"Goodbye". And down in tears, moved. Zlatan greets Milan without playing and the Curva Sud of Milan pays homage to him with a banner. It says "Godbye", a play on words dedicated to the idol of all time, two-time Italian champion in the Rossoneri shirt and special leader. Milan-Verona opened like this, with Zlatan's moved face next to the bench of the first team, in those sofas from which he never stopped cheering on him during the long months of stop. Ibra, once framed on the big screen, mimicked a heart with his hands, addressed to his fans. Everyone in the stadium is crying, and he laughs at first. Then even his eyes become glossy, red, wet, full of sincere tears, and then even Ibrahimovic the tough guy, Rosengard's boy, the braggart of the ghetto who sings, dances, cries and retires to San Siro. His Rossoneri "The Last Dance" is all in one sentence that cuts through the goodbye and immediately turns into a farewell. Goodbye to the ball. "The time has come to say goodbye to football." And this is how it suddenly appears, after months and months of statements in which Zlatan had proudly shown his chest saying "I want to continue".

Dark suit, pigtail, shirt with the last button open, the whole family in the stands and seventy thousand Milan fans all for him. His wife Helena, framed several times on the big screen, is crying profusely, as are her children. Zlatan's ceremony begins after the 3-1 win against Verona, with a red carpet rolled out to midfield and the players around him. Ibra receives applause and hugs, the last with Pioli, Maldini, Massara and the president Scaroni, who give him a t-shirt with the number 11 autographed by the whole team. All on the notes of "Now we are free", the soundtrack of the Gladiator. Then he leaves: “At this stage many memories bind me, many emotions. I want to thank all my family and those who have been patient with me. And then I say thanks to my second family, the players and the fans, from the bottom of my heart. You made me feel at home." The last sentence is for the entire Rossoneri world: “I will be a Milan fan for life. Now the time has come to say 'hello' to football, but not to you. See you around, if you're lucky." And then row to take the applause during the greeting field lap. Dancing, singing, moving, this time on the notes of "The best" by Tina Turner. Ibra day is a festival of love and passion. Even giants cry their eyes out. We will miss him, but he will never be far away. Nel cuore.

0 Comments

Imagine, for a moment, that the government of Cuba was demanding the extradition of an Australian publisher in the United Kingdom for exposing Cuban military crimes. Imagine that these crimes had included a 2007 massacre by helicopter-borne Cuban soldiers of a dozen Iraqi civilians, among them two journalists for the Reuters news agency.

Now imagine that, if extradited from the UK to Cuba, the Australian publisher would face up to 175 years in a maximum-security prison, simply for having done what media professionals are ostensibly supposed to do: report reality. Finally, imagine the reaction of the United States to such Cuban conduct, which would invariably consist of impassioned squawking about human rights and democracy and a call for the universal vilification of Cuba. Of course, it doesn’t take a stretch of the imagination to deduce that the above scenario is a rearranged version of true events, and that the publisher in question is WikiLeaks founder Julian Assange. The antagonising nation is not Cuba but rather the US itself, which is responsible for not only the obliteration of Assange’s individual human rights but also a stunning array of far more macro-level assaults on people across the world. As per the US narrative, Assange’s WikiLeaks endeavours endangered the lives of people in Iraq, Afghanistan, and elsewhere – although it would seem like one surefire way to not endanger lives in such places would be to not blow them up in the first place. It is furthermore perplexing that a nation for which military slaughter is an institutionalised pastime should make such a selective stink about the exposure of certain gory details. Granted, footage of defenceless civilians being picked off at close range like videogame targets by a laughing helicopter crew does little to uphold Americans’ projected role as the “good guys” – a façade that is key in terms of justifying the country’s self-presumed right to wreak international havoc as it pleases. Had Assange wanted to save his own skin, he could have stuck to the sort of imperial propaganda that functions as mainstream journalism, a field that was itself instrumental in selling the wars on Afghanistan and Iraq to the US public. Instead, he is incarcerated at Belmarsh prison in southeast London, awaiting extradition to the so-called “land of the free” while serving as a veritable case study in prolonged psychological torture, as documented back in 2019 by the UN Special Rapporteur on Torture. In a caustic letter addressed to King Charles ahead of his recent coronation, Assange described himself as a “political prisoner, held at your majesty’s pleasure on behalf of an embarrassed foreign sovereign”. He observed: “One can truly know the measure of a society by how it treats its prisoners, and your kingdom has surely excelled in that regard”. The embarrassed foreign sovereign has certainly exhibited excellence in that realm, as well, boasting the highest incarceration rate on the planet and an impressive track record of executing innocent people. To be sure, domestic efforts to sentence a citizen of another country to 175 years in prison for telling the truth is also a pretty good indication that something is very, very wrong with a society. Then there’s the whole matter of the United States’ offshore penal colony in Guantánamo Bay, Cuba, the former CIA torture den and persistent judicial black hole into which the US has sought to disappear some of the human fallout of its forever wars. Indeed, the fact the US feels entitled to call out the Cuban government for its own “political prisoners” while operating an illegal prison on occupied Cuban territory can be safely filed under the category of mind-blowingly sinister hypocrisy. If only there were more journalists who wanted to talk about such things. But just like you can’t cover up the crimes of Guantánamo by classifying prisoners’ artwork, you can’t hide the horrors of US policy by effectively redacting Julian Assange out of existence. It’s the old kill-the-messenger approach – in which the “killing” takes the form of long-drawn-out psychological erosion conducted in tandem with a campaign to normalise the idea that Assange should be behind bars for eternity-plus. In the end, the assault on Assange is not just your average disproportionate imperial conniption fit. Whatever the ultimate outcome, it has already set a perilous precedent in criminalising not only freedom of speech and the press but also – if you think about it – freedom of thought. Although Australian officials are making increasing noise agitating for Assange’s release, Australian Prime Minister Anthony Albanese has refused to say whether he will address the issue with US President Joe Biden at the Quad Leaders’ Summit in Sydney on May 24. And as the forever wars of the US rage on increasingly out of sight, so, too, does the forever war on Julian Assange.  In recent years, the concept of being "woke" has become increasingly prevalent in society. Being woke generally refers to being aware of social issues and actively fighting against oppression and injustice. While this may seem like a positive movement, there are dangers associated with a community that is too focused on being "woke."

First and foremost, the idea of being woke can be extremely divisive. While it is important to recognize and address societal issues, constantly focusing on them can create an "us versus them" mentality. This can lead to a lack of understanding and empathy for those who may not share the same views or experiences. A community that is too woke can become intolerant of differing opinions, which can lead to a breakdown in communication and further divide society. Additionally, the pressure to be constantly "woke" can be overwhelming and lead to a sense of burnout. It is important to recognize that social issues cannot be solved overnight, and it is not the responsibility of any one person to fix everything. The constant pressure to be aware of every issue and to constantly speak out about them can be exhausting and ultimately counterproductive. Another danger of a community that is too focused on being woke is the potential for hypocrisy. It is easy to criticize others for not being woke enough or for perpetuating societal issues, but it is important to also recognize our own biases and shortcomings. The idea of being woke can create a culture of virtue signalling, where individuals may speak out against issues solely to gain social status or to be seen as "woke." Furthermore, a focus on being woke can sometimes lead to a lack of action. While it is important to recognize societal issues, it is equally important to take action to address them. A community that is too focused on being woke may become complacent in their activism, believing that simply acknowledging issues is enough to effect change. In conclusion, while it is important to be aware of societal issues and to fight against oppression and injustice, a community that is too focused on being woke can be dangerous. It can lead to division, burnout, hypocrisy, and a lack of action. It is important to strive for a balance between awareness and action, and to approach social issues with empathy and understanding for all individuals.  The merger between Switzerland’s two largest lenders, the embattled Credit Suisse and UBS, could have a negative impact on the entire Western bond market, Bloomberg reported on Monday, citing analysts.

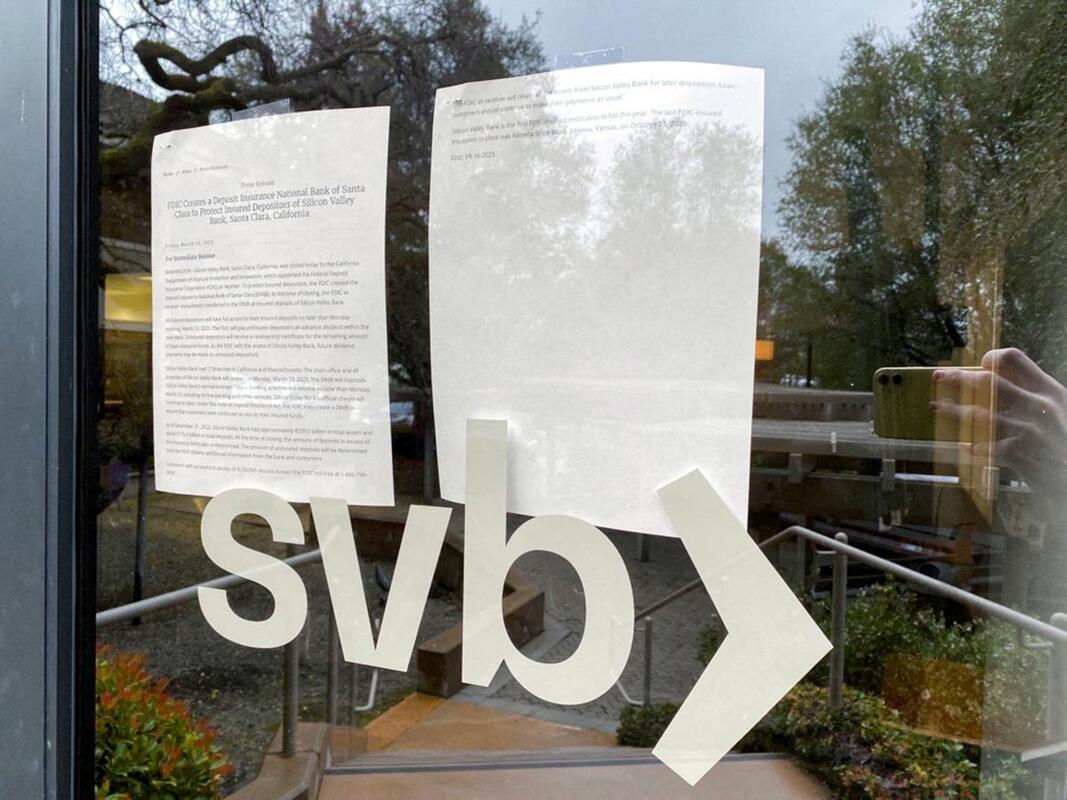

UBS agreed on Sunday to acquire its rival, which was on the brink of insolvency due to the loss of investor and customer confidence, for 3 billion Swiss francs ($3.24 billion) in stock. The deal, brokered by the Swiss authorities, came with a 9-billion-franc government guarantee for potential losses from Credit Suisse assets and 100 billion francs in liquidity assistance from Switzerland’s central bank. However, as part of the deal, Swiss financial market regulator FINMA ordered Credit Suisse to write down to zero some 16 billion Swiss francs ($17.24 billion) of its Additional Tier 1 (AT1) bonds, with the aim of bolstering the bank’s capital and resolving its liquidity problems. AT1 bonds are a riskier form of bank debt, which were created in the wake of the global financial crisis of 2008, and represent a type of junior debt that allows banks to transfer risks to investors instead of taxpayers in cases of financial difficulties. Investors find them attractive as they pay higher interest due to the fact that they carry more risk than regular bonds. While bondholders will be left with nothing, Credit Suisse shareholders will receive $3.23 billion under the UBS deal, despite the fact that bonds traditionally stand above equities in the banking hierarchy. The situation has angered bondholders, Bloomberg reports, as they now fear the authorities in other countries may follow the Swiss government’s lead. “It’s stunning and hard to understand how they can reverse the hierarchy between AT1 holders and shareholders… Wiping out AT1 holders while paying substantial amounts to shareholders goes against all the resolution principles and rules that were agreed internationally after 2008,” Jerome Legras, the head of research at Axiom Alternative Investments, an investor in Credit Suisse’s AT1 debt, has said. “This just makes no sense… Shareholders should get zero… it’s crystal clear that AT1s are senior to stocks,” Patrik Kauffmann, a fixed-income portfolio manager at Aquila Asset Management, who also holds the bonds, said. Some analysts, however, argue that the write-off of the bonds is a logical step, as this is part of the reason they were created – as a way to impose losses on creditors instead of taxpayers in case of bank failures. Overall, experts predict that either the AT1 market will soon be closed for new issuance, or the bonds will surge in price because of the extra risk displayed by the Credit Suisse rescue merger.  It is early days yet to assess if the collapse of Silicon Valley Bank (SVB) will turn out to be a Lehman moment for the global financial system. SVB’s failure was triggered by factors different from the ones that precipitated the Lehman collapse or for that matter, India’s bad loan crisis. If those crises were about banks piling on credit risks on their loan books, SVB’s failure can be traced to mis-management of rate risks in its investment book.

Running an asset-liability mismatch to earn a spread is central to any banking business. But SVB stretched this concept much too far in deploying its copious deposit flows into long-dated treasuries and mortgage securities, which it parked mainly in its held-to-maturity (HTM) portfolio. As inflation rose and the US Fed raised interest rates by 450-475 basis points, SVB’s portfolio racked up large losses. The advent of the funding winter, which prompted start-ups to draw down their deposits, forced SVB to liquidate not just its Available For Sale bonds but also its HTM ones. The resulting $1.8 billion write-off followed by a failed attempt to raise capital, spooked the closely-knit start-up community to launch a run on SVB’s deposits. When interest rates shoot up in a short span, no bank can shield its investment book from losses. But SVB was more vulnerable to a run than a vanilla bank, because of its over-reliance on big deposits from a closed ecosystem — start-ups, their founders and VCs. The Federal Deposit Insurance Corporation has been quick to take over SVB, halting the run. But its ability to shore up dented depositor confidence in US banks, may depend on whether SVB’s uninsured depositors (who make up 90 per cent of its $175 billion book) will need to take haircuts. To prevent a snowballing effect on the start-up ecosystem, SVB’s clients may need to be thrown a liquidity lifeline to meet emergency payouts. As SVB had limited inter-linkages with other banks, a contagion effect on the US or global banking system from its failure, appears unlikely. But its collapse does call for stricter regulatory vigilance on other counts. With the previous crisis stemming from lending, the current global regulatory framework for banks focusses a lot on proactive accounting of bad loans and stress-testing their impact on capital adequacy. But the SVB crisis highlights that in a scenario of rapidly rising rates, banks’ investment books need an equal degree of scrutiny and stress-testing. The present expedient of allowing banks to sweep their bond losses under the carpet by owning large HTM portfolios, can lead to blow-ups. In India, the RBI may need to scrutinise bank books for depositor concentration. The SVB saga also offers a salutary lesson to global central banks that when they switch from extended ultra-loose monetary policies to uncalibrated, sharp rate hikes to quell inflation, they can inflict damage not just on growth, but also on financial system stability that they strive so hard to protect.  The future of central bank digital currency (CBDC) is highly dependent on the actions and decisions of central banks and governments around the world. As of now, some central banks are actively exploring the possibility of issuing their own digital currency. For example, the People's Bank of China has been working on a digital version of the Chinese yuan for several years, and it's expected to be launched in the near future. Other central banks, such as the European Central Bank and the Bank of Japan, are also conducting research and pilot projects on CBDCs. However, the decision to issue CBDCs is not one that should be taken lightly. There are many technical, legal and regulatory challenges that need to be addressed before launching CBDCs. Furthermore, Central Banks will have to ensure that CBDCs will not lead to financial stability risks and that it will coexist with other forms of money. If CBDCs are successfully implemented, they could have a significant impact on the global economy and financial system. They could provide an alternative to private cryptocurrencies, while also making it easier for people to access and use digital payments. Additionally, they could also help to reduce the risks associated with physical cash and improve financial inclusion.

On the other hand, if not properly implemented, CBDCs could lead to unintended consequences such as financial stability risks, erosion of privacy and freedom and a decline in the use of bank deposits and other financial products. Central bank digital currency (CBDC) is a topic that has been gaining a lot of attention in recent years. As the world becomes increasingly digital, many central banks are exploring the possibility of issuing their own digital currency as a way to modernize their monetary systems and stay relevant in the age of digital payments. There are a number of potential benefits to CBDCs. For one, they could help to reduce the risks associated with physical cash, such as the potential for counterfeiting and money laundering. They could also make it easier for people to access and use digital payments, especially in areas where access to traditional banking services is limited. One of the main arguments in favor of CBDCs is that they could provide an alternative to private cryptocurrencies like Bitcoin, which are decentralized and not backed by a government. CBDCs, on the other hand, would be issued and regulated by central banks, providing a level of oversight and stability that is currently lacking in the world of private cryptocurrencies. However, there are also some potential downsides to CBDCs. One concern is that they could further erode privacy and financial freedom, as central banks would have access to detailed information about how individuals are using the currency. Additionally, the introduction of CBDCs could also have an impact on the traditional banking system, potentially leading to a decline in the use of bank deposits and other financial products. Overall, the idea of central bank digital currency is an interesting one that deserves further exploration. While there are certainly potential benefits, it's important for central banks and policymakers to carefully consider the potential downsides and unintended consequences before moving forward. Ultimately, any decision to issue CBDCs should be made with the goal of promoting financial inclusion, stability, and security for all citizens.  The issue of the creation of a BRICS reserve currency has taken on particular significance in recent months after President Putin declared that the creation of such a currency was in the process of discussion. This was followed by a series of statements coming from Russia’s legislative branch on the expediency of creating a new reserve currency — most recently from the Federation Assembly speaker Valentina Matvienko. While the debate on the possibility of creating such a reserve currency is only starting in Russia and more broadly across the global economy, the implications of such a move on the part of the BRICS could have transformational consequences for the global financial system.

Initially, the proposal to create a new reserve currency based on a basket of currencies of BRICS countries was formulated by the Valdai Club back in 2018 — the idea was to create an SDR-type currency basket composed of BRICS countries’ national currencies as well as potentially some of the other currencies of BRICS+ circle economies. The choice of BRICS national currencies was due to the fact that these were the among the most liquid currencies across emerging markets. The name for the new reserve currency — R5 or R5+ — was based on the first letters of the BRICS currencies all of which begin with the letter R (real, ruble, rupee, renminbi, rand). The recent debates concerning the prospects for the creation of a new reserve currency focused more on the risks, fragilities and outright impossibility of the R5 project. Less attention has been accorded to estimating the benefits (including in terms of hard figures) to BRICS economies and EM more generally. There has also been scant attention with respect to the actual modalities of launching the BRICS reserve currency. What is clear at this stage is that the BRICS reserve currency will not be created to replace the national reserve currencies of the BRICS economies — rather it will complement these national currencies and will serve to improve the possibilities for more EM currencies to attain reserve status. Accordingly, the attainment of high trading shares among the BRICS economies is a desirable but not altogether an indispensable condition for launching the new reserve currency. In fact, the new BRICS currency does not have to service all trade transactions among BRICS economies in the very near term. Initially, the new BRICS currency could perform the role of an accounting unit to facilitate transactions in national currencies. In the longer run, the R5 BRICS currency could start to perform the role of settlements/payments as well as the store of value/reserves for the central banks of emerging market economies. Within the composition of the R5 currency basket the share of the Chinese renminbi may be initially set at a relatively high level in order to take advantage of the already advanced reserve status of the Chinese currency. This share may be reduced progressively in stages later on along with the inclusion of new EM national currencies. Outside of the BRICS economies some of the potential candidates that with time could be included into the R5+ currency basket may feature the Singaporean dollar or the UAE’s dirham. One of the potential risks associated with the use of EM currencies in reserves is their high volatility. The basket mechanism of the BRICS reserve currency will allow for reducing some of this volatility via averaging out the exchange rate dynamics of currencies that follow different market trends — if the currencies of Russia, South Africa and Brazil follow the commodity cycle, the opposite is true with respect to commodity importers such as India and China. Importantly, the scope for employing the new reserve currency in the world economy is sizeable given the tremendous potential for de-dollarization. The new BRICS reserve currency can act in concert with the stronger role performed by BRICS national currencies to take on a greater share of the total pie of currency transactions in the world economy. This greater role can be gradually extended from servicing foreign trade transactions to investment flows across the developing world. In line with the original R5 concept developed by Valdai Club in 2018 one of the possible venues for boosting the use of national currencies and the BRICS reserve currency could be the creation of a platform for regional development banks in which BRICS economies are members. Such a platform could develop a portfolio of common/integration projects that may be financed in national currencies. In the end, the launching of a new reserve currency if successful will impart a transformational effect on the international financial system. The Central Banks in the global economy are experiencing a notable shortage of reserve currencies in managing their reserve holdings. In this respect, the emergence of additional reserve currencies from among the EM economies will serve to expand the possibilities for diversifying reserve holdings and reducing the vulnerabilities associated with the dependence on a narrow range of currencies. The R5 project can thus become one of the most important contributions of emerging markets to building a more secure international financial system.  As I sat with my family watching the first half of France vs Morocco, a chant from Moroccan fans rumbled through the stadium.

“Are they saying ‘La ilaha il Allah’?” I asked my husband. “No way – but it sure sounds like it.” They were, in fact, repeating the first half of the Muslim declaration of faith, “There is no God but God,” and a few claps later, the second half: “Muhammad is the messenger of God.” A sort of collective rallying cry to both uplift spirits and express pride in Islam’s central creed among fellow believers. Our scepticism clearly had not caught up with the mesmerising spectacle that was the Atlas Lions. It was the winning streak that at least in this region, we could not look away from – the deeply satisfying underdog narrative of this World Cup, most deliciously for Arabs, Africans, the diaspora in the West, and Muslims collectively, rejoicing at an authentic representation of their lived faith and values on display in the most celebratory way. When some of the players showed the world just how much they love their mothers, many Muslims joked that it was only due to the “mother’s ‘dua’ [prayer]” that they were still hanging on. Others commented that their against-all-odds victories – against Belgium, Spain, Portugal – were a case of feeling more at home at the first World Cup in the Middle East, being in their neck of the woods (or the closest thing to it), and the energy of the fans, that propelled them to keep on keeping on. No one could deny the electrifying Moroccan fandom that to an outsider seemed to pop up in Qatar overnight. And that is the thing about this story in particular – it was as much about the fans as it was about the players. When Morocco beat Portugal last week, a colleague turned to me and asked an important editorial question: “So, the first African team to make it to the semis, or the first Arab team?” My answer did not skip a beat. “Both. All of it. And then some. Their win means whatever you want it to mean, for you.” We decided right there and then that our coverage would not delve into the very real identity ping-pong taking place over who gets to claim Morocco. It is not that these debates are not valid; it is that we simply chose to lean into a moment swirling in optimism and unity. We also chose a different conversation to spotlight: the power of football as a force for social change. I spoke to a few people who were merely supporting Morocco in solidarity with the Palestinian cause, as players and fans regularly waved the Palestinian flag. For them, the following message about Palestinians was enough: “They exist. Their struggle is real and felt beyond their homes. They will not be erased.” It is so much bigger than football. And the ability of the Atlas Lions to connect so many people from different backgrounds around a common desire to believe in miracles, shift the game when no one saw it coming, in a region ignored by football’s big guns (until now) – was a story worth telling, and one the world needed, however fleeting.  In a large-scale raid, German police targeted dozens of individuals from the far-right Reichsbürger scene who were suspected of planning a coup. What kind of movement is this — and what threat does it pose to democracy?

A group of "Reichsbürger" allegedly spent months preparing for a "Day X," on which they wanted to overthrow the government. In a large-scale raid on Wednesday morning, several suspects were arrested, including ex-soldiers and a former member of the Bundestag. Since November 2021, they had been holding secret meetings and engaged in shooting exercises in preparation for a coup, according to the attorney general. In their plans, the suspects did not shy away from the use of military force or homicide. "The sheer number of arrests and searches has shocked me," sociologist Timo Reinfrank, executive director of the Amadeu Antonio Foundation. The foundation is one of Germany's leading NGOs working against right-wing extremism, racism, and antisemitism. "A real coup d'état can hardly succeed in Germany, as the state order and the constitution are too solid for that, but these people believe it is possible. That shows how caught up they are in their delusion." But attacks like the one on the Capitol in Washington, D.C., on January 6, 2021, would also be possible in Germany, Reinfrank fears. What does the movement believe? Reichsbürger reject the German legal system and the country's parliamentarism, and most of them propagate the re-establishment of the German empire founded in 1871. They also believe that the victorious Western Allies of World War II, who defeated Nazi Germany, still secretly rule the country. In recent years, the growing number of Reichsbürger has alarmed German security authorities. In its June 2022 report, the domestic intelligence service estimated that around 21,000 people belong to this scene — and their number is rising. The high potential for violence among the self-proclaimed Reichsbürger was described as particularly worrying: "Around 500 of these people still have at least one weapons permit," the intelligence report read. The Reichsbürger are not a homogeneous group, according to a 2018 study by the Amadeu Antonio Foundation. Instead, the term refers to a "large, very diverse milieu of ideologists" who vary in their propensity for violence and militancy, but all are united by the belief that the Federal Republic of Germany is not a sovereign state. They reject the constitution and all state institutions. Around 1,150 of the Reichsbürger — or just over 5% — were classified as right-wing extremists in 2021. But many others also use elements of right-wing extremist ideology or believe in antisemitic conspiracy myths. The idea that Germany's borders should be extended to include territories in Eastern Europe, which were occupied under Nazi rule that ended in 1945, is also found in its milieu. How dangerous are the Reichsbürger? In recent years, a number of serious crimes have been attributed to Reichsbürger. Several have stood trial for murder or attempted murder. The crimes registered by the domestic intelligence service rose sharply between 2020 and 2021. Reinfrank said that militancy is already rooted in the Reichsbürgers' ideology. "Because Reichsbürger do not recognize the constitution and the legitimacy of the security authorities, their ideology legitimizes them to act with violence." "These are not people who commit random attacks. They want to specifically attack the basic state order, like elected local politicians," Reinfrank explained. The past three years of protests against the COVID-19 restrictions led to radicalization and an increase in the number of supporters of Reichsbürger ideology. For example, at a demonstration by the group "Freie Geister" (free spirits), protesters held a banner that read: "Sovereignty. For the freedom of our country." "The scene has become radicalized. People are becoming more receptive to the core idea of the Reichsbürger, that Germany is not free and the elected government is not sovereign," Reinfrank said.  Frustration and grievances over China’s zero-COVID policy have led to large protests in more than a dozen cities, on a scale unseen since the Tiananmen Square demonstrations in 1989. These youth-led social protests involved open calls for a change not just in COVID-19 policies but in governance and politics as well. The big message from the scenes coming out of China: The suppression of policy debates in an increasingly centralised bureaucracy can ignite social unrest overnight despite intensified censorship and security enforcement. For the moment, the Chinese Community Party has responded by moving to ease some virus restrictions despite high daily case numbers, signalling softened positions in the face of mounting protests. But the key test for President Xi Jinping lies ahead: What has he really learned from the outpouring of anger on China’s streets, in its universities and at its factories?

After the student-led Tiananmen Square protests in 1989, which were triggered by the death of pro-reform leader Hu Yaobang, the ruling CCP drew lessons from the incident by adopting a collective leadership model that was more open towards policy debates in government and in society. The Chinese leaders who followed, including Jiang Zemin and Hu Jintao, moved away from strongman politics towards a power-sharing model at the top. More broadly, the CCP underwent a thorough shift — what was labelled “re-institutionalisation” — led by senior leaders like Zeng Qinghong (China’s vice president under Hu Jintao), Li Yuanchao (vice president during the early years of Xi’s rule), and political theorist Wang Huning. This move towards a semblance of inner-party democracy encouraged policy debates at various levels and pushed forward a decentralisation process that empowered local officials to promote economic development. Some observers described the process as an example of the CCP’s “authoritarian resilience”, in which a single leader could not dominate policy-making in all realms and had to share power with other colleagues in the Politburo and its Standing Committee — the party’s top bodies. The political game was transformed from the conventional winner-take-all model to a power-balancing model, in which all of the Politburo Standing Committee members were vested with almost equal political authority, resulting in more power-sharing and high-level checks and balances. The regime’s authoritarian feature was lessened by fragmented policy enforcement, relatively subdued censorship and abundant policy debates. Xi became a game changer in 2012, when he replaced Hu Jintao as CCP general secretary and started a “re-centralisation” process that consolidated his power as the core leader of the party. Facing a disgruntled society vexed by yawning income disparity and corruption, Xi borrowed from Mao Zedong’s tactical playbook and urged civil servants and military officers to reconnect with the common people — while tightening limits to discussions of ideas such as democracy and freedom of speech. With the ruling party’s tightening control of the media and the rectification of ideology, opinion leaders in China have appeared more cautious than before about voicing different views over public policies or human rights. This has brought the move towards more robust policy debates within the CCP under Jiang and Hu to a screeching halt. The result: increased risks from policy blunders, since there are fewer checks and balances in place.  The breaking news throughout the first half of November has been dominated by coverage of the sudden collapse of FTX, one of the world’s biggest cryptocurrency exchanges. The crash has shaken the crypto market, lost institutional investors billions – and individual customers millions – led to official investigations of FTX in several countries, and made some question whether the Bitcoin sphere might crash and burn outright, and perhaps cause wider problems for the financial system.

Some take the view that FTX was a fraud all along, ever since its launch in April 2019. If that’s the case, it has grave implications for the US Democratic Party and Ukrainian government, as the company’s corrupt activity may have been used to fund both, openly and secretly. The Ukraine connection On March 14, FTX launched a new online portal for cryptocurrency donations, Aid for Ukraine, in partnership with Ukraine’s Ministry of Digital Transformation. Through this, crypto traders, both large and small, could donate bitcoin and other cryptocurrencies, which FTX would convert into cash for the Ukrainian Ministry of Defense to spend on weapons and other war-related expenses. Very rapidly, the fund claimed to have amassed “over” $60 million in donations. By April 14, it was reported that just over $45.15 million of that sum had been splurged on digital rifle scopes, thermal imagers, monoculars, rations, armor, helmets, military clothing, tactical backpacks, fuel, communication devices, laptops, drones, medical supplies, and a “worldwide anti-war media campaign.” The same records show a further $10 million was spent over the next three months – leaving around $5 million in the bank, so to speak. An Aid for Ukraine social media post on November 15 said this sum was still held in reserve, and that $60 million remained of the total amount of donations received through the portal to date.This seems very odd, particularly given that Ukraine was reported to have received $100 million in bitcoin donations, and then spent almost all of it, between February 24 and March 11 alone, before Aid for Ukraine’s establishment. Are we to believe that – over the course of seven months, from the time the $60 million figure was first publicized to today – no further funds at all have been donated through Aid for Ukraine? Despite the entire crypto community having been able to do so, and being actively encouraged to do so that whole time? Official investigations into FTX, and its founder and CEO Sam Bankman-Fried, have only just begun. However, it seems clear already that he secretly and illegally moved billions stored in the FTX exchange to its sister company Alameda Research, a quantitative trading firm that he also runs. The gaping black hole Bankman-Fried’s sleight-of-hand created meant that, when customers sought to withdraw their money from the exchange, FTX didn’t have the funds to keep up with demand. It seems he was assisted in this underhand ploy by a “back-door” specially created for him in the company’s accounting, which meant sums could be moved into and out of the exchange off the books, and without auditors or FTX employees noticing. Much of the money taken out of FTX by Bankman-Fried has disappeared completely. The US Securities and Exchange Commission and Commodity Futures Trading Commission are particularly looking at whether these stolen client deposits were used to prop up Alameda in any way, which was reportedly struggling financially. There is, as yet, no sign though that these authorities are probing an obvious lead – Aid for Ukraine. Was money moved from FTX to Alameda, then channelled to Kiev to be spent on Western – mainly US – weapons, and indeed other activities that the government and its backers in Washington, London, and elsewhere in Europe and North America would prefer to be kept hidden? Conversely, money raised beyond the initial $60 million total could’ve been funnelled out of Aid for Ukraine by Bankman-Fried to enrich himself, or secretly spent for very different purposes – such as funding the US Democratic Party’s election campaigns. The Democratic Party connection Bankman-Fried is a very well-connected figure in US politics, especially to the Democratic Party. Over the course of the 2020 presidential election cycle, he contributed $5.2 million to two super PACs supporting Joe Biden’s campaign and was the overall second-largest individual donor to Biden that year. Such extravagant spending appears trivial today. In 2021/22, he provided tens of millions to Democratic causes and candidates, becoming the party’s second-largest donor, behind only “spyless coup” specialist George Soros. Bankman-Fried has boasted of meeting policymakers in Washington “every two or three weeks for the last year.” Over 2022, this has included multiple audiences with senior government officials and top Biden advisers at the White House. These meetings escalated in volume around the time that the Ukraine conflict began. On March 7, exactly one week before Aid for Ukraine was launched, his brother Gabe Bankman-Fried – who directs his political operations – visited the White House along with Jenna Narayanan, a Democratic strategist who once worked for the Democracy Alliance, which has been called the “most powerful liberal donor club” in the US. Bankman-Fried himself then visited the White House on numerous occasions in April and May, concurrent with him donating $865,000 to the Democratic National Committee. In early June, mere days after his last recorded White House meet-and-greet, Bankman-Fried announced he would invest up to $1 billion in further funds between then and 2024 to guarantee Biden – or whoever might take his place – won the next presidential election. These activities have been interpreted by many as an attempt by Bankman-Fried to ingratiate himself with politicians to further his commercial interests. It is certainly true that, at the same time, he and FTX high rankers were attempting to influence US lawmakers on crypto regulation, to make the market more favourable for his company. In this context, the promised $1 billion appears to be a dangled carrot, an implied promise of future financing if Bankman-Fried got his way. Accompanying him on some of these visits was Mark Wetjen, FTX head of policy and regulatory strategy, who previously served as commissioner on the Commodity Futures Trading Commission under President Barack Obama – but only some. Were the other meetings related to Ukraine? If so, the $1 billion pledge may have reflected what Bankman-Fried thought could be secretly skimmed from Aid for Ukraine for Democratic Party purposes. It’s conspicuous that in mid-October, he completely disowned that enormous commitment, saying, “That was a dumb quote. I think my messaging was sloppy and inconsistent in some cases.” In repudiating his $1 billion promise, Bankman-Fried also quietly added that he would stop giving any money at all to political causes. It was just days later that it was announced FTX was subject to investigation in Texas for allegedly selling unregistered securities. Jump to a few weeks later, and the company had filed for bankruptcy. Bankman-Fried clearly said something he shouldn’t have back in June – whether he got carried away by all the positive press and high-level access his political donations were receiving and wrote a proverbial check in public he couldn’t privately cash, or his comments drew unwanted attention to how much money was actually flowing into Aid for Ukraine, we do not currently know. But the truth must out.  This month, United States President Joe Biden warned that the world could face Armageddon if his Russian counterpart, Vladimir Putin, were to use a tactical nuclear weapon in Ukraine. You would imagine that such a prognosis would lead to urgent action to dial down the confrontation. Yet no effort is being made to move us back from that risk. On the contrary, governments on all sides are piling on more threats, more militarisation and more actions that are not just making nuclear war possible but are increasing its probability.

Last week, NATO began a round of nuclear exercises simulating the dropping of ‘tactical’ B61 nuclear bombs over Europe. Although these drills are presented as routine, they are occurring alongside parallel Russian exercises. It’s hard to imagine worse timing. Surely with concerns about Armageddon expressed at the very highest levels of power, these exercises should have been called off as a message that the West won’t contribute to escalating nuclear tensions? Instead, our leaders are systematically failing to reduce the risk. Still, there are powerful messages that should be listened to and acted upon. In August — even before Putin’s latest, thinly veiled nuclear threats — United Nations Secretary General Antonio Guterres warned that the world is “one miscalculation away from nuclear annihilation”. His words must serve as a wake-up call to leaders who pursue policies inexorably driving us towards nuclear war and to populations that are not yet taking action to stop these terrible dangers. Guterres warned that we are at a time of nuclear danger “not seen since the height of the Cold War”. He cautioned against countries seeking “false security” by spending vast sums on “doomsday weapons”. He said that the world had been lucky that nuclear weapons have not been used since 1945. But as he rightly stated: “Luck is not a strategy. Nor is it a shield from geopolitical tensions boiling over into nuclear conflict.” Indeed, we cannot rely on luck. And we must remember what nuclear use means and understand what nuclear war would look like today. An estimated 340,000 people died after the US dropped atomic bombs over Hiroshima and Nagasaki in Japan in 1945. That included many who survived the immediate blast but died shortly afterwards from fatal burns. Others died because of the complete breakdown of rescue and medical services that had also been destroyed. And many more died when the impact of radiation kicked in, poisoning people and causing cancers and birth deformities. If that isn’t bad enough, consider this: The Hiroshima bomb was actually a small nuclear bomb in today’s terms. Current nuclear weapons — even the supposedly limited-range, battlefield-oriented ‘tactical’ nuclear weapons now routinely discussed in the context of the Ukraine war — are many, many times more powerful. The ones that the current exercises over Europe are designed for have variable yields of up to 20 times greater strength than the bomb that destroyed Hiroshima in 1945. Equally worrying are the recent policies of nuclear weapons states. We had seen gradual reductions in nuclear weapons for a few decades. Now we are seeing modernisation programmes on all sides, with the US planning an upgrade of missiles that can deliver nuclear weapons, France launching a project to build a new generation of nuclear-powered ballistic missile submarines, and Britain, India and Pakistan preparing to increase their nuclear arsenals.  History records that on October 16, 1962, then-US President John F. Kennedy received information from the CIA about the deployment of Soviet missiles in Cuba. This event was the formal beginning of the Cuban Missile Crisis — the first, and for a long time, the only event in world history that brought humanity to the brink of nuclear war. Back then, cool heads – who had not yet forgotten the horrors of a real war – were able to prevent a catastrophe. Whether today's leaders will show the same restraint is far from certain. Rhymes and echoes Nineteenth century American humourist Mark Twain famously said, “History never repeats itself, but it often rhymes.” Pakistani-British historian Tariq Ali is credited with a similar take: “History rarely repeats itself, but its echoes never go away.” Either could have been referring to today’s Russia-Ukraine conflict, which seems to be rhyming with, and echoing, a perilous episode from 60 years ago and 6,000 miles away – the Cuban Missile Crisis. Observers who recall the US-Soviet showdown of October 1962 can only hope that the latest confrontation between Washington and Moscow doesn’t require as much luck to avert a potentially planet-ending nuclear war. The similarities – rhymes and echoes – are evident. For starters, the Ukraine and Cuban crises were both rooted at least partly in the same principle: A superpower can’t stand idly by when a geopolitical rival upsets the security balance between them. In 1962, the trigger was the secret placement of Soviet missiles in Cuba, right on America’s doorstep. Soviet leader Nikita Khrushchev, who ironically grew up in what was then Ukraine, saw the move as a way to protect the island against a US invasion after the failed Bay of Pigs assault in April 1961, as well as a tit-for-tat response to the Pentagon’s deployment of Jupiter missiles in Turkey and Italy, which positioned Washington’s nuclear warheads to hit the USSR's territory in as few as ten minutes. At the time, the long-range missiles in Soviet territory took hours to fuel up and fire, meaning a delayed response to a US first strike. “Since the Americans have already surrounded the Soviet Union with a ring of their military installations, we should pay them back in their own coin and give them a taste of their own medicine so that they find out for themselves how it feels to live as a target of nuclear arms,” Khrushchev was quoted as saying by Aleksandr Alekseev, then Moscow’s ambassador to Cuba.  John Kennedy and Nikita Khrushchev meeting in Vienna for an friendly discussion US President John F. Kennedy didn’t see it that way when a U-2 spy plane spotted surface-to-surface missiles in Cuba on October 16. As Ukrainian-born author Sergey Plokhiy wrote in his 2021 book, ‘Nuclear Folly,’ Kennedy was initially inclined to order an attack on the missile sites, which easily could have escalated into a Soviet response and, eventually, mushroom clouds on both sides. The American president wasn’t yet aware that the Soviets had already shipped nuclear warheads to Cuba. Nor did he know that the USSR had 43,000 troops on the island, as well as tactical nukes that could be used to destroy a US attack force. But Kennedy knew that having Soviet ballistic missiles just across the Florida Straits – Havana is only about 1,100 miles from Washington and 230 miles from Miami – was intolerable and potentially gave the USSR the ability to win a nuclear war with the US. Russia has raised similar concerns about NATO’s eastward expansion. The Western military bloc was formed to ensure collective security against the USSR, but instead of reaping a peace dividend after the Soviet collapse in 1991, it has expanded to 30 states, nearly doubling in size. It also placed strategic weapons in Eastern Europe, which Moscow perceived as a threat. As if those moves weren’t provocative enough, NATO has also pledged to eventually push into Ukraine and Georgia, which would expand its reach into two former Soviet republics on Russia’s borders. Tensions escalated further when a US-backed coup overthrew Ukraine’s elected government in 2014, setting off a war between Kiev and separatists in the Donbass that left an estimated 14,000 people dead even before Moscow began its military offensive last February. Some observers have blamed the US and NATO for provoking the conflict. “As the one who started the Ukraine crisis and the biggest factor fueling it, the US needs to deeply reflect on its erroneous actions of exerting extreme pressure and fanning the flame on the Ukraine issue,” Chinese Foreign Ministry spokesman Zhao Lijian said in July.  A US Navy Lockheed SP-2H Neptune flying over a Soviet cargo ship with crated Russian bombers on deck in late 1962 Pope Francis claimed in June that World War III had already been declared and reiterated his claim that NATO may have triggered the crisis. He cited an unidentified world leader who told him that the bloc was “barking at the gates of Russia” and pushed back against criticism that he had failed to condemn Russian President Vladimir Putin. NATO isn’t just a casual association of states. As UK cabinet minister Sajid Javid noted in February, shortly before the Russian offensive started, an encroachment on one member is an encroachment on all. He even referred to the 30 member states as “NATO territory,” as if the bloc were one giant nation. In terms of security, it may as well be one country. As Article 5 of the NATO treaty states, an armed assault on one member is considered an attack on all. That was a heavy responsibility when NATO started with 12 close allies. It has become a far more precarious pledge with expansion eastward. A dust-up in Skopje or Tallinn, even if justifiable, could have just as much potential to trigger a nuclear conflagration as an attack against Berlin or Paris. And what if one of the little brothers is a bad actor, essentially provoking a fight that the big brothers are bound to finish? From Russia’s perspective, Ukraine would pose just such a risk. Putin has accused Kiev of committing “genocide” against Russian speakers in Donbass, and Ukraine has failed to implement the Minsk agreements, the protocols brokered by Germany and France to bring peace to the region. Russia also has called for the “denazification” of Ukraine. Moscow’s envoy to Washington, Anatoly Antonov, tried to explain Russia’s security concerns to a CBS News interviewer just four days before tanks rolled across Ukraine’s borders. Geopolitical rivals mustn’t trample on the principle of 'indivisible security', meaning neither NATO nor Russia should be allowed to strengthen its own security at the expense of the other party, he said. In that context, adding Ukraine to NATO would be “not possible for us to swallow,” Antonov explained. His next comment made clear why such tactics aren’t in the interest of NATO member states, either: You’ll see that there’s no space for us to retreat World War I was supposed to have taught politicians that hair-trigger alliances can bring unintended consequences, such as when the assassination of an Austrian archduke in Sarajevo set off a global conflict that killed or maimed 40 million people. The resulting carnage was so devastating that it was supposed to be “the war to end all wars,” though tragically, rival blocs were going at it again – with even more deadly consequences – just 21 years later.

British Prime Minister Liz Truss on Sept. 23 unveiled the UK’s biggest tax cuts since 1972 to tackle high energy costs and inflation, and to boost productivity and wages. However, the plan has roiled financial markets, as it lacks detailed forecasts on economic growth, inflation and public finances, and involves no firm commitments to fiscal discipline.

The concerns over the plan, coupled with the US Federal Reserve’s aggressive rate hikes, Russia’s invasion of Ukraine and fears of a global recession, pushed the British pound to an all-time low against the US dollar last week. Investors also ditched UK bonds as yields spiked amid expectations of ballooning government debt and even higher inflation. British equity markets also fell, with the blue-chip FTSE 100 hitting its lowest level since March. The volatility prompted the Bank of England to intervene by pledging unlimited purchases of long-dated bonds. However, the emergency measure is not expected to have major implications for the British central bank’s monetary policy, as it was deployed mainly to preserve financial stability. At the same time, investors would remain jittery about an ongoing bond sell-off once the two-week intervention period ends on Friday next week. Economists and investment strategists have said the British crisis could spill over to global markets, similar to Russia’s default on its domestic debt in 1998 and the Greek debt crisis in 2009, when domestic crises led to larger financial turmoil. Former US secretary of the Treasury Larry Summers wrote on Twitter on Tuesday that he was worried the British crisis might trigger a global crisis if the Truss government does not take steps to stop the bleeding in the pound and government bonds. As the pound is a global reserve currency, a balance-of-payment crisis in the UK could reverberate beyond the nation’s borders, Summers said. Seven Investment Management LLP strategist Ben Kumar said fear might be contagious and warned that UK equity outflows could prompt parallel selloffs worldwide, Bloomberg News reported on Saturday. More importantly, the UK’s troubles this time around are not just market turmoil caused by its own fiscal policies, but a reflection of the vulnerability of financial markets as policymakers revise their monetary and fiscal strategies after years of ultra-loose monetary policies. Specifically, there is growing tension between monetary and fiscal policymakers, as central banks hike rates to fight inflation while other government agencies prefer low interest rates, tax cuts and other incentives to spur post-COVID-19 economic recovery. Many central banks have raised interest rates and some have adopted quantitative tightening by selling the assets they have accumulated over the years. This two-pronged tightening has led to dramatic volatility in interest rates worldwide and caused global currencies to weaken against the ever-surging US dollar, with the euro falling to its lowest in 20 years, the Chinese yuan dropping to a 14-year low and the New Taiwan dollar looking to test the critical barrier of NT$32 against the greenback. Over the past two years, the world has made a concerted effort to combat the COVID-19 pandemic. However, countries need to work more closely together in the face of a likely vicious cycle triggered by the synchronized rate hikes to avoid a global financial crisis. As for Taiwan, the government must make financial, economic and industrial adjustments to cope with the challenge of a potential global recession.  A view of a Monument of the Soviet first mass-produced tactical nuclear bomb RDS-4 at the Fedora Poletaeva square in Moscow The world’s indifference to the prospect of a nuclear disaster, today, is frankly insane. For the past few months, Western experts have downplayed the probability that the Ukraine war would lead to nuclear escalation between Russia and the West. Since Putin first put Russia’s nuclear arsenal on alert back in February, many experts have argued that he was merely posturing in a bid to throw his “adversaries off balance”. However, Putin’s most recent threats of using such weapons — made in a televised speech on Wednesday morning — must not be taken lightly, regardless of his motivation or intention.

He said that Western officials have threatened Russia with nuclear weapons, a charge that US President Joe Biden denied during his speech to the United Nations General Assembly hours later. Putin also announced a partial mobilisation and his support for upcoming referendums in four Russian-controlled regions of Ukraine that could pave the way for their annexation by Moscow. It’s one thing for the West to dismiss as irrelevant the threat of Putin firing, for instance, a secretary. However, any chance he may fire his nukes should be taken seriously, regardless of how remote the possibility is. In fact, the West has so far avoided imposing a no-fly zone over Ukraine or transferring long-range missiles and other weapons that may threaten Russian territory for fear of the Kremlin’s retaliation against Europe. Yet, the sophisticated military assistance that the US and its allies have provided to Kyiv has begun to change the balance of power on the battlefield in favour of Ukraine. Russia’s mounting losses in the past few weeks are clearly pushing Putin into a corner. He is angry, humiliated and is losing clout at home and abroad. That’s why he has decided to mobilise 300,000 extra troops to try to reverse his setbacks in Ukraine. However, as past Russian and American wars have shown – whether in Vietnam, Afghanistan, Iraq or elsewhere – a troops surge may win him time but won’t necessarily win him the war. That’s why he coupled his decision for a military surge with a nuclear warning, putting the West on notice: back off or face the consequences. Hence the seriousness of Putin’s threat to use weapons of mass destruction. The threat is “not a bluff” as he put it, nor a bluster; it rather sounds desperate and deliberate. It is also the biggest escalation since the invasion began seven months ago and the biggest troop mobilisation since the end of the Cold War. Some are now sounding a warning about Putin’s potential use of tactical nuclear weapons on the battlefield. Or as one analyst put it: “Russia is willing to use nuclear weapons if Ukraine continues its offensive operations”. Indeed, former Russian President Dmitry Medvedev said on Thursday that the Kremlin could use tactical nuclear weapons to defend its occupation of parts of Ukraine that it annexes. In theory, the use of these weapons, which are short-range and designed for limited strikes, sounds implausible considering Ukraine’s geographic proximity and Russia’s nuclear doctrine which underlines the defensive use of nuclear weapons or when the very existence of Russia is threatened. |

Thank you for choosing to make a difference through your donation. We appreciate your support.

Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed