|

The World Economic Forum just had their Davos Agenda 2021 meeting in January. Now The Great Reset has been something talked about in detail since the pandemic started. But are we seeing The Great Reset happening right before our eyes? I think we are starting to see the slow implementation of The World Economic Forum's Great Reset right now. It's like a chess match, nothing happens right away, many moves are made before the endgame.

The Great Reset that was proposed by the World Economic Forum is looking to forgive all the world's debt and has us live by the slogan, "You'll Own Nothing, And You Will Be Happy". Now first and foremost, we are starting to see a slow implementation of a universal basic income. It was actually what the World Economic Forum talked about and advocate for in the Davos agenda 2021 meeting that happened a few weeks back. Starting with the continual stimulus packages that we have received in the past few months to help stimulate the economy, seems like a slow inoculation into government dependency. Since we can't work where are we going to get our money from? Secondly, The Great Reset talks about how having ALL of our debts forgiven. Well who's going to buy them? The Federal Reserve? Sure, but with the sale of debt, comes the control of the debt. And whoever controls debt, controls YOU! The great reset is all about debt forgiveness but then we won't be able to own anything ever again......and we will be happy about it. I'm not completely convinced that the World Economic Forum is looking to do this for the good of the people. They literally said, "You'll Own Nothing and Be Happy" about it. Would you like to NOT own your home, car, business? I sure would like to own all of the things I've worked very hard for and I can speak on behalf of most people who own those things. Lastly, the Davos agenda 2021 got into cryptocurrency. Currently crypto is decentralized and lacks certain regulation from major regulatory bodies. That is a beautiful thing, but the World Economic Forum has already spoke about crypto in their Davos agenda 2021 meeting that happened a few weeks back. With the Great Reset, the fiat currency will crash because of the reckless printing from The Federal Reserve. So expect to see heavy regulation and government intervention with crypto.

0 Comments

There is a very worrying trend that has been accelerated under the veil of fear and confusion, and that trend has been drastically intensified…

The corona crisis has already taken a very high toll and caused deep damage in our societies and our economies, the extent of which is yet to become apparent. We have seen its impact on productivity, on unemployment, on social cohesion and on political division. However, there is another very worrying trend that has been accelerated under the veil of fear and confusion that the pandemic has spread. The war on cash, that was already underway for almost a decade, has been drastically intensified over the last few months. The “problem” Over the last years, and as the war on cash escalated, we’ve gotten used to hear certain arguments or “reasons” on why we should all abandon paper money and move en masse to an exclusively digital economy. These talking points have been repeated over and over, in most western economies and by countless institutional figures. “Cash is used by terrorists, money launderers and criminals” is arguably the most oft-repeated one, as it’s been widely employed in most debates about the digital transition. Just a couple of years ago, it was also used by Mario Draghi, to support the decision to scrap the 500 euro note. We didn’t get any specific information or data about how many terrorists were actually using this high-denomination note, but we do know a lot of law-abiding citizens were using it to save, as did small business owners for their operational liquidity needs. Now, however, the corona crisis has introduced a whole new direction of anti-cash rhetoric and fresh arguments in favor of a digital economy. Even in the early stages of the pandemic, when essentially nothing was concretely known about the virus itself or its transmission, the seeds of new fears were already planted by sensational media reports and fear-mongering political and institutional figures. The insidious idea that “you can catch Covid through cash” might have been prematurely spread, but it did stick in most people’s minds. This is, of course, understandable, given the extremely high levels of uncertainty and anxiety in the general public. Wanting to eliminate potential threats was a natural instinct and so was the urge to take back at least some control over our lives, after they’d been suddenly thrown into utter chaos in the wake of the global economic freeze. Another factor that concretely helped the shift away from physical cash was an entirely practical one. Given the lockdown measures and the new “social distancing” directives that were enforced all over the world, it became difficult to use cash, even if you really wanted to, or had no other means of transaction, as is the case for billions of people. With physical stores being forced to shut down and with more and more online shops offering contactless delivery (either as a choice or as a service requirement), the need for cash very quickly gave way to digital payments. For most of us, who have access to online banking, cards or other digital payment services, this introduced no real inconvenience and we probably didn’t even give it a second thought. However, for many of our fellow citizens it was a serious impediment, which in some cases blocked their access to basic goods and essential supplies. Contrary to the glowing promises of the digital economy, of financial inclusion and convenience, the fact remains that there are still millions of people who simply do not have access to this brave new world. According to figures by the World Bank, globally there are 2.5 billion people with no bank account, with a high concentration in the developing world. In the West too, however, there is a very large part of the population that is unbanked and/or has no access to digital solutions, while the elderly are also to a very large extent “locked out” of the digital economy. For all these millions of people, cash is the only way to save, to transact and to cover their basic needs. The “solution” With cash being presented not just as a danger to society and to national security, but also as a direct health hazard due to the coronavirus, the push towards digital alternatives has been massively reinforced over the last few months. Both international organizations and individual governments have actively participated and encouraged this push, some through public guidance statements and others through the blunt enforcement of direct rules and measures that leave no real room for their citizens to make their own choices. The CDC in its official guidance to retail workers recommenced that they “encourage customers to use touchless payment options”, while a report by the Word Bank highlighted the need to adopt cashless payments for the sake of “social protection”. The UAE Central Bank encouraged the use of online banking and digital payments “as a measure to protect the health and safety of UAE residents”, and the Bank of England has acknowledged that banknotes can hold “bacteria and viruses” and recommended that people wash their hands after handling money. In March, a report from Reuters revealed that the U.S. Federal Reserve was quarantining dollars that it repatriated from Asia and so did South Korea’s central bank, while banks in China were forced by the government to disinfect bills and keep them in a safe for up to 14 days, before putting them in circulation. A highlight, however, came in May, when the World Economic Forum published an article in its “Global Agenda” strongly supporting the mass adoption of digital payments, for the sake of public health. In it, the authors argue that “contactless digital payments at the point of sale, such as facial recognition, Quick Response (QR) codes or near-field communications (NFC), can make it less likely for the virus to spread to others through cash exchanges.” They also applauded the efforts of China in digitalizing payments and appeared to hold the country and its measures as a model to be emulated: “China’s path to enabling digital payments should provide some lessons to other countries eager to follow suit.” Since a number of Western governments may indeed be “eager to follow suit”, let us take a closer look at this bright example and examine what it really entails. Fiat money 2.0 The digitalization drive in all aspects of the Chinese state, society and economy is nothing new and it certainly predated the emergence of Covid-19. The country’s infamous “social rating system” has made headlines years ago and the government’s eagerness to use technology, the internet and all sorts of digital systems to track its citizens’ behaviors and affiliations has long attracted International criticism and widespread condemnation by human rights organizations, privacy advocates and free speech supporters. Now, however, the state has been given a reason to accelerate its efforts in the mass adoption of digital payments and the abandonment of cash. To a large extent, this digitalization of payments task was much easier in China, as digital payments there are already very widespread in the population. More than 80% of consumers already used mobile payments in 2019, according to management consultancy Bain, a sharp contrast with the US that had adoption rates of less than 10%. So, as the population has already accepted a new way of payment, the new initiative sought to dominate the means of payment too. Thus, a new “digital yuan” was introduced. This new fiat currency, that has been in development for over 5 years, was rolled out in April in four Chinese cities with a plan for national adoption soon, so that it eventually replaces the physical legal tender. This so-called Digital Currency Electronic Payment (DCEP) will be put into circulation through China’s big four state banks and citizens will be able to receive and use it by downloading an electronic wallet application authorized by the People’s Bank of China (PBOC), which will be linked to their bank account. On the surface, it appears to work just like the old currency. It is issued and backed by the PBOC, it’s valued the same as the physical banknotes and, thanks to partnerships with Alipay and WeChat Pay, that control 80% of the country’s payment market, it will be used to get paid by anyone and to pay for anything. In fact, some public servant salaries and state subsidies are already being paid out in this new digital yuan, arriving in their intended recipients’ digital wallets. According to China’s state media People’s Daily, the new currency is meant to simplify domestic transactions and trade, but it will also facilitate and ease cross border transactions. The implication there is clear: It is yet another attempt to challenge the global dominance of the USD, after the Belt and Road initiative failed to really move the needle as the Chinese state had hoped. The strategy of spending of huge amounts of Chinese money abroad did provide some leverage over developing countries, but it didn’t come anywhere near “dethroning” the Dollar and internationalizing the Renminbi. Perhaps, this initiative will fare better, especially as it now has the “first-mover” advantage. Entering this “digital fiat” arena first is hugely important and the timing of the currency’s launch was no coincidence. The development and the rollout plan were significantly accelerated following Facebook’s announcement of the Libra, as the Chinese state wouldn’t have the private tech giant beat them to the punch. In fact, the digital yuan resembles the Libra in many ways. Most importantly, neither of them is a cryptocurrency, which is decentralized by design and allows for peer to peer transactions without the need of an intermediary or third party. In this case, the issuer is the third party and all transactions go through a very centralized system that controls and has access to all the data. In another non-coincidence just a few years back, China’s government banned initial coin offerings and placed great burdens on cryptocurrencies and crypto-investors making it very hard to operate in the country, thereby dismantling the threat of potential competition from the private sector and clearing the way for its own digital coin.  The head of China’s central bank is calling for countries to replace the U.S. dollar as an international reserve currency with something called SDRs. Created by the IMF way back in 1969 for that purpose, SDRs never caught on. While SDRs may be declared an official international reserve asset today, they are not likely to become the world’s key international currency anytime soon. In the meantime, countries in China’s current predicament—acquiring more dollars than they think prudent—could avoid such risks in the future by allowing their currencies to appreciate.

Yi Gang, governor of the Bank of China, wants a new international reserve currency, one that is “disconnected from economic conditions and sovereign interests of any single country.” He claims that credit-based national reserve currencies, like the dollar, are inherently risky, facilitate global imbalances, and foster the spread of financial crises, but China’s concerns may also be a bit more parochial. The country holds a huge portfolio of dollar-denominated assets that could incur valuation losses, if recent U.S. actions to limit financial turmoil and stimulate the economy generate inflation and dollar depreciation. The People’s Bank of China has offered a fix to the dollar problem. They recommend supplanting the reserve-currency role of the U.S. dollar with Special Drawing Rights (SDRs), a composite currency issued by the International Monetary Fund (IMF). Others, including Nobel Prize winner Joseph Stiglitz and a U.N. panel of experts, have endorsed the idea. Adopting the SDR as an official international reserve asset may be technically feasible and it could conceivably occur fairly quickly, but substituting the SDR for the dollar more broadly as the world’s key international currency will not happen anytime soon. People reap substantial economies from conducting cross-border commerce in dollars, and until the SDR matches these benefits, central banks will still need dollars. In the interim, countries that want to limit their exposure to credit-based reserve currencies, like the dollar, might simply allow their currencies to appreciate. Something Old, Something New Complaints about the dollar and a fascination with SDRs are not new. The IMF created SDRs as an international reserve currency in the late 1960s to solve problems, similar to Dr. Zhou’s concerns, which rose out of the Bretton Woods fixed-exchange-rate system. Although Bretton Woods was at its heart a gold-based currency arrangement, the U.S. dollar quickly emerged as the key international currency, both for financing international commerce and as an official reserve currency. Today, as during Bretton Woods, countries accumulate foreign exchange when they prevent or limit the appreciation of their currencies in the face of persistent trade surpluses and foreign financial inflows. Once acquired, official reserves then provide these countries with a buffer stock that they can draw down to mitigate the disruptive economic effects of unexpected trade shortfalls and temporary outflows of foreign funds. Absent such reserves, these countries would either have to allow their currencies to depreciate or quickly tighten their monetary policies, but such abrupt adjustments could be disruptive and might not be compatible with these countries’ current goals for inflation or real economic growth. At its heart, the desire to acquire and hold official foreign-exchange reserves reflects a desire to prevent, or at least limit, exchange-rate adjustments. About 15 years into the Bretton Woods era—just like today—many countries began to view their holdings of official U.S. dollar reserves as excessive, and they worried that the United States might be forced to devalue the dollar. A dollar devaluation would saddle these countries with foreign exchange losses, since a devalued dollar would buy less abroad. As the situation unfolded, some countries, led by France, sought to replace the dollar with a reserve currency unrelated to a single national currency, if not solely related to gold. The IMF—then the guardian of the Bretton Woods parity grid—came up with the SDR. The IMF initially defined the SDR in terms of a fixed amount of gold, then equal to one dollar, and allocated 9.3 billion SDRs between 1970 and 1972 to member countries in proportion to their quotas in the IMF. Before the SDRs even hit the shelf, however, President Nixon threw a wrench in the Bretton Woods works. He closed the U.S. gold window on August 15, 1971, refusing thereafter to convert dollar reserves into U.S. gold. Countries holding dollars were stuck. By March 1973, the large developed countries had all allowed their currencies to float against the dollar, ending their need to acquire dollar reserves. With the advent of floating exchange rates, the IMF redefined the SDR as a weighted average of the U.S. dollar, the British pound, the Japanese yen, and the currencies that eventually comprised the euro. The dollar has the largest weight, currently about 40 percent, so changes in the dollar impact the SDRs more than similar changes in the pound, yen, or euro. Because of its construction, however, the SDR will likely be more stable relative to other currencies than the dollar; so, holding a portfolio of SDRs is liable to present a country with less exchange-rate valuation risk than holding dollars. While many in the late 1960s and early 1970s believed that the SDR would supplant reserve currencies and possibly even gold in official portfolios, the SDR basically died at birth. The IMF made a second allocation of 21.4 billion SDRs between 1979 and 1981, again in proportion to member countries’ quotas, but the SDR quickly devolved for the most part into a unit of account, primarily on the IMF’s books, as the large developed countries accepted floating exchange rates as the norm. If countries are willing to allow their exchange rates to adjust freely to trade flows and to cross-border movements of financial funds, they do not need official foreign-exchange assets. Despite the widespread acceptance of floating exchange rates, however, no country—including the United States—has completely tossed out their portfolio of foreign-exchange reserves. They keep some around just in case they may sometimes want to support their exchange rates. In doing so, they accept that the exchange value of these reserves will fluctuate from time to time. The Dollar The reserve currency of choice is the dollar (figure 1). The IMF estimates that 64 percent of the world’s official foreign-exchange reserves are held in dollar-denominated assets. The euro, the second most widely held international reserve currency, lags well behind, followed by the British pound and Japanese yen. These currencies’ rankings as official reserves parallel their status in international commerce more generally. This correlation should be of no surprise. Why hold a currency that no one uses?  What are the risks with Bitcoin? Bitcoin is the first and most valuable cryptocurrency and it has seen massive growth in 2017. But many people are warning about the risks associated with Bitcoin. A number of high-profile investors regard Bitcoin as a ‘bubble’ or ‘mirage’, and expect the market to crash, like the dot-com bubble. Others highlight that cryptocurrencies like Bitcoin help to enable financial crime and funding of terrorism, due to the level of anonymity that digital currencies can provide to technologically adept criminals.

It seems like everybody is talking about cryptocurrencies at the moment. With apps like Coinbase making it possible to buy and trade cryptocurrencies at the tap of a button, thousands of people – from political idealists to economic opportunists – have been jumping on the crypto investment bandwagon. Cryptocurrencies are creeping into the mainstream, with even Goldman Sachs recently announcing their plans to start trading Bitcoin. 2017 saw the asset value of Bitcoin boom, amidst growing confidence in the first and most important cryptocurrency. Many cryptocurrency investors have seen the growth of Bitcoin as a win-win situation for all concerned. But are crypto-investors inadvertently paying into a system that is making the world less safe, and putting us all at risk? Since its early days, Bitcoin has had its share of ties with criminal activity. With the increased level of anonymity that it provided, Bitcoin was a popular currency on the darknet marketplace the ‘Silk Road’, where it was used chiefly to trade illegal drugs, as well as other contraband. As it crawls towards the mainstream, Bitcoin has certainly shaken off some these negative associations. But the fact remains that crypto transactions continue to afford criminals with a veil of anonymity, enabling them to evade justice – and enabling the financing of all manner of malicious activities. The problem is that, unlike conventional currencies, cryptocurrencies are decentralized, and therefore not subject to the same regulations, reviews, and monitoring as in financial institutions or banks. This means that potential criminal transactions that are processed in cryptocurrency bypass the regulatory controls that banks are legally required to perform. Jargon buster Bitcoin – a digital cryptocurrency and payment system. It is a decentralized digital currency, as it operates independently of a central bank. Cryptocurrency – a digital asset designed to function as a medium of exchange. Encryption techniques are used to regulate the generation of units of currency and verify the transfer of funds. Bitcoin is the first, and, at present, the most valuable cryptocurrency. Blockchain – an encrypted ledger which records the history of cryptocurrency transactions Bitcoin and terrorist funding Amongst the criminal organizations that are benefitting from unregulated cryptocurrency transactions are ISIS. In a PDF circulated on social media, entitled “Bitcoin and the Charity of Violent Physical Struggle”, one ISIS supporter explains, “This system has the potential to revive the lost sunnah of donating to the mujahideen, it is simple, easy, and we ask Allah to hasten it’s (sic) usage for us”. As academics from Macquarie University have highlighted, the utility of crypto for helping to fund ISIS terrorist operations is significant. Ghost Security Group, a hacktivist and anti-terrorism group, claimed to have identified a chain of transactions to Bitcoin wallets believed to be owned by ISIS which contained funds between $4.7m and $15.7m – between one to three percent of their estimated annual income. The group stated to news network NewsBTC that ISIS is “extensively using Bitcoin for funding their operations”. In 2015, German media company Deutsche Welle reported that one Bitcoin wallet believed to belong to ISIS received around $23m within a single month. The latest vault reporting data from the London Bullion Market Association (LBMA) in London, which is now released on the 5th business day of the month, claims that as of the end of March, there were 1.25 billion ozs (38,859 tonnes) of silver in the LBMA London vaults, which would be an 11% increase on the total claimed to be held in those vaults at the end of February. To put this into perspective, that’s an extra 3,863 tonnes that the LBMA claims has arrived into its vaults in London during March, or an extra 124.2 million ozs. That’s nearly as much silver claimed to be added by the LBMA during March, as the Sprott Physical Silver Trust PSLV holds. (PSLV holds 130.97 million ozs of silver).

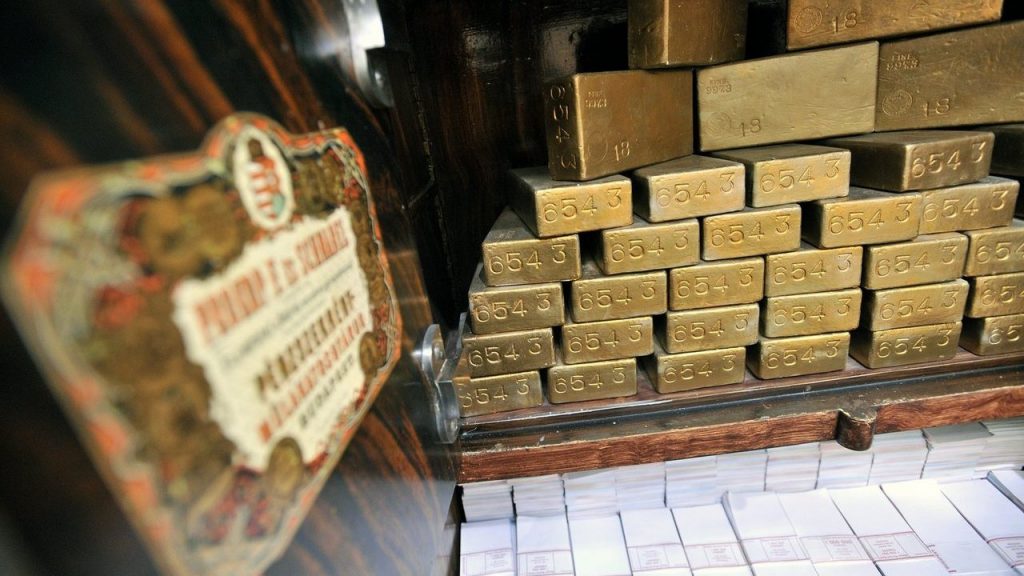

Said another way, 3863 tonnes added to the London LBMA vaults during March would be 124,200 wholesale silver bars (each bar weighing about 1000 ozs). These 124,200 bars are stored 30 bars per pallet. This would be 4,140 pallets extra pallets of silver bars. Usually these vaults store pallets of silver 6 pallets high. That would be 690 extra towers of pallets, each 6 pallets high. It would mean that 193 containers (each allowed to carry a maximum of 20 tonnes) arrived at the London vaults during March, or over 8.4 containers on average per day, every business day, and that the vault staff had to move and store 180 pallets each day. All of this in an environment where everyone from refiners to Mints to wholesalers to bullion retailers are reporting availability issues in sourcing physical silver bars right now. Seems plausible, right? And this LBMA vault data does not even break down how much each of the LBMA London vaults of JP Morgan, HSBC, Brinks, Malca-Amit, Loomis, and ICBC Standard, claim to hold. Which is why, if the LBMA vault data on silver (and gold) is to be even remotely trusted (which is a far stretch), then it is now time to independently and physically AUDIT THE LBMA VAULTS. Not that this will ever happen given that the LBMA is run by the bullion banks which run the paper silver and gold markets. But it needs to happen. More info @ https://www.lbma.org.uk/prices-and-data/london-vault-holdings-data  Gold bars in the Central Bank of Hungary’s vaults in Budapest The central bank of Hungary, the Magyar Nemzeti Bank (MNB), has just announced a purchase of a massive 63 tonnes of Good Delivery gold bars, and in doing so tripled the nation’s gold holdings from 31.5 tonnes to 94.5 tonnes. In its press release about the huge transaction, published April7, 2021, the Hungarian central bank explains its rationale for the dramatic purchase of what is approximately 5040 large (400 oz) gold bars, highlighting that gold has no credit risk and no counterparty risk, and so reinforces sovereign trust over all economic environments (normal and extreme), while being one of the most crucial reserve assets that a central bank can hold.

From 10 Fold to 30 Fold For those who may remember, this is not the first major gold purchase by the Hungarians in recent times, as the Hungarian central bank also caused shockwaves in October 2018 when it purchased 28.4 tonnes of gold, on that occasion increasing its gold reserves 10 fold from 3.1 tonnes of 31.5 tonnes, or a 1000% increase. This means that over exactly two and a half years, the Hungarians have increased their sovereign gold reserves by a staggering 3000%, or 30 fold, from 3.1 tonnes to 94.5 tonnes, an absolute increase of 91.4 tonnes. How’s that for a conviction trade? On the October 2018 occasion, the Hungarians purchased their 28.4 tonnes of gold at the Bank of England in London, and repatriated it back to Hungary in the same month, announcing the purchase and the repatriation at the same time, saying that ‘the repatriation has already taken place‘. On this occasion, the MNB does not say where it bought its 63 tonnes of gold, but it may well have been again at the Bank of England in London. Nor does the MNB say if the 63 tonnes of gold has been repatriated to Hungary yet. However, going on the previous pattern from 2018, one would expect that yes it has been brought back to Hungary by plane and under heavily armed guard. A No Confidence Vote in the System Interestingly, this time around in 2021, the Magyar Nemzeti Bank says that part of the motivation for the new gold purchase is in “managing new risks arising from the coronavirus pandemic”, which is a subtle way of saying that since central banks and governments around the world have used the Covid excuse to ramp up debt levels, ramp up quantitative easing and ramp up money supply growth, therein debasing their fiat currencies and introducing inflationary risks to bond holders, the Hungarians are simultaneously ramping up their physical gold holdings to counter this insanity. Or said in the diplomatic language of the latest Hungarian central bank press release, these concerns “further increase the importance of gold in national strategy as a safe-haven asset and as a store of value.”

The finest known 1822 Half Eagle gold coin set a new world record when an anonymous bidder snatched it up at a Las Vegas auction last Thursday for $8.4 million. “The 1822 Half Eagle is now the most valuable gold coin minted by the United States ever sold at auction. It’s also now the third-most valuable coin ever sold at auction,” said Brian Kendrella, the president of Stack’s Bowers Galleries. Exactly 17,796 of these $5 coins were minted, but only three specimens are known to have survived. The record holder is the only one owned by a private individual. The other two are permanent residents of the National Numismatic Collection in the Smithsonian Institution. The privately owned specimen was first acquired by Virgil Brand in 1899 and remained in his vast collection until it was sold by his heirs in 1945.

At that time, it entered the unparalleled collection of Louis E. Eliasberg, Sr., who had the distinction of successfully assembling a complete set of every U.S. coin ever minted. When the gold coins from the Eliasberg Collection were auctioned in 1982, the successful buyer was the young D. Brent Pogue in the early stages of building what would become the most valuable numismatic collection in history, according to Stack’s Bowers Galleries. Pogue’s collection would eventually fetch more than $140 million in a series of sales by Stack’s Bowers Galleries from 2015 through 2021. The newest owner of the 1822 Half Eagle has chosen to remain anonymous. While the 1822 Half Eagle earned the distinction of being the most expensive GOLD coin ever minted by the U.S, two other coins have sold for more. The 1794 Flowing Hair Silver Dollar — the first dollar coin issued by the United States federal government — realized more than $10 million at an auction at Stack’s Bowers Galleries in January 2013. The 1787 Brasher Doubloon — a gold coin minted privately by goldsmith and silversmith Ephraim Brasher — earned $9.36 million at Heritage Auctions this past January. Interestingly, barrons.com reader Stephen Donnelly did the math to determine the compound return for a $5 coin that would eventually sell for $8.4 million. He concluded that the $5 coin returned 7.5% annually over 199 years.

Scarce metals have become the new gold. Investors are now investing as a geopolitical battle for such metals is emerging and prices are rising. The price of rhodium, a raw material used to make automotive catalytic converters, has risen by 75% this year alone and by 200% since the start of the corona crisis. The number of police reports of catalytic converters cut off by criminals under cars is increasing. Thanks to a record price, thieves are diving everywhere on the metal that is offered to recyclers. Prices of raw materials such as lithium, cobalt, nickel and graphite are also on the rise, these metals are the hard core of batteries for electric cars and jet engines. There is stock worldwide, but new mines take years to be able to extract them.

Buying lists The demand for the metals for battery cars will only grow for the time being, according to ING Research. The environmental measures tightened up in the Paris climate agreement mean that polluting production with iron ore, steel and coal will be phased out. Investors walk through the purchase lists of rare metals that are becoming increasingly popular. They are also already looking at gallium, indium and platinum varieties. Also on the lists of "critical" metals is the dark gray beryllium, which is sought after in aerospace for its strength and limited weight. For example for the next generations of communication satellites. Tantalum is extremely resistant to metal corrosion and is therefore used in liquid metal containers, enamelled drums and jet engines. Fluorspar is also in demand, it is found in cement, glass and iron and lithium makes batteries more energy efficient. Rhodium is becoming scarcer: in combination with platinum and other metals, it can significantly reduce car emissions. Not well known, but electric toothbrushes can only make tens of thousands of rotational movements thanks to small magnets that work with scarce metals such as dysprosium, boron and neodymnium. Everyone runs to the same mines for such metals. Copper Revolution President Biden last week announced a US infrastructure investment plan that spans $ 2,250 billion. The entire road network is being overhauled, thousands of windmills and charging pole systems for battery cars are being built. Also for the fleet of the White House. Prices of tarmacadam for roads, kobolt and lithium are rising due to the expected demand from suppliers. Less scarce, but very popular for battery cars and the cabling of thousands of wind turbines is copper, which is widely used in construction works. Europe is emerging from the corona crisis after the United States and will also start purchasing more of the copper and rare materials for its industry and battery cars. Both regions notice that China, which has come out of the corona lockdowns earlier, has been buying up since April last year. Stocks are being hijacked, scarce metals are the subject of political power struggles. According to professor Rob de Wijk in his study The New World Order, China has the best strategic priority in this regard. For a decade, China has been restricting its own exports of rare metals, which are needed for lightweight metals for aircraft and windmill wings. China itself is not the largest battery metals miner, but 80% is processed there in its enormous industry, according to researcher Benchmark Mineral Intelligence. The power game According to market analysts, the Chinese Bureau of State Reserves recently bought up considerably more than the average in recent years at the very low corona crisis prices. Even a third more to the buyer. Copper prices have doubled since March last year to above $ 9,000 per ton. Trading house Trafigura, a large copper merchant, foresees a rise in the copper price to $ 15,000. His economist Graeme Train attributes this to a historically unprecedented increase in demand. PwC, consultant for companies, has been warning corporate executives in the automotive, defense and chemical industries for the "ticking time bomb." With a growing population claiming the same prosperity, the demand for rare metals is outstripping supply.

In the days before the pandemic, 20 or 30 people would squeeze together around the long table and, over coffee and Danishes, listen to recordings of the Bible, according to people who were there. First might come the Old Testament, perhaps Isaiah or Lamentations. Then came the New, the Gospels, which called out to the listeners drawn from a path known more for its earthly greed than its godly faith: Wall Street. Hitting the play button and then receding into the background was the host, Bill Hwang, the mysterious billionaire trader now at the center of one of the biggest Wall Street fiascos of all time. The story thus far -- of a mind-boggling fortune made in stealth and then wiped out very publicly in a blink -- has sent shock waves through some of the world's mightiest banks. Estimates of the potential size of his position before it imploded have spiraled toward $100 billion. The Securities and Exchange Commission is looking into the disaster, which has set teeth on edge in trading rooms across the globe. But those accounts tell only part of the story. Interviews with people from inside Hwang's circle, Wall Street players close to him and documents associated with his multimillion-dollar charitable foundation fill in missing puzzle pieces -- ones that haven't been reported previously. The picture that emerges is unlike anything Wall Street might suspect. There are, in a sense, not one but two Bill Hwangs.

Christian Capitalist One of them walks for hours through New York's Central Park listening to recordings of the Bible and embraces a new, 21st-century vision of an age-old ideal: that of a modern Christian capitalist, a financial speculator for Christ, who seeks to make money in God's name and then use it to further the faith. A generous benefactor to a range of unglamorous, mostly conservative Christian causes, this Hwang eschews the trappings of extravagant wealth, rides the bus, flies commercial and lives in what is, by billionaire standards, humble surroundings in suburban New Jersey. Then there's the other Bill Hwang: a former acolyte of hedge fund legend Julian Robertson with a thirst for risk and a stomach for volatile markets -- a daring trader who once lost a fortune betting against German automaker Volkswagen AG while running a hedge fund that was supposedly focused on Asian stocks. This is also the Bill Hwang who then went on to quietly become one of the most successful alumni of Robertson's vaunted Tiger Management. This one masks his dangerous leveraged bets from public view via financial derivatives, was once accused of insider trading and pleaded guilty in 2012 to wire fraud on behalf of his hedge fund, Tiger Asia Management. That same Bill Hwang, it turns out, is also a backer of one of Wall Street's hottest hands of late, Cathie Wood of Ark Investments. Like Hwang, Wood is known to hold Bible study meetings and figures into what some refer to as the "faith in finance" movement. And here, at last, is where the Bill Hwangs collide. The fortune he amassed under the noses of major banks and financial regulators was far bigger and riskier than almost anyone might have thought possible -- and these riches were pulled together with head-snapping speed. In fact, it was perhaps one of the greatest accumulations of private wealth in the history of modern finance. And Hwang lost it all even faster. Archegos -- a Greek word often translated as "author" or "captain," and often considered a reference to Jesus -- was believed by many traders doing business with the firm to be sitting atop $10 billion of assets. That figure, representing Hwang's personal fortune, was actually closer to $20 billion, according to people who did business with Archegos. To put that figure in context: Bill Hwang, a name few even on Wall Street had heard until now, was worth more than well-known industry figures like Ray Dalio, Steve Cohen and David Tepper. Even more remarkable is the breakneck speed at which Hwang's fortune grew. Archegos started out in 2013 with an estimated $200 million. That's a sizable fortune but nowhere near big money in the hedge fund game. Yet within a decade, Hwang's fortune swelled 100 times over, traders and bankers now estimate. Much of those riches accrued in the past 12 to 24 months alone, as Hwang began to employ more and more leverage to goose his returns, and as banks, eager for his lucrative trading business, eagerly obliged by extending him credit. Hwang's success enabled him to endow his own charity, the Grace & Mercy Foundation, which had almost $500 million of assets as of 2018, according to its most recent tax filing. One institution close to Hwang, and a beneficiary of his foundation, is The King's College, a small Christian school in the heart of New York's Financial District. In a statement to Bloomberg, the college said it was grateful for his generosity and that "our prayers are with Mr. Hwang and his staff." McDonald's Job The story of both Bill Hwangs begins in South Korea, where he was born Sung Kook Hwang in 1964. The tale he has told friends and associates is a familiar one of immigrant striving -- followed by financial success that few even on Wall Street can fathom. Hwang grew up in a religious household (like roughly a third of Koreans, his parents were Christian). When he was a teenager, the family moved to Las Vegas, where his father got a job as a pastor at a local church. Hwang has told friends that he arrived in the U.S. unable to speak or write in English and only picked up the language while working nights at McDonald's. Soon after, his father died and his mother moved the family to Los Angeles. Hwang went on to study economics at the University of California, Los Angeles, and then picked up an MBA at Carnegie Mellon University in Pittsburgh. Finance beckoned -- and Hwang, it turned out, was very good at it. While a lowly salesman at Hyundai Securities, part of the sprawling Korean chaebol the Hyundai Group, he caught Julian Robertson's eye. Hwang, not yet 33, was then handed a golden ticket to Wall Street: an offer to join Robertson's Tiger Management, then at the top of its game. Hwang quickly distinguished himself by introducing Robertson to the Korean markets -- at the time headed into the teeth of the Asian financial crisis -- and masterminding what turned into a lucrative stake in SK Telecom Co. Hamptons Lunch Tiger colleagues say Hwang was one of Robertson's most successful proteges -- a quiet, methodical analyst with intense focus. Even today, he keeps his desk free of all clutter, the better to focus his mind. Robertson, these people recall, dubbed him "the Michael Jordan of Asian investing." Robertson, now 88, still considers Hwang a friend, and the two lunched together in the Hamptons a few months ago. "He's not one to be tiny, that's one thing for sure," Robertson told Bloomberg after news of the Archegos losses broke. Hwang would eventually strike out on his own as a so-called Tiger cub. Initially, Hwang shot the lights out, returning an annualized 40% through 2007, when he managed $8 billion. The hot streak didn't last. In late 2008, his Tiger Asia incurred stinging losses on a big bet against Volkswagen. Many other hedge funds were shorting the German automaker, too, and when Porsche Automobil Holding SE abruptly announced that it would raise its stake, all hell broke loose. VW soared 348% within 48 hours, crushing shorts like Hwang. Tiger Asia ended the year down 23%. Many investors pulled their money, angry that a hedge fund that was supposed to be focusing on Asia somehow got caught up in the massive squeeze. GameStop Frenzy It was a painful and instructive lesson for Hwang, people who know him say. In the future, he'd hunt out stocks that many traders were shorting and go long instead. Millions of amateur investors took up that approach this year during the social media-fueled frenzy over GameStop and other stocks. But before the next success, Tiger Asia ran into more trouble -- this time, trouble big enough to bring Hwang's days as a hedge fund manager to an end. When Tiger Asia pleaded guilty to wire fraud in 2012, the SEC said the firm used inside information to trade in shares of two Chinese banks. Hwang and his firm ended up paying $60 million to settle the criminal and civil charges. The SEC banned him from managing outside money and Hong Kong authorities prohibited him from trading there for four years (the ban ended in 2018). Shut out of hedge funds, Hwang opened Archegos, a family office. The firm, which recently employed some 50 people, initially occupied space in the Renzo Piano-designed headquarters of the New York Times. Today it's based further uptown, by Columbus Circle, sharing its address with the Grace & Mercy Foundation. "My journey really began when I was having a lot of problems in our business about five or six years ago," Hwang said in a 2017 video. "And I knew one thing, that this was a situation where money and connections couldn't really help. But somehow I was reminded I had to go to the words of the God." That belief helped Hwang rebuild his financial empire at dizzying speed as banks loaned him billions of dollars to ratchet up his bets that unraveled spectacularly as the financial firms panicked. What ensued was one of the greatest margin calls of all time, pushing his giant portfolio into liquidation. Some of the banks may end up with combined losses of as much as $10 billion, according to analysts at JPMorgan Chase & Co. As a bruised Wall Street points its collective finger at Hwang, his Christian associates have rallied around him. Doug Birdsall, honorary co-chairman of the Lausanne Movement, a global group that seeks to mobilize evangelical leaders, said Hwang always likes to think big. When he met with him to discuss a new 30-story building in New York for the American Bible Society, Hwang said, "Why build 30 stories? Build it 66 stories high. There are 66 books in the bible." Before so much went so wrong so fast, Archegos appeared to be ramping up. A year ago, Hwang petitioned the SEC to let him work or run a broker-dealer; the SEC agreed. It's impossible to say where Bill Hwang, the hard-charging financial speculator, ends, and Bill Hwang, the Christian evangelist and philanthropist, begins. People who know him say the one is inseparable from the other. Despite brushes with regulators, staggering trading losses and the question swirling around his market dealings, they say Hwang often speaks of bridging God and mammon, of bringing Christian teaching to the money-centric world of Wall Street. |

Thank you for choosing to make a difference through your donation. We appreciate your support.

Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed