The history of Russia and Ukraine is a complex and intertwined one that spans over a millennium. The two countries have been connected by cultural, religious, and political ties for centuries, but also marked by periods of conflict and rivalry. In this essay, we will explore the key events and turning points that have shaped the history of Russia and Ukraine.

Early history and Kievan Rus The earliest history of the region that is now Russia and Ukraine dates back to the 9th century, when a loose federation of Slavic tribes known as the Kievan Rus emerged in the area. The Kievan Rus were ruled by a series of princes, and Kiev became the center of a powerful state that extended from the Baltic Sea to the Black Sea. The Kievan Rus adopted Eastern Orthodox Christianity in the 10th century, which became a unifying force for the region. Mongol invasion and the rise of Moscow In the 13th century, the Kievan Rus was invaded by the Mongols, who destroyed Kiev and other major cities. The Mongol Empire ruled over the region for several centuries, but gradually declined, allowing the rise of the Grand Duchy of Moscow in the 14th and 15th centuries. Moscow gradually gained power and influence, and by the 16th century, it had become the center of a new Russian state. Expansion and imperial Russia Under the rule of Ivan the Terrible in the 16th century, Russia expanded its territories, conquering Siberia and expanding its influence in Central Asia. By the 18th century, Russia had become a major European power under the rule of Peter the Great, who modernized the country and expanded its territories even further. In the 19th century, Russia became an imperial power, colonizing Central Asia and parts of Eastern Europe. The Soviet era In 1917, the Russian Revolution overthrew the imperial government and established a communist government under the leadership of Vladimir Lenin. Ukraine, which had been part of the Russian Empire, declared its independence and established a republic. However, the new Soviet government quickly reasserted control over Ukraine and other parts of the former empire. Under Soviet rule, Ukraine and Russia were united as part of the Soviet Union, which became a superpower in the 20th century. The Soviet government imposed a system of collectivized agriculture and industrialization that transformed the economy, but also led to widespread famine and repression. Ukraine was particularly hard hit by the Soviet policies, which led to the deaths of millions of people in the 1930s. Post-Soviet era and current relations In 1991, the Soviet Union collapsed, and Ukraine declared its independence. Russia also underwent a period of political and economic upheaval, as it transitioned to a market economy and a democratic government. However, relations between Russia and Ukraine have been fraught with tension since the collapse of the Soviet Union. Ukraine has sought closer ties with Europe and the West, while Russia has sought to maintain its influence in the region. In 2014, a political crisis in Ukraine led to the ouster of President Viktor Yanukovych, who was seen as pro-Russian. Russia annexed Crimea, a region of Ukraine with a majority Russian-speaking population, and supported separatist rebels in eastern Ukraine. The conflict has led to thousands of deaths and ongoing tensions between Russia and Ukraine. Conclusion The history of Russia and Ukraine is one of complex relations, marked by periods of cooperation and conflict. The two countries have been connected by cultural, religious, and political ties for centuries, but also have different visions for their future. The current conflict between Russia and Ukraine is a reminder of the challenges that the two countries face in maintaining a peaceful and stable relationship.

0 Comments

Elon Musk has announced that starting April 15, only verified Twitter accounts will be eligible to be featured on the platform’s recommendation timeline. The tech mogul explained the move in a Twitter post on Monday, stating it’s “the only realistic way to address advanced AI bot swarms taking over.”

Apart from no longer being featured in other users’ ‘For You’ feeds, unverified accounts – those that have not paid the $7 monthly fee to have their account verified with a blue checkmark – will also lose the ability to vote in polls. Musk again explained the decision by pointing to the prevalence of bots on the platform. It is unclear, however, if Musk was only referring to polls created by Twitter and himself – as he often gauges public opinion on key decisions through this tool – or all polls on the platform. Twitter announced last week that it would remove the verified status of some ‘legacy’ accounts by April 1, meaning only those paying a monthly subscription will now have the blue checkmark in their profiles. According to analysts from Sensor Tower, Twitter currently has an estimated paying user base of just over 385,000 mobile subscribers worldwide on both iOS and Android. Critics of Musk’s algorithm change say it will significantly hinder the recommendation timeline’s relevance, as it will essentially prevent regular people from reaching a wider audience and only feature paying users, brands, and accounts of officials. Meanwhile, Twitter has been dealing with a source code leak, after an unknown hacker or group of people posted the code on GitHub – a software collaboration platform. Twitter has filed a court petition seeking to identify those responsible for the leak, arguing that the code, which underpins the website’s entire operation, could expose security vulnerabilities. Musk bought Twitter for $44 billion in late October 2022. After appointing himself CEO and vowing to transform the site into a free speech platform, the billionaire fired nearly three-quarters of Twitter’s workforce, removed some of its more contentious censorship policies, and restored a number of banned accounts, including that of former US President Donald Trump. However, he has yet to make the company profitable, as its value has decline by one half since the takeover, according to the Wall Street Journal, despite cutting the workforce and implementing a subscription model.  France saw its largest protest so far against President Emmanuel Macron’s pension reform on Thursday, with more than a million people taking to the streets across the country. The gatherings started peacefully, but were marred by violence in Paris and several other cities, as police used batons, tear gas and water cannons to disperse rioters, who hurled rocks and Molotov cocktails at officers, set up barricades, and vandalised public property. The French Interior Ministry said 1.089 million people took part in the ninth nationwide rally against the government’s plan to raise the retirement age from 62 to 64. According to official data, attendance doubled compared to March 15, the previous day of protests. The CGT confederation of trade unions claimed that the number of demonstrators on Thursday was far higher, totalling 3.5 million.

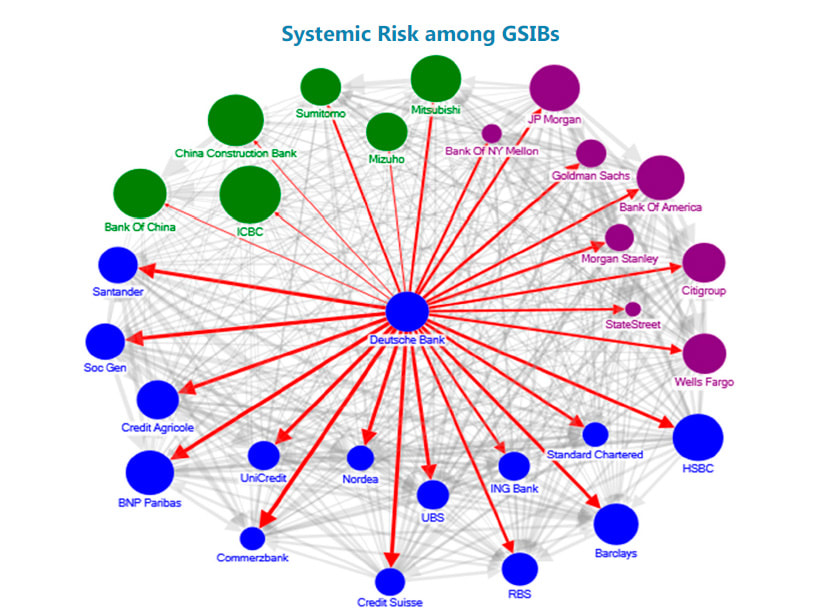

Violence and arrests Interior Minister Gerald Darmanin said on Friday morning that 457 people were arrested across the country, most of them in Paris, where 903 fires were lit on the streets. The scuffles saw 441 police officers injured, he said. There were reportedly dozens of wounded among the demonstrators, including a woman, who lost a thumb in the town of Rouen in Normandy. In his comments late on Thursday, Darmanin said the damage caused by the riots was more significant than on previous days. He singled out incidents in Bordeaux, where the entrance to the city hall was set on fire, and Lorient, where a police station was targeted. The minister blamed the chaos on some 1,500 “thugs, often from the far left, who want to bring down the state and kill police officers.” Those people are already known to law enforcement, he added. However, the deputy secretary general of the CFDT union, Marylise Leon, insisted that the “responsibility for this explosive situation lies not with the unions, but with the government.” The unrest is a result of “the falsehoods expressed by the president and his incomprehensible stubbornness,” she said. When is the next protest? The unions have called for the next – tenth – day of nationwide strikes and rallies against the pension reform to be held on Tuesday, March 28. The development could potentially distrupt a planned visit by Britain’s King Charles III, who is scheduled to travel to Bordeaux by train on that day. Speaking about future protests, which have been building momentum since January, Leon claimed that “the powerful social rejection of this project is legitimate and its expression must continue.” Pension reform Thursday’s huge turnout follows a decision by Macron’s government earlier this week to use executive privilege to pass the pension reform bill without a parliamentary vote. Despite fervent opposition and calls to resign, the president is insisting on raising the retirement age to 64 by the end of the year. He argues that failure to do so will cause the entire French pension system to collapse. Macron, whose ratings have slumped to below 30% since the onset of the crisis, said on Wednesday that he would always choose the future of the nation over short-term opinion polls, pledging: “If it is necessary to accept unpopularity today, I will accept it.” However, trade unions insist that the reform is “unfair” and mainly harms low-skilled workers with physically draining jobs and women with interrupted careers. One of attendees at Thursday’s rally claimed Macron’s plan was “a death sentence” for him.  Another bank is entering troubled territory amid the recent banking crisis that has spilled into global markets—this time in Germany.Deutsche Bank is facing fears of a collapse after shares dropped 11 percent on Friday morning, bringing those stocks down to a total of 29 percent since the bank chaos began on March 8. "We are still on edge waiting for another domino to fall, and Deutsche is clearly the next one on everyone's minds (fairly or unfairly)," Chris Beauchamp, chief market analyst at IG Group, told Reuters. "Looks like the banking crisis hasn't been entirely put to bed." Friday's stock market news is the latest development related to the fallout from the failure of Silicon Valley Bank (SVB) earlier this month, and the second involving a European bank. This week, Swiss bank Credit Suisse was rescued by rival UBS in a last-minute deal after Credit Suisse saw a plunge in share prices following the SVB collapse. Deutsche Bank's latest slump, driven partly by the Credit Suisse deal, signals that confidence in the banking system remains low. It marks the third week of decline for European banks, which fell 4.2 percent in the wake of the financial turmoil.

While many are worried it could be the next bank to collapse, other analysts have remained optimistic that it won't fall to the same fate as Credit Suisse. "We have no concerns about Deutsche's viability or asset marks. To be crystal clear - Deutsche is NOT the next Credit Suisse," research firm Autonomous said in a Friday report. German Chancellor Olaf Scholz has also dismissed the panic, saying that Deutsche Bank had "thoroughly reorganized and modernized its business model and is a very profitable bank," during a Friday news conference. In a Friday memo, JPMorgan strategists said that Deutsche Bank "had its own share of headline pressure and governance fumbles," but that it "still commands a relatively elevated cost base and has relied on its FICC (fixed income, currencies and commodities) trading franchise for organic capital generation and credit re-rating."

"Indeed, if there is anything depositors might learn from the past few weeks, both in the U.S. and Europe, it is just how far regulators will always go to ensure depositors are protected," JP Morgan wrote. Just a day earlier, Treasury Secretary Janet Yellen said the U.S. government was "certainly" prepared to take additional actions to stabilize banks—a shift in tone from her statements the day before, in which she said no such moves were being considered.  Russia is ready to increase settlements in yuan in its foreign trade, President Vladimir Putin said on Tuesday during talks with his Chinese counterpart Xi Jinping, who is in Moscow on a three-day official visit.

“We are for the use of Chinese yuan in settlements between Russia and the countries of Asia, Africa, and Latin America. I am sure that these forms of settlements in yuan will be developed between Russian partners and their counterparts in third countries,” Putin said. Two thirds of current trade between Moscow and Beijing is carried out in national currencies – the yuan and the ruble, the Russian president noted. China’s trade with Russia hit a record high in 2022, growing by nearly a third amid Western sanctions against Moscow. Bilateral trade is on pace to hit over $200 billion this year. The latest data from the Bank of Russia shows the yuan has become a major player in Russia’s foreign trade, with its share in the country’s import settlements jumping to 23% by the end of last year from only 4% in January 2022. The yuan’s share in export settlements also surged, from 0.5% to 16%.“It is important that national currencies are increasingly used in mutual trade. This practice should be further encouraged, and the mutual presence of financial and banking structures in the markets of our countries should be expanded,” Putin added. Meanwhile, the share of the US dollar and euro in Russia’s export settlements last year dropped substantially, from 65% in January 2022 to 46% in December. In February, the Chinese currency overtook the dollar as the most traded currency on the Russian stock market for the first time ever, according to data from the Moscow Exchange.  The merger between Switzerland’s two largest lenders, the embattled Credit Suisse and UBS, could have a negative impact on the entire Western bond market, Bloomberg reported on Monday, citing analysts.

UBS agreed on Sunday to acquire its rival, which was on the brink of insolvency due to the loss of investor and customer confidence, for 3 billion Swiss francs ($3.24 billion) in stock. The deal, brokered by the Swiss authorities, came with a 9-billion-franc government guarantee for potential losses from Credit Suisse assets and 100 billion francs in liquidity assistance from Switzerland’s central bank. However, as part of the deal, Swiss financial market regulator FINMA ordered Credit Suisse to write down to zero some 16 billion Swiss francs ($17.24 billion) of its Additional Tier 1 (AT1) bonds, with the aim of bolstering the bank’s capital and resolving its liquidity problems. AT1 bonds are a riskier form of bank debt, which were created in the wake of the global financial crisis of 2008, and represent a type of junior debt that allows banks to transfer risks to investors instead of taxpayers in cases of financial difficulties. Investors find them attractive as they pay higher interest due to the fact that they carry more risk than regular bonds. While bondholders will be left with nothing, Credit Suisse shareholders will receive $3.23 billion under the UBS deal, despite the fact that bonds traditionally stand above equities in the banking hierarchy. The situation has angered bondholders, Bloomberg reports, as they now fear the authorities in other countries may follow the Swiss government’s lead. “It’s stunning and hard to understand how they can reverse the hierarchy between AT1 holders and shareholders… Wiping out AT1 holders while paying substantial amounts to shareholders goes against all the resolution principles and rules that were agreed internationally after 2008,” Jerome Legras, the head of research at Axiom Alternative Investments, an investor in Credit Suisse’s AT1 debt, has said. “This just makes no sense… Shareholders should get zero… it’s crystal clear that AT1s are senior to stocks,” Patrik Kauffmann, a fixed-income portfolio manager at Aquila Asset Management, who also holds the bonds, said. Some analysts, however, argue that the write-off of the bonds is a logical step, as this is part of the reason they were created – as a way to impose losses on creditors instead of taxpayers in case of bank failures. Overall, experts predict that either the AT1 market will soon be closed for new issuance, or the bonds will surge in price because of the extra risk displayed by the Credit Suisse rescue merger.

2023 FORMULA 1 WORLD CHAMPIONSHIP CONSTRUCTOR STANDINGS

Chinese auto makers have embarked on a major expansion in the Russian market and are expected to reach a 60% share of total sales this year, the newspaper Izvestia reported on Monday, citing car-dealer chain Autodom.

According to the report, in the first half of 2022 the share of Chinese car brands in the Russian market stood at 3.7%, a figure that rose to almost 33% in the second half. Overall car sales in Russia last year decreased by 58.8% to 687,000 units, the Association of European Businesses (AEB) calculated. Chery, Haval and Geely were named the most popular Chinese car brands in Russia. Their share in the country’s market will continue to grow in 2023, according to the CEO of Autodom Andrey Olkhovsky. Meanwhile, the Association of Russian Automobile Dealers told Izvestia that it expects around 785,000 new car sales in Russia this year, of which at least 250,000 (32%) will be Chinese made. According to market expert Viktor Kondrashin, the lack of competition leads to an increase in prices for models such as Geely and Haval. He told the newspaper that “new models of Chinese crossovers currently cost the same as Volvo or Skoda two years ago.” .Kondrashin believes that domestic car prices could moderate when deliveries of automobiles from Iran start to arrive. The popularity of Chinese automobiles in Russia has been rising amid the exodus of European, American, and Japanese brands. Many automakers found it difficult to continue operations in the country due to logistical disruptions resulting from Western sanctions, particularly after deliveries of cars and spare parts to Russia were stopped.

2023 Formula 1 World Championship Drivers' Standings

FORMULA 1 STC SAUDI ARABIAN GRAND PRIX 2023 - Race Results

FORMULA 1 STC SAUDI ARABIAN GRAND PRIX 2023 - Top 10 Qualifying Results

* Grid penalty  Farmers movement BBB has become the largest party in all twelve Dutch provinces, according to the provincial results. Utrecht was the last province to get its results in. GroenLinks and BBB were neck-on-neck in the province, but BBB came out on top with 13.2 percent of the votes. GroenLinks is the second largest party there with 12.8 percent, followed by VVD with 11.9 percent, NOS and ANP report.

The turnout stood at 57.5 percent, higher than 2019’s already high 56 percent. According to the broadcaster, the turnout for this provincial election will likely be the highest since the late 1980s. Prime Minister Mark Rutte called the BBB’s massive victory “a very clear cry to politicians” and a “very clear relevant signal” from the voter. Rutte told ANP he does not yet know how to interpret this cry. He needs more time to think about it. Sixteen hours after the first results is too early for a “full-fledged analysis,” he said. To NOS, Rutte said he believes there is still support for his Cabinet. “We have a majority in parliament; there have been democratic elections.” The coalition already didn’t have a majority in the Senate, but losing more seats will still be a blow. Rutte wants to see how this plays out “In the coming days and weeks.” Results per province In Drenthe, the BBB got 33.5 percent of the votes, amounting to 17 seats in the Provincial Council - more than the total number of seats of the parties in places 2 to 7, according to the broadcaster. In Overijssel, the party got 31 percent of the votes. In the municipalities of Dinkelland and Tubbergen, BBB even won outright, getting more than half of the votes. In these two municipalities, the CDA - traditionally the farmers’ party - lost a lot of voters. The turnout in Tubbergen was also 16 percent higher than in 2019. In Limburg, BBB got 18.5 percent of the votes, here too, mostly at the expense of the CDA. Geert Wilders’ PVV, traditionally strong in Limburg, lost some voters but became the second-largest party with 12.7 percent of the votes. In Groningen, BBB got 23.6 percent of the votes. PvdA and GroenLinks are the second and third biggest parties in the province, each getting about 10 percent of the votes. CDA’s votes about halved, from 8.1 percent in 2019 to 4.1 percent this year. The other coalition parties also scored less well than in 2019. Friesland’s provisional results had the BBB with 27.9 percent of the votes. The PvdA is the second-largest party with 10.6 percent, followed by CDA with 8.7 percent. BBB got 23.8 percent of Gelderland voters' votes. The VVD is in a distant second place with 10 percent. PvdA is the third party with 8.8 percent of the votes. In Zuid-Holland, the farmers' party got 13.7 percent of the votes, beating the VVD's 12.9 percent. In 2019, the ruling party still got 15.7 percent of the votes. GroenLinks is the third largest party in Zuid-Holland with 9.7 percent of the votes, 0.6 percent more than in 2019. BBB got 14.2 percent of the votes in Noord-Holland, over a percentage point more than second-place VVD. PvdA and GroenLinks are the third and fourth largest parties in the province. Together, the two left-wing parties are larger than the BBB. In Noord-Brabant, the farmer's movement got 18.2 percent of the votes. VVD is the second largest party, with 14.1 percent of the votes. BBB will get 11 of the 55 seats in the Provincial Council, the VVD 9. GroenLinks is the third largest party, with 7.7 percent of the votes and five seats. In Flevoland, BBB got 20.8 percent of the votes. VVD came in second largest with 9.9 percent of the votes, followed by the PVV with 7.7 percent, PvdA with 7.6 percent, and GroenLinks with 6.9 percent. And in Zeeland, the BBB is the largest party with 19.7 percent of the votes, pushing the CDA from its throne. Left-wing combination GroenLinks/PvdA is the second largest party with 13.4 percent, followed by the SGP with 12.5 and then CDA with 11.4 percent. Eerste Kamer This was the BBB’s first time participating in the provincial elections, and its massive victory translates into 16, maybe 17 seats in the Eerste Kamer, the Dutch Senate, according to a prognosis by ANP on Thursday afternoon. The left-wing bloc PvdA/GroenLinks is projected to get 15 seats. The two parties had separate electoral lists but will form one faction in the Senate. The biggest loser in this election was FvD, who won 12 seats in the 2019 elections and only 2, maybe 3, in this one. Though due to infighting and split-offs, the FvD currently only has one actual seat in the Senate, so even with the much fewer votes, it may be considered a win. All four coalition pirates - VVD, D66, CDA, and ChristenUnie - lost seats. For many voters, dissatisfaction with the current Cabinet motivated their choice to vote for someone else, according to an online poll by Ipsos.  Following a stint with Demi Lovato in 2022, guitarist Nita Strauss has returned to Alice Cooper's band, which will be hitting the road in late April for a series of 2023 North American tours. "From the studio to the stage, it's always an immense honor to make music with Alice Cooper! I'm very excited to be rejoining the band on the road for the 2023 dates, and so I'll see you on the road in April. Let the nightmare return," Strauss said in a press release.

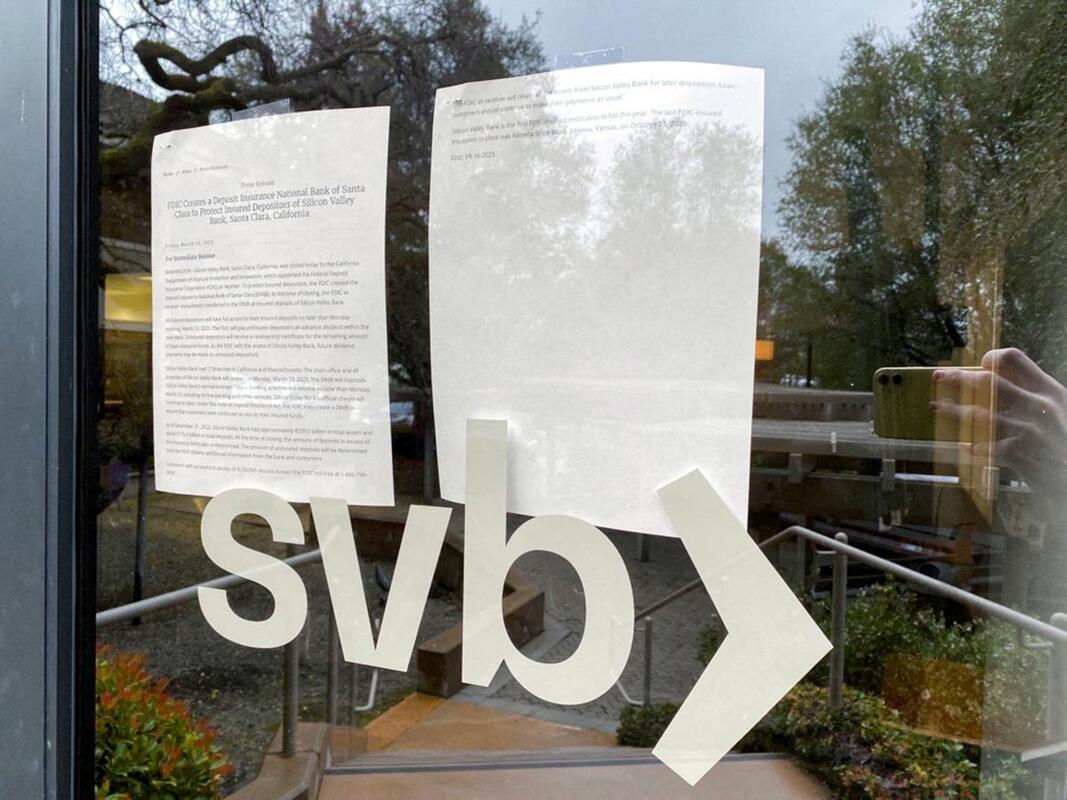

"She's Back! " Nita asked for a leave of absence to work with someone else, something I always encourage my band members to do. I like them to challenge themselves and try new things," Cooper added. "I'm thankful to my old friend Kane Roberts for stepping up and filling in for her, but she'll be back with us for the new tour that starts up in late April. It's going to be great to have her back." Strauss announced her departure from Cooper's band last July, and revealed shortly after that she was joining Lovato on tour in support of the singer's 2022 album Holy Fvck. The guitarist had been playing with Cooper since 2014, but he expressed his full support of her decision to change gears. "[Alice and Sheryl Cooper] hugged me and were so happy and gave their absolute blessing," Strauss recalled during a Loudwire Nights interview. "Alice said, 'We're so proud of you. Go out, shine your light, have a great time and we'll see what happens for next year.' There was never a, 'Hey, I quit, goodbye, thanks for everything.' It was just, 'I'm gonna take a step back, try something different for a few months and we'll regroup and see what happens.'" As a result, Roberts reunited with the shock-rocker after 34 years and played on his fall 2022 tour. Cooper will embark on a headlining tour starting April 28 in Mt. Pleasant, Mich. The run wraps up with a May 20 performance at the Welcome to Rockville festival in Daytona Beach, Fla., and then the shock rocker is set to play a handful of dates with Motley Crue and Def Leppard in August. Later that month, he'll head out for a co-headlining tour with Rob Zombie, which will conclude in late September. Well, well, well, it seems the collapse of Silicon Valley Bank (SVB) has brought a certain individual back into the spotlight. Joseph Gentile, the bank’s Chief Administrative Officer, has been making headlines due to his past involvement with Lehman Brothers, the global finance firm that famously went bankrupt during the 2008 financial crisis. Yup, you read that right, the same guy who used to be Lehman Brothers’ Chief Financial Officer (CFO) is now at the center of attention in the SVB debacle.

SVB, once the premier financial institution for tech and health startup businesses in the US, has been in a rapid downward spiral since Friday, with customers starting to withdraw their deposits due to the bank’s investments being adversely affected by recently hiked interest rates.This led to California regulators handing over control of the bank to the Federal Deposit Insurance Corporation (FDIC) and a bid for its assets now underway. Ouch. But back to Gentile. Twitter has been abuzz with comments and takes on his involvement with SVB, with some likening the bank’s collapse to the 2008 crisis, while others have taken a more humorous approach. “Just in case you thought you were bad at your job, Silicon Valley Bank’s Chief Administrative Officer Joseph Gentile was the former CFO of Lehman Brothers,” tweeted Stock Talk Weekly. Neither Gentile nor SVB has commented on the situation, leaving many to speculate on what led to the bank’s downfall and what this means for the tech and health startup businesses it once served.Alf (not that Alf), the founder of The Macro Compass, had some pretty harsh words for the way they’ve handled things. Spent hours going through SVB’s financial statements and changed my mind on the topic. “These guys weren’t bad at risk management. They were outright horrific. They literally gambled billions away,” he said on Twitter. Either the level of incompetence was extreme, or a gigantic amount of moral hazard was at play. I think the latter, and if I am right this is really f*cked up.”  It is early days yet to assess if the collapse of Silicon Valley Bank (SVB) will turn out to be a Lehman moment for the global financial system. SVB’s failure was triggered by factors different from the ones that precipitated the Lehman collapse or for that matter, India’s bad loan crisis. If those crises were about banks piling on credit risks on their loan books, SVB’s failure can be traced to mis-management of rate risks in its investment book.

Running an asset-liability mismatch to earn a spread is central to any banking business. But SVB stretched this concept much too far in deploying its copious deposit flows into long-dated treasuries and mortgage securities, which it parked mainly in its held-to-maturity (HTM) portfolio. As inflation rose and the US Fed raised interest rates by 450-475 basis points, SVB’s portfolio racked up large losses. The advent of the funding winter, which prompted start-ups to draw down their deposits, forced SVB to liquidate not just its Available For Sale bonds but also its HTM ones. The resulting $1.8 billion write-off followed by a failed attempt to raise capital, spooked the closely-knit start-up community to launch a run on SVB’s deposits. When interest rates shoot up in a short span, no bank can shield its investment book from losses. But SVB was more vulnerable to a run than a vanilla bank, because of its over-reliance on big deposits from a closed ecosystem — start-ups, their founders and VCs. The Federal Deposit Insurance Corporation has been quick to take over SVB, halting the run. But its ability to shore up dented depositor confidence in US banks, may depend on whether SVB’s uninsured depositors (who make up 90 per cent of its $175 billion book) will need to take haircuts. To prevent a snowballing effect on the start-up ecosystem, SVB’s clients may need to be thrown a liquidity lifeline to meet emergency payouts. As SVB had limited inter-linkages with other banks, a contagion effect on the US or global banking system from its failure, appears unlikely. But its collapse does call for stricter regulatory vigilance on other counts. With the previous crisis stemming from lending, the current global regulatory framework for banks focusses a lot on proactive accounting of bad loans and stress-testing their impact on capital adequacy. But the SVB crisis highlights that in a scenario of rapidly rising rates, banks’ investment books need an equal degree of scrutiny and stress-testing. The present expedient of allowing banks to sweep their bond losses under the carpet by owning large HTM portfolios, can lead to blow-ups. In India, the RBI may need to scrutinise bank books for depositor concentration. The SVB saga also offers a salutary lesson to global central banks that when they switch from extended ultra-loose monetary policies to uncalibrated, sharp rate hikes to quell inflation, they can inflict damage not just on growth, but also on financial system stability that they strive so hard to protect. |

Thank you for choosing to make a difference through your donation. We appreciate your support.

Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed