Shares of several regional US lenders plunged on Tuesday after the collapse of First Republic Bank, the third major casualty of the biggest crisis to hit the country's banking sector since 2008. Los Angeles-based PacWest Bancorp, which has $41.2 billion in assets, and Arizona-based Western Alliance Bancorp, which has $68 billion in assets, led the steep selloff. Shares of both lenders were down by at least 15% on Tuesday, triggering investor concerns about the financial health of other mid-sized banks. The pair has shed more than $5 billion in market value so far this year. The KBW Bank Index, a benchmark index tracking the leading lenders, slumped 5.52%, hitting its lowest since December 2020. The S&P 500 Index sank almost 2% at one point. The embattled First Republic Bank was taken over by regulators on Monday and will be sold to JPMorgan Chase, America’s biggest bank, which will “assume all deposits, including all uninsured deposits, and substantially all assets” of First Republic in a $10.6 billion deal.

If a ‘confidence crisis’ can happen to First Republic, it can happen to any bank in this country,” CEO of Longbow Asset Management Jake Dollarhide told Reuters.Investors fear the latest turmoil, which began with the failures of Silicon Valley Bank and Signature Bank in March, could spread to other regional banks. Both were shut down by regulators following massive bank runs. “Wall Street is quickly hitting the sell button as banking turmoil appears it is not going away anytime soon,” senior market analyst at Oanda, Ed Moya, told Bloomberg. “Risk appetite did not stand a chance as traders focused on lingering doubts over the regional banks, rising recession odds, and growing risks that the US could default on its debt next month,” he added. The selloff was driven by the threat of higher interest rates combined with high inflation data, making the situation worse and pointing to an economic downturn, economists say.

0 Comments

Swedish home prices continued to slide in March as stubborn inflation and surging borrowing costs extend a housing market crunch in the country. Residential property prices in the largest Nordic economy declined by 0.8% last month, data from the state-owned mortgage lender SBAB published on Monday showed. The decline had slowed to 0.6% in February, but most experts say housing prices will continue to fall and may even surpass the forecast 20% drop-off. Housing prices plunged by 15% in nominal terms last year, driven by surging inflation and interest rate hikes by the central bank. The worst housing-price slump in three decades in Sweden has contributed to a surge in defaults, particularly in the construction industry, which is responsible for 11% of the country’s economic output. In March, bankruptcies in the sector surged 14%, which has suppressed investment in new dwellings.

The chief economist at SBAB, Robert Boije, called the March slide “surprisingly strong” adding that he expects “significantly weaker development going forward if the Riksbank continues to raise the policy rate and inflation continues to remain at high levels.” Sweden’s housing market is the most vulnerable in the EU due to the country’s rising interest rates. Although about 64% of Swedes own their homes, many have mortgages. However, because in most cases these are not long-term, fixed-rate mortgages, there is a high degree of exposure across the sector to rising interest rates, which are now at their highest levels in more than a decade following a series of hikes by the Riksbank. Industry experts say housing prices are also strongly affected by unusually high electricity prices and warn that the decline in the Swedish property market may last for years.  Another bank is entering troubled territory amid the recent banking crisis that has spilled into global markets—this time in Germany.Deutsche Bank is facing fears of a collapse after shares dropped 11 percent on Friday morning, bringing those stocks down to a total of 29 percent since the bank chaos began on March 8. "We are still on edge waiting for another domino to fall, and Deutsche is clearly the next one on everyone's minds (fairly or unfairly)," Chris Beauchamp, chief market analyst at IG Group, told Reuters. "Looks like the banking crisis hasn't been entirely put to bed." Friday's stock market news is the latest development related to the fallout from the failure of Silicon Valley Bank (SVB) earlier this month, and the second involving a European bank. This week, Swiss bank Credit Suisse was rescued by rival UBS in a last-minute deal after Credit Suisse saw a plunge in share prices following the SVB collapse. Deutsche Bank's latest slump, driven partly by the Credit Suisse deal, signals that confidence in the banking system remains low. It marks the third week of decline for European banks, which fell 4.2 percent in the wake of the financial turmoil.

While many are worried it could be the next bank to collapse, other analysts have remained optimistic that it won't fall to the same fate as Credit Suisse. "We have no concerns about Deutsche's viability or asset marks. To be crystal clear - Deutsche is NOT the next Credit Suisse," research firm Autonomous said in a Friday report. German Chancellor Olaf Scholz has also dismissed the panic, saying that Deutsche Bank had "thoroughly reorganized and modernized its business model and is a very profitable bank," during a Friday news conference. In a Friday memo, JPMorgan strategists said that Deutsche Bank "had its own share of headline pressure and governance fumbles," but that it "still commands a relatively elevated cost base and has relied on its FICC (fixed income, currencies and commodities) trading franchise for organic capital generation and credit re-rating."

"Indeed, if there is anything depositors might learn from the past few weeks, both in the U.S. and Europe, it is just how far regulators will always go to ensure depositors are protected," JP Morgan wrote. Just a day earlier, Treasury Secretary Janet Yellen said the U.S. government was "certainly" prepared to take additional actions to stabilize banks—a shift in tone from her statements the day before, in which she said no such moves were being considered.  The merger between Switzerland’s two largest lenders, the embattled Credit Suisse and UBS, could have a negative impact on the entire Western bond market, Bloomberg reported on Monday, citing analysts.

UBS agreed on Sunday to acquire its rival, which was on the brink of insolvency due to the loss of investor and customer confidence, for 3 billion Swiss francs ($3.24 billion) in stock. The deal, brokered by the Swiss authorities, came with a 9-billion-franc government guarantee for potential losses from Credit Suisse assets and 100 billion francs in liquidity assistance from Switzerland’s central bank. However, as part of the deal, Swiss financial market regulator FINMA ordered Credit Suisse to write down to zero some 16 billion Swiss francs ($17.24 billion) of its Additional Tier 1 (AT1) bonds, with the aim of bolstering the bank’s capital and resolving its liquidity problems. AT1 bonds are a riskier form of bank debt, which were created in the wake of the global financial crisis of 2008, and represent a type of junior debt that allows banks to transfer risks to investors instead of taxpayers in cases of financial difficulties. Investors find them attractive as they pay higher interest due to the fact that they carry more risk than regular bonds. While bondholders will be left with nothing, Credit Suisse shareholders will receive $3.23 billion under the UBS deal, despite the fact that bonds traditionally stand above equities in the banking hierarchy. The situation has angered bondholders, Bloomberg reports, as they now fear the authorities in other countries may follow the Swiss government’s lead. “It’s stunning and hard to understand how they can reverse the hierarchy between AT1 holders and shareholders… Wiping out AT1 holders while paying substantial amounts to shareholders goes against all the resolution principles and rules that were agreed internationally after 2008,” Jerome Legras, the head of research at Axiom Alternative Investments, an investor in Credit Suisse’s AT1 debt, has said. “This just makes no sense… Shareholders should get zero… it’s crystal clear that AT1s are senior to stocks,” Patrik Kauffmann, a fixed-income portfolio manager at Aquila Asset Management, who also holds the bonds, said. Some analysts, however, argue that the write-off of the bonds is a logical step, as this is part of the reason they were created – as a way to impose losses on creditors instead of taxpayers in case of bank failures. Overall, experts predict that either the AT1 market will soon be closed for new issuance, or the bonds will surge in price because of the extra risk displayed by the Credit Suisse rescue merger. Well, well, well, it seems the collapse of Silicon Valley Bank (SVB) has brought a certain individual back into the spotlight. Joseph Gentile, the bank’s Chief Administrative Officer, has been making headlines due to his past involvement with Lehman Brothers, the global finance firm that famously went bankrupt during the 2008 financial crisis. Yup, you read that right, the same guy who used to be Lehman Brothers’ Chief Financial Officer (CFO) is now at the center of attention in the SVB debacle.

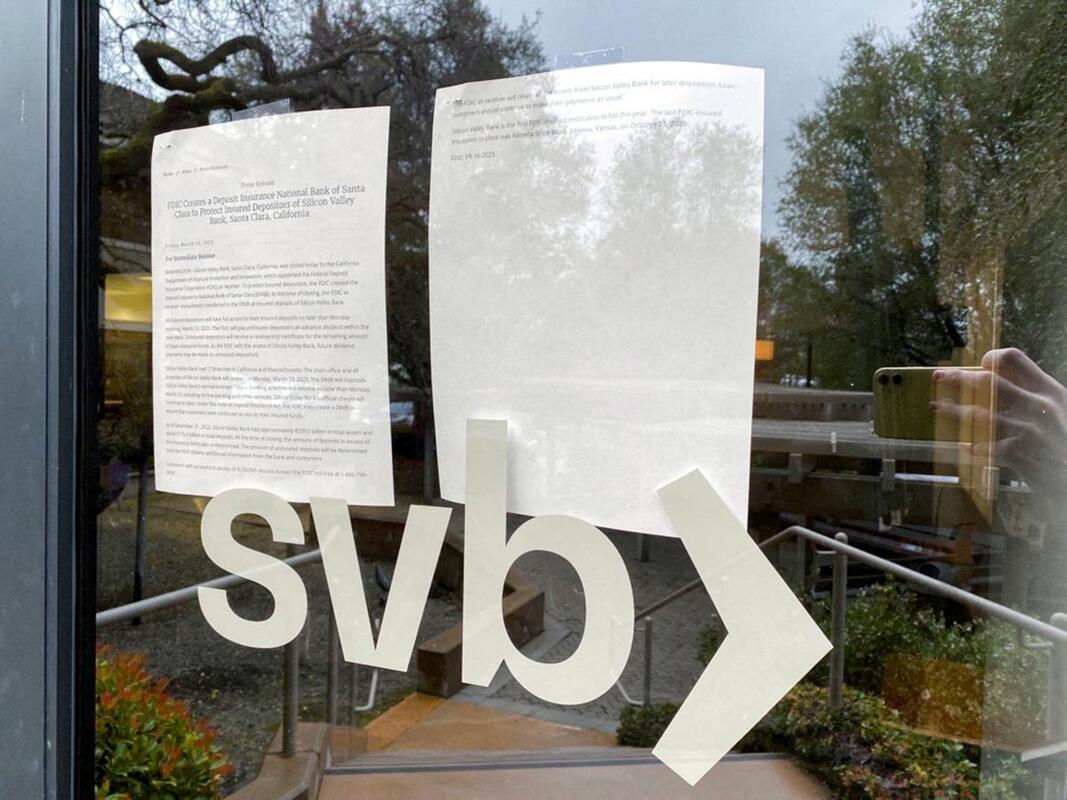

SVB, once the premier financial institution for tech and health startup businesses in the US, has been in a rapid downward spiral since Friday, with customers starting to withdraw their deposits due to the bank’s investments being adversely affected by recently hiked interest rates.This led to California regulators handing over control of the bank to the Federal Deposit Insurance Corporation (FDIC) and a bid for its assets now underway. Ouch. But back to Gentile. Twitter has been abuzz with comments and takes on his involvement with SVB, with some likening the bank’s collapse to the 2008 crisis, while others have taken a more humorous approach. “Just in case you thought you were bad at your job, Silicon Valley Bank’s Chief Administrative Officer Joseph Gentile was the former CFO of Lehman Brothers,” tweeted Stock Talk Weekly. Neither Gentile nor SVB has commented on the situation, leaving many to speculate on what led to the bank’s downfall and what this means for the tech and health startup businesses it once served.Alf (not that Alf), the founder of The Macro Compass, had some pretty harsh words for the way they’ve handled things. Spent hours going through SVB’s financial statements and changed my mind on the topic. “These guys weren’t bad at risk management. They were outright horrific. They literally gambled billions away,” he said on Twitter. Either the level of incompetence was extreme, or a gigantic amount of moral hazard was at play. I think the latter, and if I am right this is really f*cked up.”  It is early days yet to assess if the collapse of Silicon Valley Bank (SVB) will turn out to be a Lehman moment for the global financial system. SVB’s failure was triggered by factors different from the ones that precipitated the Lehman collapse or for that matter, India’s bad loan crisis. If those crises were about banks piling on credit risks on their loan books, SVB’s failure can be traced to mis-management of rate risks in its investment book.

Running an asset-liability mismatch to earn a spread is central to any banking business. But SVB stretched this concept much too far in deploying its copious deposit flows into long-dated treasuries and mortgage securities, which it parked mainly in its held-to-maturity (HTM) portfolio. As inflation rose and the US Fed raised interest rates by 450-475 basis points, SVB’s portfolio racked up large losses. The advent of the funding winter, which prompted start-ups to draw down their deposits, forced SVB to liquidate not just its Available For Sale bonds but also its HTM ones. The resulting $1.8 billion write-off followed by a failed attempt to raise capital, spooked the closely-knit start-up community to launch a run on SVB’s deposits. When interest rates shoot up in a short span, no bank can shield its investment book from losses. But SVB was more vulnerable to a run than a vanilla bank, because of its over-reliance on big deposits from a closed ecosystem — start-ups, their founders and VCs. The Federal Deposit Insurance Corporation has been quick to take over SVB, halting the run. But its ability to shore up dented depositor confidence in US banks, may depend on whether SVB’s uninsured depositors (who make up 90 per cent of its $175 billion book) will need to take haircuts. To prevent a snowballing effect on the start-up ecosystem, SVB’s clients may need to be thrown a liquidity lifeline to meet emergency payouts. As SVB had limited inter-linkages with other banks, a contagion effect on the US or global banking system from its failure, appears unlikely. But its collapse does call for stricter regulatory vigilance on other counts. With the previous crisis stemming from lending, the current global regulatory framework for banks focusses a lot on proactive accounting of bad loans and stress-testing their impact on capital adequacy. But the SVB crisis highlights that in a scenario of rapidly rising rates, banks’ investment books need an equal degree of scrutiny and stress-testing. The present expedient of allowing banks to sweep their bond losses under the carpet by owning large HTM portfolios, can lead to blow-ups. In India, the RBI may need to scrutinise bank books for depositor concentration. The SVB saga also offers a salutary lesson to global central banks that when they switch from extended ultra-loose monetary policies to uncalibrated, sharp rate hikes to quell inflation, they can inflict damage not just on growth, but also on financial system stability that they strive so hard to protect.  US stocks have soared to unsustainable highs and could crash 26% within months, Morgan Stanley's top strategist has warned. In an analyst note the bank's chief US equity strategist, Mike Wilson, said that the current level of stock valuations could be compared to the “death zone,” a term in mountaineering describing an altitude so high that climbers do not have enough oxygen to breathe. “Many fatalities in high-altitude mountaineering have been caused by the death zone, either directly through loss of vital functions, or indirectly by wrong decisions made under stress or physical weakening that lead to accidents,” Wilson wrote. “This is a perfect analogy for where equity investors find themselves today, and quite frankly, where they've been many times over the past decade,” he added.

The metaphor indicates the excessive levels that stock prices have climbed to since the start of this year. Wilson suggested the S&P 500 could tumble to 3,000 points within months, down about 26% from current levels, saying that “it’s time to head back to base camp before the next guide down in earnings.” The grim forecast follows what many analysts have called the worst year for the stock market since the 2008 financial crisis. All three indexes tumbled in 2022 with the Dow Jones Industrial Average ending the year down 8.8% while the S&P 500 sank 19.4% and the Nasdaq Composite plunged 33.1%. “The bear market rally that began in October from reasonable prices and low expectations has morphed into a speculative frenzy based on a Fed pause/pivot that isn't coming,” Wilson’s latest note said. The strategist has repeatedly warned that the market rally won’t last as he expects inflation to prove stickier than many other economists forecast, forcing the US Federal Reserve to hike rates in order to bring soaring prices under control.  The future of central bank digital currency (CBDC) is highly dependent on the actions and decisions of central banks and governments around the world. As of now, some central banks are actively exploring the possibility of issuing their own digital currency. For example, the People's Bank of China has been working on a digital version of the Chinese yuan for several years, and it's expected to be launched in the near future. Other central banks, such as the European Central Bank and the Bank of Japan, are also conducting research and pilot projects on CBDCs. However, the decision to issue CBDCs is not one that should be taken lightly. There are many technical, legal and regulatory challenges that need to be addressed before launching CBDCs. Furthermore, Central Banks will have to ensure that CBDCs will not lead to financial stability risks and that it will coexist with other forms of money. If CBDCs are successfully implemented, they could have a significant impact on the global economy and financial system. They could provide an alternative to private cryptocurrencies, while also making it easier for people to access and use digital payments. Additionally, they could also help to reduce the risks associated with physical cash and improve financial inclusion.

On the other hand, if not properly implemented, CBDCs could lead to unintended consequences such as financial stability risks, erosion of privacy and freedom and a decline in the use of bank deposits and other financial products. Central bank digital currency (CBDC) is a topic that has been gaining a lot of attention in recent years. As the world becomes increasingly digital, many central banks are exploring the possibility of issuing their own digital currency as a way to modernize their monetary systems and stay relevant in the age of digital payments. There are a number of potential benefits to CBDCs. For one, they could help to reduce the risks associated with physical cash, such as the potential for counterfeiting and money laundering. They could also make it easier for people to access and use digital payments, especially in areas where access to traditional banking services is limited. One of the main arguments in favor of CBDCs is that they could provide an alternative to private cryptocurrencies like Bitcoin, which are decentralized and not backed by a government. CBDCs, on the other hand, would be issued and regulated by central banks, providing a level of oversight and stability that is currently lacking in the world of private cryptocurrencies. However, there are also some potential downsides to CBDCs. One concern is that they could further erode privacy and financial freedom, as central banks would have access to detailed information about how individuals are using the currency. Additionally, the introduction of CBDCs could also have an impact on the traditional banking system, potentially leading to a decline in the use of bank deposits and other financial products. Overall, the idea of central bank digital currency is an interesting one that deserves further exploration. While there are certainly potential benefits, it's important for central banks and policymakers to carefully consider the potential downsides and unintended consequences before moving forward. Ultimately, any decision to issue CBDCs should be made with the goal of promoting financial inclusion, stability, and security for all citizens.  The global economy had a rocky year in 2022. As the worst of COVID-19’s effects on public health receded, the war in Ukraine and China’s tough “zero COVID” curbs injected new chaos into global supply chains. Food and energy prices soared as inflation in many economies hit four-decade highs.

China’s reopening After nearly three years of punishing lockdowns, mass testing and border closures, China earlier this month began the process of unwinding its controversial “zero COVID” policy after rare mass protests. With draconian restrictions inside the country a thing of the past, China’s international borders are set to reopen from January 8. The reopening of the world’s second-largest economy — which has slowed dramatically during the last year — should inject new momentum into the global recovery. A rebound in Chinese consumer demand would give a boost to major exporters such as Indonesia, Malaysia, Thailand and Singapore, while the end of restrictions offers relief to global brands from Apple to Tesla that suffered repeated disruptions under “zero COVID”. At the same time, China’s rapid U-turn away from “zero COVID” carries significant risks. While Beijing has stopped publishing COVID statistics, hospitals across China have been flooded with the sick, while morgues and crematoriums have reported being overwhelmed with the influx of bodies. Some medical experts have estimated that China could see up to 2 million deaths in the coming months. With the virus spreading rapidly among China’s colossal population, some health experts have also expressed concerns about the emergence of new and more dangerous variants. “Barring this very disruptive opening up, I think that the market will do great,” Alicia Garcia-Herrero, chief economist for Asia Pacific at Natixis. “I would say once people see the end of the tunnel, so maybe the end of January, the end of the Chinese New Year, I would argue that’s when markets are really going to read a rapid recovery of the Chinese economy,” Garcia-Herrero added. “The other thing to watch is if there’s a major mutation, and mutations can be either less lethal but they could also be more lethal, and I think if the latter happens, and we start seeing closures of borders again, that would be traumatic for investor confidence.” Bankruptcies Despite the economic devastation wrought by COVID-19 and lockdowns, bankruptcies in fact declined in many countries in 2020 and 2021 due to a combination of out-of-court arrangements with creditors and large government stimulus. In the United States, for example, 16,140 businesses filed for bankruptcy in 2021, and 22,391 businesses did so in 2020, compared with 22,910 in 2019. That trend is expected to reverse in 2023 amid rising energy prices and interest rates. Allianz Trade has estimated that bankruptcies globally will rise more than 10 percent in 2022 and 19 percent in 2023, eclipsing pre-pandemic levels. “The COVID pandemic forced many businesses to take on substantial loans, worsening a situation of increasing dependence on cheap loans to make up for the loss of Western competitiveness due to globalisation,” Tziamalis said. “The survival of highly indebted businesses is now called into question as they face a perfect storm of higher interest rates, higher energy prices, more expensive raw materials and less consumption spending by consumers … It is also worth pointing out that the appetite of Western governments for any direct help to the private sector has been curbed by their increased deficits and prioritisation of support for households.” Fraying globalisation Efforts to roll back globalisation accelerated this year and look set to continue apace in 2023. Since its launch under the Trump administration, the US-China trade and tech war has deepened under US President Joe Biden. In August, Biden signed the CHIPS and Science Act blocking the export of advanced chips and manufacturing equipment to China — a move aimed at stifling the development of the Chinese semiconductor industry and bolstering self-sufficiency in chip making. The passage of the law was just the latest example of a growing trend away from free trade and economic liberalisation towards protectionism and greater self-sufficiency, especially in critical industries linked to national security. In a speech earlier this month, Morris Chang, the founder of Taiwan Semiconductor Manufacturing Company (TSMC), the world’s biggest chip manufacturer, lamented that globalisation and free trade are “almost dead”. “The West, and particularly the US, are increasingly threatened by China’s economic trajectory and respond with economic and military pressure against the emerging superpower,” Tziamalis said. “An outright war over Taiwan is highly unlikely but more expensive imports and slower growth for all countries involved in this trade war are a near certainty.”  The US Department of Commerce has labeled the Russian private military company Wagner Group a “military end user,” potentially restricting its access to any technology made with American equipment anywhere in the world. Undersecretary for Industry and Security Alan Estevez called Wagner “one of the most notorious mercenary organizations in the world” in a statement released to Reuters on Wednesday.

Wager has been under US sanctions since 2017, to little effect. Earlier this month, the State Department designated it an “entity of particular concern” with regard to religious freedom in Africa, putting it in the same category as Islamic State (ISIS), Al-Qaeda and the Taliban. In November, the State Department claimed Wagner was seeking to purchase drones from Iran, and labeled the group as part of the Russian defense sector. Commerce’s move falls short of the rumored designation of Wagner as a “terrorist” entity, advocated by some outspoken Democrats in Washington since this summer. Wagner was founded in 2014, and has mainly operated as a security contractor in Africa and the Middle East. More recently, its members have taken part in battles with the Ukrainian military in the Donbass.The group’s boss, Russian businessman Yevgeny Prigozhin, gave an ironic reaction to the news on Thursday. “Of course, this will create problems for the repair depot and ammunition supply for the triple-sevens. Oh, and also the HAWK AA. Lovely system, but breaks down a lot, unfortunately,” he said, referring to the M-777 howitzers and Raytheon’s anti-aircraft rockets that the US has supplied to Kiev’s military, with some presumably getting captured. “I hope that we will be able to order [parts] through Poland or the Baltic states, where we have close contacts with the defense ministries,” he added, needling the most anti-Russian NATO members. Prigozhin has trolled the Western media and governments on many occasions, including in November when he “admitted” to meddling in US elections with a movie quote, which most US and EU outlets rushed to report at face value.  Investors have withdrawn a record amount of digital coins from global cryptocurrency exchanges amid fears over the safety of their assets following the bankruptcy of major exchange FTX, data from analytics firm Crypto Compare shows. According to the report, 91,363 bitcoin was pulled out of centralized exchanges such as Binance, Kraken, and Coinbase in November. The tokens were worth roughly $1.5 billion based on last month’s average price of around $16,400.

“Bitcoin recorded the largest outflows from exchanges in its history... Since FTX, centralized exchanges have witnessed a string of outflows as market participants look to safeguard their funds,” Crypto Compare said. It is not clear from the report whether the funds are being sold or moved to private wallets. Data also showed that the outflow trend has continued in December, with 4,545 bitcoin withdrawn from centralized exchanges in the first seven days of the month, while the same period last year saw inflows of 3,846 bitcoin. The rush for the exits comes after FTX, a once major brokerage for trading crypto, filed for bankruptcy protection in mid-November. The company’s downfall left as many as 1 million FTX creditors with no access to their assets, dented investor confidence in cryptocurrencies and set off a chain reaction in the crypto market. In late November, another cryptocurrency lender, BlockFi, filed for bankruptcy. According to Bloomberg, over 130 FTX-affiliated entities have collapsed so far. Eric Robertsen, global head of research at Standard Chartered Bank, warned this week that the crypto market crisis will continue well into next year. “While the bitcoin sell-off decelerates, the damage has been done… More and more crypto firms and exchanges find themselves with insufficient liquidity, leading to further bankruptcies and a collapse in investor confidence in digital assets,” he told the Financial Times.  Russia wants its main agricultural lender Rosselkhozbank to be reconnected to the SWIFT financial network, in order to free up grain and fertilizer exports, Deputy Foreign Minister Sergei Vershinin said on Saturday.

“This is not the first time we are discussing this because, from my perspective, reconnecting Rosselkhozbank, which provides the majority of agricultural transactions, is a key issue… We have discussed this issue and received assurances again from the UN representatives that they also consider this issue to be vital,” Vershinin told reporters. His comments follow a meeting with senior UN officials on Friday, addressing the deal guaranteeing safe passage to Ukraine’s grain exports via the Black Sea. Under the pact, brokered in July by the UN and Türkiye, Russia sought a sanctions reprieve for its own agricultural trade, but has since voiced discontent with UN efforts to lift Western restrictions affecting the sector. While the sanctions do not directly target Russia’s agriculture, they affect payments, insurance and shipping. Many Russian banks were disconnected from the SWIFT financial messaging system earlier this year, making it difficult to carry out direct settlements for exports. According to Vershinin, one way to ease the problem would be to open correspondent accounts in foreign banks, such as Citibank and JPMorgan, to facilitate payments for Russian exports. “This option, if anything, can only be temporary, because the real solution is a full reconnection to the SWIFT financial messaging system of Rosselkhozbank,” he stressed, adding that the issue needs to be resolved before the grain deal expires on November 19. Vershinin noted that Moscow has not yet agreed to extend its participation in the deal. Previously, a number of top Russian top officials warned that the country could choose to exit the agreement, if the UN does not fulfil its pledges regarding Russian exports.  FTX founder Sam Bankman-Fried is shown testifying to a US House committee last December in Washington Failing cryptocurrency exchange FTX has begun moving assets offline, after more than $600 million in tokens was allegedly pilfered from the digital wallets on its platform. After filing for bankruptcy protection from creditors on Friday, FTX “initiated precautionary steps to move all digital assets to cold storage,” said Ryne Miller, general counsel for the firm’s US arm. “Process was expedited this evening to mitigate damage upon observing unauthorized transactions.”

However, considerable damage had already been done. According to an estimate by blockchain research firm Nansen, $662 million flowed out of FTX’s US and international exchanges. The firm’s main wallet, which was used to process withdrawals, was drained of its entire balance of 45.8 million FTT tokens, worth an estimated $97.2 million, Nansen said. A separate review by another analytics firm, Elliptic Connect, pegged the thefts at $473 million. The FTX community administrator on Telegram said the exchange had been hacked. FTX applications are infected with malware, according to the administrator, which also warned followers against loading the exchange’s website. The Bahamas-based FTX and about 130 affiliated companies commenced Chapter 11 bankruptcy proceedings on Friday in Delaware. The firm also announced that Democratic Party donor Sam Bankman-Fried had resigned as CEO. Bankman-Fried, who reportedly ranked behind only billionaire political activist George Soros in 2022 pledges to Democratic Party candidates, saw his entire $16 billion fortune wiped out this week, according to Bloomberg, which called the collapse “one of history’s greatest-ever destructions of wealth.” Miller, the general counsel, said the exchange was “investigating abnormalities with wallet movements related to consolidation of FTX balances across exchanges.” The financial troubles of major cryptocurrency hub FXT threaten to wreak havoc on crypto firms and transform how they’re run, JPMorgan strategists warned on Wednesday. According to a research note cited by Business Insider, the analysts believe this will likely send the price of Bitcoin down 25% to $13,000 a coin. Crypto players are likely facing demands from lenders to put up more collateral, and some may collapse under the pressure, the Wall Street strategists wrote. “It looks likely that a new cascade of margin calls, deleveraging and crypto company/platform failures is starting,” they said. The JPMorgan team pointed out to the close links between FTX and its boss Sam Bankman-Fried’s trading firm Alameda Research, and the wider crypto space. According to the report, Bankman-Fried, who had been heralded as the white knight of crypto, and even compared to Warren Buffett, now appears to be the one in need of rescue. “The number of entities with stronger balance sheets able to rescue those with low capital and high leverage is shrinking within the crypto ecosystem,” the strategists said. They indicated that the whole situation “creates a confidence crisis and reduces the appetite of other crypto companies to come to the rescue.” It could take several weeks for the crypto turmoil to settle down, unless FTX is quickly rescued, the experts suggested. “With the crypto market cap standing at just above $1 trillion before the FTX/Alameda Research collapse, our guess is that the crypto market will find a floor above $500 billion in the current deleveraging phase,” they said. On Wednesday, Bitcoin dropped to its lowest level in nearly two years on news of the potential bankruptcy of Bankman-Fried's company after the world’s largest crypto trading platform Binance abandoned plans to acquire FTX.  A deal for major cryptocurrency exchange FTX collapsed on Wednesday as bigger rival Binance said it was pulling out after doing due diligence on the proposed acquisition. Binance signed a non-binding agreement on Tuesday to buy FTX's non-U.S. unit to help cover a "liquidity crunch" at the rival exchange, but the deal was subject to further due diligence.

"As a result of corporate due diligence, as well as the latest news reports regarding mishandled customer funds and alleged US agency investigations, we have decided that we will not pursue the potential acquisition of FTX.com," Binance said in a statement. A representative for FTX did not immediately respond to a request for comment, but Chief Executive Officer Sam Bankman-Fried told employees in a Slack message viewed by Reuters that Binance had not previously expressed reservations about the deal. The turmoil over FTX has hit crypto prices. Bitcoin, the biggest cryptocurrency by market value, was last down 13% on the day at $16,277. FTX.com is also facing scrutiny from U.S. regulators over its handling of customer funds, as well as its crypto-lending activities.

This comes less than a month after the State Bank of India had agreed to put in place a simplified rupee settlement mechanism aimed at boosting mutual trade. An Indian diplomat told the outlet that Russian banks had requested that India’s eight largest lenders organize settlement in the local currency, but had not received any response. These banks include India’s largest lender, State Bank of India, and also Punjab National Bank, Bank of India, Bank of Baroda and Central Bank of India. Sources at lending institutions told the news agency that their management was not considering using this mechanism, at least not yet.

According to a senior executive at a large state-owned bank, financial entities are wary of being punished by the US and EU for trading in rupees with Russia. “They [Western nations] can impose a sanction on us, it will be a major business and reputational loss,” the banker said. Indian banks that are exposed to the international financial system stick to dollars or euros in trade with non-sanctioned Russian lenders. They are concerned that their businesses would be disrupted if targeted by sanctions. Currently, only two small lenders, Yes Bank and UCO Bank, which have agreements with Russia’s PSCB and Gazprombank, are using the rupee payment mechanism. In September, the Economic Times reported that Indian banks had received about 20 requests from Russian credit institutions to open accounts. The rupee trade initiative was set up to bypass the US dollar, thus ensuring uninterrupted cross-border business between the two countries. |

Thank you for choosing to make a difference through your donation. We appreciate your support.

Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed