completely sold out within a matter of days. In some cases silver premiums reached historic highs, near 100% of spot prices. With the inception of the new #silversqueeze hype inspired by an army of retail investors on Reddit, silver has traded at an 8-year high, as demand was exploding. Silver’s given back $2 since its $29 peak on Feb. 1. But it’s still up 20% since late November, and has gained 125% since its March lows according to Kitco news. To add to that, silver stocks in the United states have been surging. It’s all related to the now infamous WallStreetBets calls to action, the latest of which targeted silver. It was enough to cause Comex to raise silver margins by 18% after just two up days. But silver’s story is still in its early days. Dramatically higher silver prices are still squarely ahead. The silver market has been largely under-owned and underinvested until 2020, when silver began its bull rally and outperformed gold. According to John Feeney from Guardian Vaults: Silver is looking more and more like the metal of the future and a substantial investment for 2021. The big driver that is here to stay is a global move into renewable energy, he said. "Under the Biden administration, we will see a lot of money getting moved into solar panel production. That is happening globally too. If you look at the solar market, the outlook for the next 5-10 years is very bullish for silver." Also, there is an argument to be made for the start of the commodity supercycle. "A lot of analysts think that we are at the beginning of it. There has been a lot of underinvestment in commodities over the last few years. A lot of capital moved into the tech sector and hardly any capital in comparison moved into the commodities sector," Feeney said. Gold and silver as a whole are considered safe haven assets - an investment that’s expected to hold their value during market turbulence. However people are often skeptical about whether to invest in gold or silver! They often think of investing in these metals as a long term yet reliable opportunity. So today we're going to break down in depth: how much gold and silver will be worth if the U.S Dollar collapses? Is it wise to invest in gold and silver or are there other options? Considering gold and Silver is considered are considered safe haven assets as we’ve mentioned above, that makes it a likely choice for investors during political and economic upheavals because they have intrinsic value, carry no credit risk, and cannot be inflated. That’s why either gold or silver, investing in precious metals is one of the best types of investments you can make in 2021. Owning just a small percentage of precious metals diversifies your portfolio, and therefore reduces volatility and risks. It can also protect your future buying power. Even in today’s cryptocurrency dominated world of investing, gold and silver hold a prominent place in the stock market. To briefly summarize this article, I firmly believe silver and gold both are good resources for future investments and something you should own even when the U.S dollar collapses. The World Economic Forum just had their Davos Agenda 2021 meeting in January. Now The Great Reset has been something talked about in detail since the pandemic started. But are we seeing The Great Reset happening right before our eyes? I think we are starting to see the slow implementation of The World Economic Forum's Great Reset right now. It's like a chess match, nothing happens right away, many moves are made before the endgame.

The Great Reset that was proposed by the World Economic Forum is looking to forgive all the world's debt and has us live by the slogan, "You'll Own Nothing, And You Will Be Happy". Now first and foremost, we are starting to see a slow implementation of a universal basic income. It was actually what the World Economic Forum talked about and advocate for in the Davos agenda 2021 meeting that happened a few weeks back. Starting with the continual stimulus packages that we have received in the past few months to help stimulate the economy, seems like a slow inoculation into government dependency. Since we can't work where are we going to get our money from? Secondly, The Great Reset talks about how having ALL of our debts forgiven. Well who's going to buy them? The Federal Reserve? Sure, but with the sale of debt, comes the control of the debt. And whoever controls debt, controls YOU! The great reset is all about debt forgiveness but then we won't be able to own anything ever again......and we will be happy about it. I'm not completely convinced that the World Economic Forum is looking to do this for the good of the people. They literally said, "You'll Own Nothing and Be Happy" about it. Would you like to NOT own your home, car, business? I sure would like to own all of the things I've worked very hard for and I can speak on behalf of most people who own those things. Lastly, the Davos agenda 2021 got into cryptocurrency. Currently crypto is decentralized and lacks certain regulation from major regulatory bodies. That is a beautiful thing, but the World Economic Forum has already spoke about crypto in their Davos agenda 2021 meeting that happened a few weeks back. With the Great Reset, the fiat currency will crash because of the reckless printing from The Federal Reserve. So expect to see heavy regulation and government intervention with crypto.  There is a very worrying trend that has been accelerated under the veil of fear and confusion, and that trend has been drastically intensified…

The corona crisis has already taken a very high toll and caused deep damage in our societies and our economies, the extent of which is yet to become apparent. We have seen its impact on productivity, on unemployment, on social cohesion and on political division. However, there is another very worrying trend that has been accelerated under the veil of fear and confusion that the pandemic has spread. The war on cash, that was already underway for almost a decade, has been drastically intensified over the last few months. The “problem” Over the last years, and as the war on cash escalated, we’ve gotten used to hear certain arguments or “reasons” on why we should all abandon paper money and move en masse to an exclusively digital economy. These talking points have been repeated over and over, in most western economies and by countless institutional figures. “Cash is used by terrorists, money launderers and criminals” is arguably the most oft-repeated one, as it’s been widely employed in most debates about the digital transition. Just a couple of years ago, it was also used by Mario Draghi, to support the decision to scrap the 500 euro note. We didn’t get any specific information or data about how many terrorists were actually using this high-denomination note, but we do know a lot of law-abiding citizens were using it to save, as did small business owners for their operational liquidity needs. Now, however, the corona crisis has introduced a whole new direction of anti-cash rhetoric and fresh arguments in favor of a digital economy. Even in the early stages of the pandemic, when essentially nothing was concretely known about the virus itself or its transmission, the seeds of new fears were already planted by sensational media reports and fear-mongering political and institutional figures. The insidious idea that “you can catch Covid through cash” might have been prematurely spread, but it did stick in most people’s minds. This is, of course, understandable, given the extremely high levels of uncertainty and anxiety in the general public. Wanting to eliminate potential threats was a natural instinct and so was the urge to take back at least some control over our lives, after they’d been suddenly thrown into utter chaos in the wake of the global economic freeze. Another factor that concretely helped the shift away from physical cash was an entirely practical one. Given the lockdown measures and the new “social distancing” directives that were enforced all over the world, it became difficult to use cash, even if you really wanted to, or had no other means of transaction, as is the case for billions of people. With physical stores being forced to shut down and with more and more online shops offering contactless delivery (either as a choice or as a service requirement), the need for cash very quickly gave way to digital payments. For most of us, who have access to online banking, cards or other digital payment services, this introduced no real inconvenience and we probably didn’t even give it a second thought. However, for many of our fellow citizens it was a serious impediment, which in some cases blocked their access to basic goods and essential supplies. Contrary to the glowing promises of the digital economy, of financial inclusion and convenience, the fact remains that there are still millions of people who simply do not have access to this brave new world. According to figures by the World Bank, globally there are 2.5 billion people with no bank account, with a high concentration in the developing world. In the West too, however, there is a very large part of the population that is unbanked and/or has no access to digital solutions, while the elderly are also to a very large extent “locked out” of the digital economy. For all these millions of people, cash is the only way to save, to transact and to cover their basic needs. The “solution” With cash being presented not just as a danger to society and to national security, but also as a direct health hazard due to the coronavirus, the push towards digital alternatives has been massively reinforced over the last few months. Both international organizations and individual governments have actively participated and encouraged this push, some through public guidance statements and others through the blunt enforcement of direct rules and measures that leave no real room for their citizens to make their own choices. The CDC in its official guidance to retail workers recommenced that they “encourage customers to use touchless payment options”, while a report by the Word Bank highlighted the need to adopt cashless payments for the sake of “social protection”. The UAE Central Bank encouraged the use of online banking and digital payments “as a measure to protect the health and safety of UAE residents”, and the Bank of England has acknowledged that banknotes can hold “bacteria and viruses” and recommended that people wash their hands after handling money. In March, a report from Reuters revealed that the U.S. Federal Reserve was quarantining dollars that it repatriated from Asia and so did South Korea’s central bank, while banks in China were forced by the government to disinfect bills and keep them in a safe for up to 14 days, before putting them in circulation. A highlight, however, came in May, when the World Economic Forum published an article in its “Global Agenda” strongly supporting the mass adoption of digital payments, for the sake of public health. In it, the authors argue that “contactless digital payments at the point of sale, such as facial recognition, Quick Response (QR) codes or near-field communications (NFC), can make it less likely for the virus to spread to others through cash exchanges.” They also applauded the efforts of China in digitalizing payments and appeared to hold the country and its measures as a model to be emulated: “China’s path to enabling digital payments should provide some lessons to other countries eager to follow suit.” Since a number of Western governments may indeed be “eager to follow suit”, let us take a closer look at this bright example and examine what it really entails. Fiat money 2.0 The digitalization drive in all aspects of the Chinese state, society and economy is nothing new and it certainly predated the emergence of Covid-19. The country’s infamous “social rating system” has made headlines years ago and the government’s eagerness to use technology, the internet and all sorts of digital systems to track its citizens’ behaviors and affiliations has long attracted International criticism and widespread condemnation by human rights organizations, privacy advocates and free speech supporters. Now, however, the state has been given a reason to accelerate its efforts in the mass adoption of digital payments and the abandonment of cash. To a large extent, this digitalization of payments task was much easier in China, as digital payments there are already very widespread in the population. More than 80% of consumers already used mobile payments in 2019, according to management consultancy Bain, a sharp contrast with the US that had adoption rates of less than 10%. So, as the population has already accepted a new way of payment, the new initiative sought to dominate the means of payment too. Thus, a new “digital yuan” was introduced. This new fiat currency, that has been in development for over 5 years, was rolled out in April in four Chinese cities with a plan for national adoption soon, so that it eventually replaces the physical legal tender. This so-called Digital Currency Electronic Payment (DCEP) will be put into circulation through China’s big four state banks and citizens will be able to receive and use it by downloading an electronic wallet application authorized by the People’s Bank of China (PBOC), which will be linked to their bank account. On the surface, it appears to work just like the old currency. It is issued and backed by the PBOC, it’s valued the same as the physical banknotes and, thanks to partnerships with Alipay and WeChat Pay, that control 80% of the country’s payment market, it will be used to get paid by anyone and to pay for anything. In fact, some public servant salaries and state subsidies are already being paid out in this new digital yuan, arriving in their intended recipients’ digital wallets. According to China’s state media People’s Daily, the new currency is meant to simplify domestic transactions and trade, but it will also facilitate and ease cross border transactions. The implication there is clear: It is yet another attempt to challenge the global dominance of the USD, after the Belt and Road initiative failed to really move the needle as the Chinese state had hoped. The strategy of spending of huge amounts of Chinese money abroad did provide some leverage over developing countries, but it didn’t come anywhere near “dethroning” the Dollar and internationalizing the Renminbi. Perhaps, this initiative will fare better, especially as it now has the “first-mover” advantage. Entering this “digital fiat” arena first is hugely important and the timing of the currency’s launch was no coincidence. The development and the rollout plan were significantly accelerated following Facebook’s announcement of the Libra, as the Chinese state wouldn’t have the private tech giant beat them to the punch. In fact, the digital yuan resembles the Libra in many ways. Most importantly, neither of them is a cryptocurrency, which is decentralized by design and allows for peer to peer transactions without the need of an intermediary or third party. In this case, the issuer is the third party and all transactions go through a very centralized system that controls and has access to all the data. In another non-coincidence just a few years back, China’s government banned initial coin offerings and placed great burdens on cryptocurrencies and crypto-investors making it very hard to operate in the country, thereby dismantling the threat of potential competition from the private sector and clearing the way for its own digital coin.  The head of China’s central bank is calling for countries to replace the U.S. dollar as an international reserve currency with something called SDRs. Created by the IMF way back in 1969 for that purpose, SDRs never caught on. While SDRs may be declared an official international reserve asset today, they are not likely to become the world’s key international currency anytime soon. In the meantime, countries in China’s current predicament—acquiring more dollars than they think prudent—could avoid such risks in the future by allowing their currencies to appreciate.

Yi Gang, governor of the Bank of China, wants a new international reserve currency, one that is “disconnected from economic conditions and sovereign interests of any single country.” He claims that credit-based national reserve currencies, like the dollar, are inherently risky, facilitate global imbalances, and foster the spread of financial crises, but China’s concerns may also be a bit more parochial. The country holds a huge portfolio of dollar-denominated assets that could incur valuation losses, if recent U.S. actions to limit financial turmoil and stimulate the economy generate inflation and dollar depreciation. The People’s Bank of China has offered a fix to the dollar problem. They recommend supplanting the reserve-currency role of the U.S. dollar with Special Drawing Rights (SDRs), a composite currency issued by the International Monetary Fund (IMF). Others, including Nobel Prize winner Joseph Stiglitz and a U.N. panel of experts, have endorsed the idea. Adopting the SDR as an official international reserve asset may be technically feasible and it could conceivably occur fairly quickly, but substituting the SDR for the dollar more broadly as the world’s key international currency will not happen anytime soon. People reap substantial economies from conducting cross-border commerce in dollars, and until the SDR matches these benefits, central banks will still need dollars. In the interim, countries that want to limit their exposure to credit-based reserve currencies, like the dollar, might simply allow their currencies to appreciate. Something Old, Something New Complaints about the dollar and a fascination with SDRs are not new. The IMF created SDRs as an international reserve currency in the late 1960s to solve problems, similar to Dr. Zhou’s concerns, which rose out of the Bretton Woods fixed-exchange-rate system. Although Bretton Woods was at its heart a gold-based currency arrangement, the U.S. dollar quickly emerged as the key international currency, both for financing international commerce and as an official reserve currency. Today, as during Bretton Woods, countries accumulate foreign exchange when they prevent or limit the appreciation of their currencies in the face of persistent trade surpluses and foreign financial inflows. Once acquired, official reserves then provide these countries with a buffer stock that they can draw down to mitigate the disruptive economic effects of unexpected trade shortfalls and temporary outflows of foreign funds. Absent such reserves, these countries would either have to allow their currencies to depreciate or quickly tighten their monetary policies, but such abrupt adjustments could be disruptive and might not be compatible with these countries’ current goals for inflation or real economic growth. At its heart, the desire to acquire and hold official foreign-exchange reserves reflects a desire to prevent, or at least limit, exchange-rate adjustments. About 15 years into the Bretton Woods era—just like today—many countries began to view their holdings of official U.S. dollar reserves as excessive, and they worried that the United States might be forced to devalue the dollar. A dollar devaluation would saddle these countries with foreign exchange losses, since a devalued dollar would buy less abroad. As the situation unfolded, some countries, led by France, sought to replace the dollar with a reserve currency unrelated to a single national currency, if not solely related to gold. The IMF—then the guardian of the Bretton Woods parity grid—came up with the SDR. The IMF initially defined the SDR in terms of a fixed amount of gold, then equal to one dollar, and allocated 9.3 billion SDRs between 1970 and 1972 to member countries in proportion to their quotas in the IMF. Before the SDRs even hit the shelf, however, President Nixon threw a wrench in the Bretton Woods works. He closed the U.S. gold window on August 15, 1971, refusing thereafter to convert dollar reserves into U.S. gold. Countries holding dollars were stuck. By March 1973, the large developed countries had all allowed their currencies to float against the dollar, ending their need to acquire dollar reserves. With the advent of floating exchange rates, the IMF redefined the SDR as a weighted average of the U.S. dollar, the British pound, the Japanese yen, and the currencies that eventually comprised the euro. The dollar has the largest weight, currently about 40 percent, so changes in the dollar impact the SDRs more than similar changes in the pound, yen, or euro. Because of its construction, however, the SDR will likely be more stable relative to other currencies than the dollar; so, holding a portfolio of SDRs is liable to present a country with less exchange-rate valuation risk than holding dollars. While many in the late 1960s and early 1970s believed that the SDR would supplant reserve currencies and possibly even gold in official portfolios, the SDR basically died at birth. The IMF made a second allocation of 21.4 billion SDRs between 1979 and 1981, again in proportion to member countries’ quotas, but the SDR quickly devolved for the most part into a unit of account, primarily on the IMF’s books, as the large developed countries accepted floating exchange rates as the norm. If countries are willing to allow their exchange rates to adjust freely to trade flows and to cross-border movements of financial funds, they do not need official foreign-exchange assets. Despite the widespread acceptance of floating exchange rates, however, no country—including the United States—has completely tossed out their portfolio of foreign-exchange reserves. They keep some around just in case they may sometimes want to support their exchange rates. In doing so, they accept that the exchange value of these reserves will fluctuate from time to time. The Dollar The reserve currency of choice is the dollar (figure 1). The IMF estimates that 64 percent of the world’s official foreign-exchange reserves are held in dollar-denominated assets. The euro, the second most widely held international reserve currency, lags well behind, followed by the British pound and Japanese yen. These currencies’ rankings as official reserves parallel their status in international commerce more generally. This correlation should be of no surprise. Why hold a currency that no one uses? The latest vault reporting data from the London Bullion Market Association (LBMA) in London, which is now released on the 5th business day of the month, claims that as of the end of March, there were 1.25 billion ozs (38,859 tonnes) of silver in the LBMA London vaults, which would be an 11% increase on the total claimed to be held in those vaults at the end of February. To put this into perspective, that’s an extra 3,863 tonnes that the LBMA claims has arrived into its vaults in London during March, or an extra 124.2 million ozs. That’s nearly as much silver claimed to be added by the LBMA during March, as the Sprott Physical Silver Trust PSLV holds. (PSLV holds 130.97 million ozs of silver).

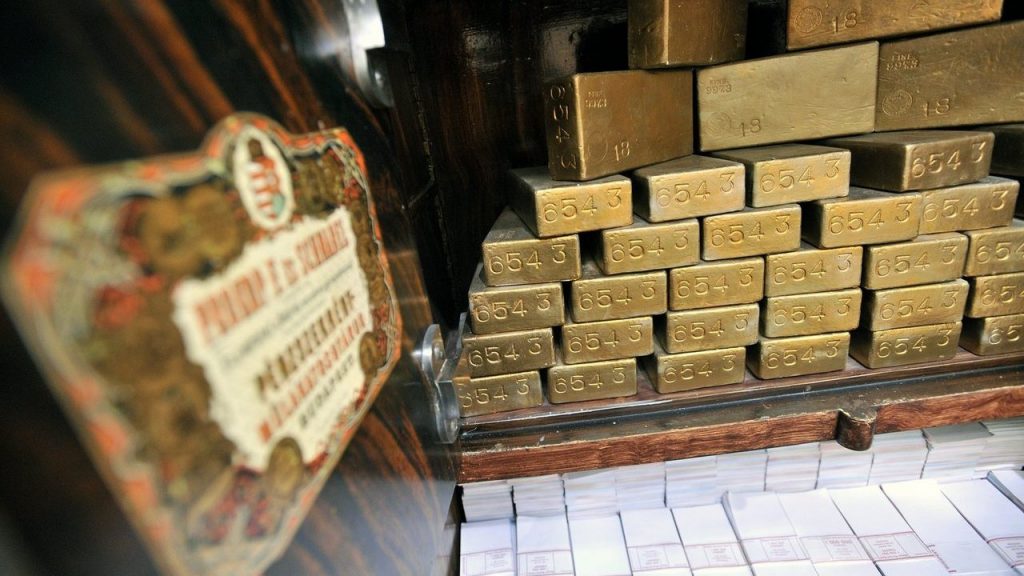

Said another way, 3863 tonnes added to the London LBMA vaults during March would be 124,200 wholesale silver bars (each bar weighing about 1000 ozs). These 124,200 bars are stored 30 bars per pallet. This would be 4,140 pallets extra pallets of silver bars. Usually these vaults store pallets of silver 6 pallets high. That would be 690 extra towers of pallets, each 6 pallets high. It would mean that 193 containers (each allowed to carry a maximum of 20 tonnes) arrived at the London vaults during March, or over 8.4 containers on average per day, every business day, and that the vault staff had to move and store 180 pallets each day. All of this in an environment where everyone from refiners to Mints to wholesalers to bullion retailers are reporting availability issues in sourcing physical silver bars right now. Seems plausible, right? And this LBMA vault data does not even break down how much each of the LBMA London vaults of JP Morgan, HSBC, Brinks, Malca-Amit, Loomis, and ICBC Standard, claim to hold. Which is why, if the LBMA vault data on silver (and gold) is to be even remotely trusted (which is a far stretch), then it is now time to independently and physically AUDIT THE LBMA VAULTS. Not that this will ever happen given that the LBMA is run by the bullion banks which run the paper silver and gold markets. But it needs to happen. More info @ https://www.lbma.org.uk/prices-and-data/london-vault-holdings-data  Gold bars in the Central Bank of Hungary’s vaults in Budapest The central bank of Hungary, the Magyar Nemzeti Bank (MNB), has just announced a purchase of a massive 63 tonnes of Good Delivery gold bars, and in doing so tripled the nation’s gold holdings from 31.5 tonnes to 94.5 tonnes. In its press release about the huge transaction, published April7, 2021, the Hungarian central bank explains its rationale for the dramatic purchase of what is approximately 5040 large (400 oz) gold bars, highlighting that gold has no credit risk and no counterparty risk, and so reinforces sovereign trust over all economic environments (normal and extreme), while being one of the most crucial reserve assets that a central bank can hold.

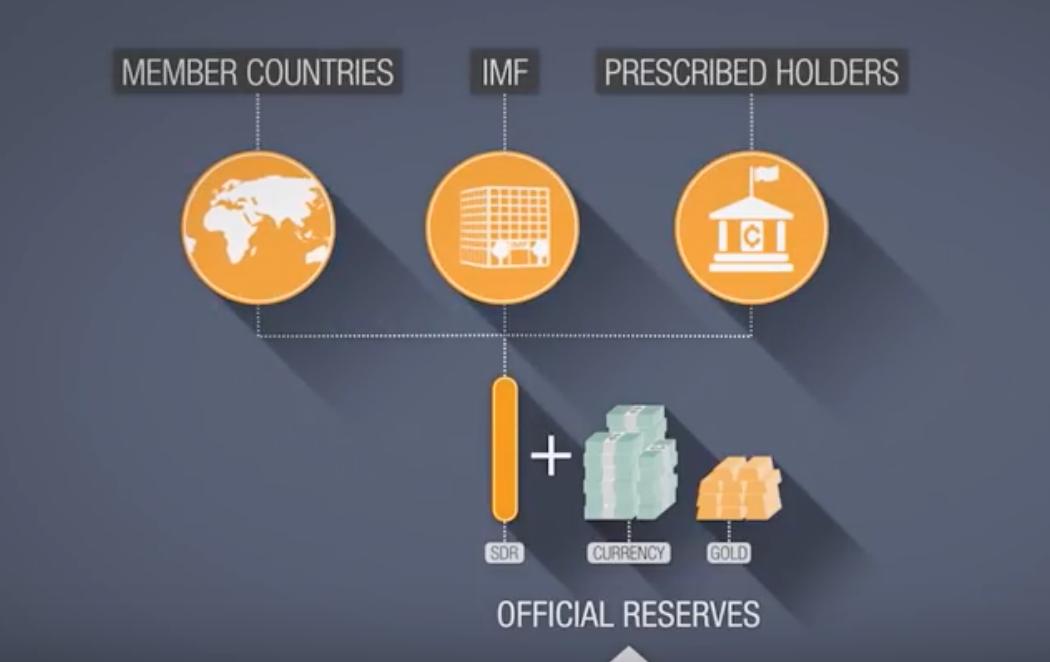

From 10 Fold to 30 Fold For those who may remember, this is not the first major gold purchase by the Hungarians in recent times, as the Hungarian central bank also caused shockwaves in October 2018 when it purchased 28.4 tonnes of gold, on that occasion increasing its gold reserves 10 fold from 3.1 tonnes of 31.5 tonnes, or a 1000% increase. This means that over exactly two and a half years, the Hungarians have increased their sovereign gold reserves by a staggering 3000%, or 30 fold, from 3.1 tonnes to 94.5 tonnes, an absolute increase of 91.4 tonnes. How’s that for a conviction trade? On the October 2018 occasion, the Hungarians purchased their 28.4 tonnes of gold at the Bank of England in London, and repatriated it back to Hungary in the same month, announcing the purchase and the repatriation at the same time, saying that ‘the repatriation has already taken place‘. On this occasion, the MNB does not say where it bought its 63 tonnes of gold, but it may well have been again at the Bank of England in London. Nor does the MNB say if the 63 tonnes of gold has been repatriated to Hungary yet. However, going on the previous pattern from 2018, one would expect that yes it has been brought back to Hungary by plane and under heavily armed guard. A No Confidence Vote in the System Interestingly, this time around in 2021, the Magyar Nemzeti Bank says that part of the motivation for the new gold purchase is in “managing new risks arising from the coronavirus pandemic”, which is a subtle way of saying that since central banks and governments around the world have used the Covid excuse to ramp up debt levels, ramp up quantitative easing and ramp up money supply growth, therein debasing their fiat currencies and introducing inflationary risks to bond holders, the Hungarians are simultaneously ramping up their physical gold holdings to counter this insanity. Or said in the diplomatic language of the latest Hungarian central bank press release, these concerns “further increase the importance of gold in national strategy as a safe-haven asset and as a store of value.” Virtually everybody knows what a dollar is, but not as many know about the SDR. The International Monetary Fund’s (IMF) Special Drawing Rights is an international, monetary reserve system created specifically to address limitations of gold and standard fiat currencies such as the USD. In short, should these fail, central banks and their governments retain the ability to trade and plan with liquidity via another, exclusive instrument — the SDR. An Artificial Currency The SDR is not an actual currency, according to the IMF, but a “potential claim on the freely usable currencies of IMF members.” As the official unit of account for the group, and an instrument only available to member countries’ central banks, the IMF itself and “designated, official entities,” SDR are exclusive assets. The average individual cannot get their hands on SDR. Comprising a basket of major global currencies, the composition of the Special Drawing Rights is reviewed in five-year intervals. Currently the SDR utilizes USD, EUR, CNY, JPY, and GBP.  The system is said to enable liquidity in international finance when assets like gold or other fiat currencies fail to do so. In the event of an unprecedented, worldwide economic collapse, SDR could become a centralized means by which to rebuild global trade networks. In fact, after the global downturn of 2008-09, the IMF’s issuance of SDR to member countries spiked dramatically in an attempt to re-stabilize the world economy.

Creation of SDR The SDR system was created in 1969 and “was initially defined as equivalent to 0.888671 grams of fine gold—which, at the time, was also equivalent to one U.S. dollar,” imf.org relates. “After the collapse of the Bretton Woods system, the SDR was redefined as a basket of currencies.” Of course, the collapse of Bretton Woods meant the international abandonment of the gold standard and the beginning of floating exchange rates. SDR is a uniquely isolated system, with its own exclusive economy and management, including interest rates set weekly and allocations to member countries determined via IMF criteria. Controversy, Control and Crypto The International Monetary Fund is well known as a financial superpower, exercising great influence in a wide scope of global affairs. The group has drawn sharp criticism throughout the years for allegedly destroying local economies and agriculture, negatively affecting healthcare, and overregulation of competing currencies and monetary instruments such as Bitcoin and crypto. In 2018, the group interestingly discouraged the Marshall Islands from creating their own cryptocurrency which could potentially challenge dollar hegemony on the islands, while just months later advocating central bank-issued digital currencies in other, more powerful national economies. While the Marshall Islands appear to be pressing on with their plan, still advocating the SOV national currency designed to fight inflation, standing up to a surveillance and regulatory behemoth like the IMF is not easily done, and likely not without serious compromises. Unlike SDR, cryptocurrencies like bitcoin are not regulated or allocated by a centralized, monetary surveillance authority such as the IMF. This has been a source of concern for the group, with former IMF head and European Central Bank presidential nominee Christine Lagarde stating in April: “I think the role of the disruptors and anything that is using distributed ledger technology, whether you call it crypto, assets, currencies, or whatever … that is clearly shaking the system.” For central bankers, this is clearly a threat to stability. Some advocates of radical financial freedom, however, believe that a decentralized shake-up of the old order may be just what is needed. After all, if the IMF can have its own special emergency currency in today’s climate of global financial instability, why not everyone else? Federal Reserve Chairman Jerome Powell said Monday (March 22) that cryptocurrencies are “speculative” investments, and therefore not reliable. He added that the Fed is moving slowly on the matter of creating a digital dollar, despite the soaring price of bitcoin in recent months.

Speaking at a virtual panel discussion, he added that cryptocurrencies are “highly volatile and therefore not really useful stores of value — and they’re not backed by anything.” As reported by CNBC, Powell said, “It’s more a speculative asset that’s essentially a substitute for gold rather than for the dollar.” The panel discussion on digital banking was hosted by the Bank for International Settlements. Meanwhile, Coinbase said that bitcoin was trading near $57,000, as it has attracted big name investors and some acceptance in the financial industry. For the past several years, the Fed has worked on its own payments system. CNBC said that the final product is likely to happen over the next two years. Last month, U.S. Treasury Secretary Janet Yellen said that central banks should explore creating and issuing sovereign digital currencies. The opportunity is that such currencies — digital dollars among them — could create “faster, safer and cheaper payments,” she said at a virtual conference. “There’s a lot of things to consider here,” Yellen said. “But it’s worth looking at.” Yellen said that among those “things to consider” is how regulators would “manage money laundering and illicit finance issues.” The rise of cryptocurrencies demands advanced technologies to close the gap with financial criminals, said. Ed Wilson, a partner at Venable LLP, a firm that specializes in financial regulations. Wilson told PYMNTS that solutions will involve using advanced technologies to help financial institutions (FIs) close the gap, with financial criminals out to exploit the digital movement of money. “Banks put too much emphasis on reducing reputational risks [caused by] regulatory failure,” he said. “They could reduce that if they would instead change how they run their account opening and anti-money laundering procedures.”

As the need for its reparations function ceases, the BIS takes up a role of a banker to the central banks and other international financial organizations, and provides a forum for promoting international cooperation, dialogue, as well as policy analysis among central banks and within the international financial community. Furthermore, it also acts as a centre for economic and monetary research

Its head office is in Basel, Switzerland and there are two representative offices: in the Hong Kong Special Administrative Region of the People's Republic of China. 2. Main Functions The Bank for International Settlements (BIS) is an international organization which fosters monetary and financial cooperation and serves exclusively as a bank for central banks. Therefore, it does not accept deposits from, or provide financial services to, private individuals or corporate entities. The BIS fulfils its mandate by acting as: 2.1 A forum to promote discussion and policy analysis among central banks and within the international financial community Bimonthly meetings of the Governors and other senior officials of the BIS member central banks to discuss monetary and financial matters are instrumental in pursuing this goal. The standing committees located at the BIS support central banks, and authorities in charge of financial stability more generally, by providing background analysis and policy recommendations. These committees also help formulate international standards and best practices on the relevant matters. The committees comprise:

2.2 A prime counterparty for central banks in their financial transactions and an agent or trustee in connection with international financial operations The BIS offers a wide range of financial services to assist central banks and other official monetary institutions in the management of their foreign reserves. BIS financial services are provided out of two linked trading rooms: one at its Basel head office and the other at its office in Hong Kong SAR. In addition to standard services such as sight/notice accounts and fixed-term deposits, the Bank has developed a range of more sophisticated financial products which central banks can actively trade with the BIS to increase the return on their foreign assets. The Bank also transacts foreign exchange and gold on behalf of its customers. The BIS also offers a range of asset management services in sovereign securities or high-grade assets. These may be either a specific portfolio mandate negotiated between the BIS and a central bank or an open-end fund structure. Furthermore, the BIS extends short-term credits to central banks, usually on a collateralized basis, and coordinates emergency short-term lending to countries in financial crisis. 2.3 A centre for economic and monetary research The economic, monetary, financial and legal research of the BIS supports its meetings and the activities of the Basel-based committees. The BIS is also a hub for sharing statistical information amongst central banks, and for publishing statistics on global banking, securities, foreign exchange and derivatives markets. 3. Organization Structure The three most important decision-making bodies within the Bank are: the General Meeting of member central banks, the Board of Directors and the Management of the Bank. Decisions taken at each of these levels concern the running of the Bank and as such are mainly of an administrative and financial nature, related to its banking operations, the policies governing internal management of the BIS and the allocation of budgetary resources to the different business areas. The BIS currently has 55 member central banks, all of which are entitled to be represented and vote in the General Meetings. Voting power is proportionate to the number of BIS shares issued to each country. 4. Relationship with Members The members can hold shares in the BIS since 2000. In total there are 547,125 shares of issued capital. The change in the BIS regulation requiring shares to be held only by central banks (CB's). As a shareholder, representatives from the CB's are invited to attend regular meetings of Governors held every two months in Basel. These gatherings provide an opportunity for participants to discuss the world economy and financial market developments, and to exchange views on topical issues of central bank interest or concern. The main result of these meetings is an improved understanding by participants of the developments, challenges and policies affecting various countries and markets. In addition, the BIS organizes frequent meetings of experts on monetary and financial stability issues as well as on more technical issues such as legal matters, reserve management, IT systems, internal audit and technical cooperation. Though targeted mostly at central banks, BIS meetings sometimes involve senior officials and experts from other financial market authorities, the academic community and market participants. 5. The Bottom Line The BIS is a global center for financial and economic interests. As such, it has been a principal architect in the development of the global financial market. Given the dynamic nature of social, political, and economic situations around the world, the BIS can be seen as a stabilizing force, encouraging financial stability and international prosperity in the face of global change.  On average international monetary systems last about 35 to 40 years before the tensions they create becomes too great and a new system is required. Prior to the first world war, major economies existed on a hard gold standard. Intra-wars, most economies returned to a “semi-hard” gold standard. At the end of the second world war, a new international system was designed — the Bretton Woods order — with the dollar tied to gold, and other key currencies tied to the dollar. When that broke down at the start of the 1970s, the world moved on to a fiat system where the dollar was not backed by a commodity, and was therefore not anchored. This system has now reached the end of its usefulness. An understanding of the drivers of the 30-year debt supercycle illustrates the system’s tiredness. These include the unending liquidity that has been created by the commercial and central banks under this anchorless international monetary system. That process has been aided and abetted by global regulators and central banks that have largely ignored monetary targets and money supply growth. The massive growth of mortgage debt across most of the world’s major economies is one key example of this. Rather than a shortage of housing supply, as is often postulated as the key reason for high house prices, it’s the abundant and rapid growth in mortgage debt that has been the key driver in recent decades. This is also, of course, one of the factors sitting at the heart of today’s inequality and generational divide. Solving it should contribute significantly to healing divisions in western societies. With a new US administration, and the end of the Covid battle in sight with the vaccination rollout under way, now is a good time for the major economies of the west (and ideally the world) to sit down and devise a new international monetary order. As part of that there should be widespread debt cancellation, especially the government debt held by central banks. We estimate that amounts to approximately $25tn of government debt in the major regions of the global economy. Whether debt cancellation extends beyond that should be central to the negotiations between policymakers as to the construct of the new system — ideally it should, a form of debt jubilee. The implications for bond yields, post-debt cancellation, need to be fully thought through and debated. A normalisation in yields, as liquidity levels normalise, is likely. High ownership of government debt in that environment by parts of the financial system such as banks and insurers could inflict significant losses. In that case, recapitalisation of parts of the financial system should be included as part of the establishment of the new international monetary order. Equally, the impact on pension assets also needs to be considered and prepared for.

Secondly, policymakers should negotiate some form of anchor — whether it’s tying each other’s currencies together, tying them to a central electronic currency or maybe electronic special drawing rights, the international reserve asset created by the IMF. As highlighted above, one of the key drivers of inequality in recent decades has been the ability of central and commercial banks to create unending amounts of liquidity and new debt. This has created somewhat speculative economies, overly reliant on cheap money (whether mortgage debt or otherwise) that has then funded serial asset price bubbles. Whilst asset price bubbles are an ever-present feature throughout history, their size and frequency has picked up in recent decades. As the Fed reported in its 2018 survey, every major asset class over the 20 years from 1997 through to 2018 grew on average at an annual pace faster than nominal GDP. In the long term, this is neither healthy nor sustainable. With a liquidity anchor in place, the world economy will then move closer to a cleaner capitalist model where financial markets return to their primary role of price discovery and capital allocation based on perceived fundamentals (rather than liquidity levels). Growth should then become less reliant on debt creation and more reliant on gains from productivity, global trade and innovation. In that environment, income inequality should recede as the gains from productivity growth become more widely shared. The key reason that many western economies are now overly reliant on consumption, debt and house prices is because of the set-up of the domestic and international monetary and financial architecture. A Great Reset offers therefore opportunity to restore (some semblance of) economic fairness in western, and other, economies. Adding Financial Data to Digital Authoritarianism China is pushing aggressively to be a global leader in financial technology. Over the last several years, use of mobile payment platforms has exploded in China while cash transactions have declined. At the same time, global interest in the development of central bank digital currencies (CBDCs) has also risen, with dozens of central banks now researching ways to offer digital versions of their fiat currency to ordinary citizens. The People’s Bank of China (PBOC) is leading in these efforts, aiming to release a central bank digital currency of its own. This CBDC system, which the Chinese government calls Digital Currency/ Electronic Payment (DCEP), will likely enable the Chinese Communist Party (CCP) to strengthen its digital authoritarianism domestically and export its influence and standard-setting abroad. By eliminating some of the previous constraints on government data collection of private citizens’ transactions, DCEP represents a significant risk to the long-held standards of financial privacy upheld in free societies. The PBOC’s DCEP strategy is motivated by a number of factors. The dominance of private mobile payment firms in China has given such companies an outsized role in retail commerce, making them indispensable to the economy. The PBOC is seeking a digital currency to harness the market share and technological innovation of private financial firms and to gain better access to information about the financial activities of Chinese consumers. DCEP is also part of China’s geopolitical ambitions, and CCP officials frame the progress of DCEP as similar to advancements in other strategically important emerging technologies, such as artificial intelligence and robotics. DCEP’s development also comes against a backdrop of China’s broader push to internationalize the renminbi. Few technical details about DCEP are publicly confirmed. The PBOC has indicated that DCEP will have a two-tier structure, with the PBOC managing the back-end infrastructure while employing banks and other companies to aid in distribution to the public. It is clear that, despite much initial PBOC discussion about distributed ledger infrastructure, DCEP will not use blockchain as part of its design. DCEP is also likely to allow for some basic programmability involving its transactions and to offer users the opportunity to access the currency via software wallets. Despite some official statements and reporting about these general features, much of the precise operational architecture is still being worked out. China is pushing aggressively to be a global leader in financial technology. It is also clear that the Chinese government hopes to leverage DCEP for the CCP’s domestic political agenda. Whereas PBOC officials have indicated that they will harness huge amounts of DCEP data to enhance monetary policy and monitor for illegal activity, officials higher in the Chinese government have stressed DCEP’s value as a tool for enforcing party discipline. PBOC officials also have said that DCEP will have “controllable anonymity,” allowing the central bank to see all of the transactions taking place while maintaining privacy among transacting parties. However, the system will also enable the CCP to exercise greater control over private transactions, as well as to wield punitive power over Chinese citizens in tandem with the social credit system. Additionally, although a number of PBOC officials hope DCEP will help drive internationalization of the renminbi, DCEP is unlikely to do so by itself in the short term.

The PBOC is in position to launch the largest digital currency project of any major economy. DCEP pilot tests have been underway since mid-2020 in several localities, and a number of state-owned banks and technology firms are building interfaces and distribution systems for the platform. The PBOC hopes to make DCEP available for wider use around the time of the 2022 Winter Olympics, which will be hosted in Beijing. With China’s quick progress in developing and testing the system, U.S. policymakers must closely track DCEP’s development and act strategically to address its potential to further the CCP’s coercive power and its influence in the evolving global financial system. Although DCEP is not likely to displace the U.S. dollar as a global reserve currency, it may serve as a model and standard-bearer for other countries to emulate. The United States might not necessarily need to create its own CBDC, but it must adapt to the quickly changing payments space, understand the geopolitical implications of this technology, influence its development, counter the DCEP’s threats to political and economic liberty, and ensure that financial technology innovation does not further China’s digital authoritarianism.  What is a Bitcoin and how does it work? Well, according to Google, Bitcoin is a decentralized digital currency that you can buy, sell and exchange directly, without an intermediary like a bank. It’s almost right what Google is telling us. Actually only one thing is right, it’s digital? But digital what? Is it a currency? Is it stock? Is it a commodity? Or is it an asset?

So is it true that you can buy, sell and exchange Bitcoins directly? I don’t think so. For buy, sell and exchange Bitcoins to Fiat currency and back, you need a regular bank. Don’t forget. The regular bank knows who you are and the Bitcoin bank need to know that too. Actually they need to know your regular bank account information, they verify it, you need to send them your ID. All will be carefully checked before you can enter the Bitcoin world.

So what is the big advantage of Bitcoins. Well, it’s true you can exchange Bitcoins from Wallet to Wallet. It will be noticed by your receive or send Bitcoin address. Oh, sorry I didn’t mention it before that your Bitcoin Wallet has a receive and send part, both identified by an address. These addresses are not secret. You can find them in the Block chain. And the Bitcoin bank(s) know they are yours. And your Wallet has a balance sheet too. So you can see you own $100,- Bitcoin value in the morning and only $90 in the evening. According to the Bitcoin/dollar exchange rate. What it a Bitcoin really worth? I don’t know. It is based on trust and an agreement. We trust the world behind Bitcoin. We trust the Bitcoin banks. We trust the Block chain. But for what reason? A regular bank is backed by the Central bank of the country. But what is backing the Bitcoin (bank)? We agree on represented value to a fiat currency like the dollar. But what makes that value? The market. Supply and demand? And what when you buy in Euro’s and the Euro is not supporting you? For me it’s just a Ponzi scheme. The ones who did buy the first Bitcoins in 2009 are the winners. But when you step in now you’re just a fool or you have too much money to burn. You will never make the profit they did make so far. But…. some captains of industries, like Elon Musk, Mike Cuban and Kevin O’Leary, think it’s the best thing ever. But is it? Sure it has a price, but does it have value? So is it smart to buy Bitcoin? I don’t think so.  Less than a week ago in ‘Houston, we have a Problem”: 85% of Silver in London already held by ETFs. We explain how with the emergence of the #SilverSqueeze, the silver-backed ETFs which claim to hold their silver in London, now account for 85% of all the silver claimed to be stored in the London LBMA vaults (over 28,000 tonnes of the LBMA total of 33,609 tonnes). This, for anyone who can out 2 and 2 together, does not leave very much available silver in London for silver ETFs or for anyone else, especially the largest silver ETF in the market the giant iShares Silver Trust (SLV), which let’s not forget has the infamous JP Morgan as custodian.

That SLV has seen massive dollar inflows in late January and early February with corresponding jumps in claimed silver holdings is now widely known, but is worth repeating here, for what’s about to come next. 3,416.11 Tonnes of Silver? The intense market interest in the iShares Silver Trust (SLV) started on 28 January when a huge volume of 152 million shares traded on NYSE Arca. Again on Friday 29 January, SLV traded a massive volume of 113 million shares. This led to an increase in SLV ‘Shares Outstanding’ on Friday 29 January of 37 million shares, and a same day claim by JP Morgan, the SLV custodian, that it had increased the silver held in the SLV by 37.67 million ozs (1,171 tonnes), all claimed to be sourced in the LBMA vaults in London. On Monday 01 February, an even larger 280 million SLV shares traded on NYSE, and by end of day SLV shares outstanding jumped by 20 million. On that day SLV claimed to add another 15.376 million ounces of silver (478.25 tonnes) within the LBMA vaults in London, about three-quarters of the value of the new SLV shares created on that day. On Tuesday 2 February, with SLV trading still elevated on NYSE, the iShares Silver Trust created a massive 61,350,000 new SLV shares, bringing the SLV shares outstanding to 729.1 million. On the same day, JP Morgan and Blackrock claimed to have added a huge 56.783 million ozs of silver (1,766 tonnes) to the SLV (again all in London), an incredible amount by any measure, but still short of reflecting the total of 118.45 million total of new shares that had been created between Friday and Tuesday (which led them to adjust down shares outstanding by 8.6 million on Wednesday 3 February). Over this time, you can see a nearly one for one relationship between the change in number of SLV shares outstanding and the amount of silver ounces claimed to be added to SLV. Between Friday 29 January and Wednesday 3 February inclusive, SLV shares outstanding increased by a net 109.85 million. Over the 3-day period from Friday 29 January to Tuesday 2 February, SLV claimed to have added an incredible 109.83 million ozs of silver (3,416.11 tonnes), with holdings of silver bars rising from 567.52 million ozs of silver to 677.35 million ounces (from 17,651.77 tonnes to 21,067.88 tonnes).According to the SLV daily bar lists, this extra 3,416.11 tonnes of silver added to SLV between 29 January and 2 February was in the form of 113,501 Good Delivery silver bars (the bars weighing approx. 1000 oz each). Again, according to the SLV bar list, these bars were added in five London vaults which SLV uses, namely Brinks vault in Premier Park London (45.5%), Loomis London vault (27.7%), Brinks Unit 7 vault Radius Park London (15.5%), Malca Amit London vault (6.0%) and JP Morgan’s own London vault (a measly 5.3%). In fact, according to the bar lists, SLV only started tapping into silver in the Brinks Premier park vault on Monday 1 February, and only started tapping to silver held in the Loomis London vault on Tuesday 2 February. Which to some people may look like a case of desperation or maybe even panic. |

Thank you for choosing to make a difference through your donation. We appreciate your support.

Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed