The European Union has put together a preliminary agreement that includes a €10,000 cap on cash payments to address the challenges posed by money laundering and the financing of terrorism.

The accord, reached through negotiations among member states and the European Parliament this week, seeks to protect citizens and the EU financial system from illicit financial activities. However, the proposed legislation raises privacy concerns and fears of state surveillance and government control over how people spend their money, as well as potential abuse of the new powers. The newly established regulations will impose the cash payment limit on entities engaged in financial services, banking, real estate agencies, asset management firms, casinos, and merchants. Moreover, these entities will be obligated to verify the identity of individuals making cash payments within the range of €3,000 to €10,000. While member countries have the flexibility to set lower limits for cash payments, the interim agreement introduces a heightened focus on monitoring high-net-worth individuals, a provision advocated for by Members of the European Parliament (MEPs). In an expansion of the scope of oversight, the interim agreement now encompasses a significant segment of the cryptocurrency sector. Crypto service providers will be required to authenticate customer identities for transactions equal to or exceeding €1,000. Beginning in 2029, the regulatory framework will be extended to include professional football clubs and agents, which will be categorized as obligated entities. This classification mandates these entities authenticate customer identities, monitor transactions, and promptly report any suspicious money transfers to the financial intelligence services of their respective countries. The agreement empowers member countries to exclude football clubs and agents from their national lists if they are determined not to pose a risk. National financial intelligence services and other competent authorities will gain access to information on ownership, bank accounts, and land and property registries. These authorities will also supervise the transfer of ownership for specific luxury goods, setting thresholds at €250,000 for cars and €7.5 million for yachts and aircraft. The impending implementation of the new legislation has ignited a robust public debate, exposing a diverse range of viewpoints. Heightened apprehensions surrounding potential totalitarian surveillance, especially with exemptions for high-profile individuals, evoke disquieting parallels to Orwell’s ‘1984’ and intensify fears of a dystopian reality. Skepticism has been cast on the effectiveness of these regulations, prompting queries about their ability to genuinely combat money laundering and fostering calls for a more inclusive strategy that addresses the burgeoning cryptocurrency sector. Conversely, some interpret the EU’s cash payment cap as a positive stride toward meeting the needs of the contemporary economy. They acknowledge the evolving financial landscapes and the digitization of cash flows, including the growing influence of central bank digital currencies. However, there are those who condemn these measures as excessive state control. The ongoing discourse reflects a polarized perspective on the EU’s actions, encapsulating concerns about potential abuses of power and the necessity of adapting payment methods to contemporary needs. This debate underscores the intricate dynamics between financial regulations, surveillance, and individual freedoms in the digital age.

0 Comments

The euro inched higher on Tuesday, reversing earlier falls that had taken it to the brink of parity with the dollar, but it stayed under heavy pressure from a potential energy supply crunch and uncertainty over the ECB's rate rise campaign. The euro fell as low as $1.00005, before edging off that level . By 1315 GMT it was up 0.15%, at $1.00540.

Neil Jones, head of currency sales at Mizuho, said markets had been 'short' the euro in anticipation of a break below parity, but "we didn't get it and now these shorts are buying back into the early New York market". One-month implied euro-dollar volatility, a gauge of expected swings, around 12.5% , the highest since March 2020. The biggest pipeline carrying Russian gas to Germany, the Nord Stream 1, began annual maintenance on Monday, with flows expected to stop for 10 days. But governments and markets are worried Russia might extend the shutdown, exacerbating the euro bloc's energy crunch and tipping its economy into recession. A dire reading from the ZEW economic research institute, reinforced the economic gloom, showing German investor sentiment nosedived in July to -53.8 points from -28.0 in June. "The market is playing cat and mouse with euro parity at the moment in the absence of any major macro drivers," said Simon Harvey, head of FX at Monex Europe, adding that Wednesday's U.S. inflation data -- expected at 8.8% for June -- could prove the catalyst. "We may have to wait for U.S. CPI...or a clearer picture for European energy markets once planned maintenance in Nord Stream comes close to finalising for euro-dollar to break the threshold," Harvey added. Euro weakness was most pronounced against the dollar. The dollar index , which tracks the unit against a basket of six counterparts with the euro most heavily weighted, earlier climbed to 108.56, its highest since October 2002, but then eased to $108.10. Analysts also cited growing uncertainty over the European Central Bank's plans to raise interest rates, initially by 25 basis points in July, then by 50 bps in September. Fed funds futures, meanwhile, price U.S. rates reaching 3.50% by March, rising from 1.58% currently. "The expectation is for the (U.S. Federal Reserve) to do 75 bps this month and its aim seems to be to get to neutral (rates) as soon as possible, while with ECB, it's more of a mixed message given the backdrop over gas," said Sarah Hewin, senior economist at Standard Chartered. Euro weakness has been a big part of the dollar index's push higher, but the greenback has been also supported by worries about growth elsewhere, with China in particular implementing strict zero-COVID policies to contain fresh outbreaks. The offshore-traded yuan approached one-month lowsat 6.753 . The dollar slipped however to 136.72 yen , down 0.5%, following Monday's jump to new 24-year highs at 137.75. The stuttering global economyis undermining commodity-focused currencies. Canada is expected to raise interest rates by 75 bps respectively on Wednesday but the Canadian dollar eased 0.2% versus U.S. dollar.  The White House will unveil a comprehensive set of regulations targeting cryptocurrency on Wednesday, President Joe Biden has revealed. The president called it “the first ever whole-of-government approach to addressing the risks and harnessing the potential benefits of digital assets and their underlying technology.” Among other measures, the order includes a 180-day deadline for several reports on “the future of money” – presumably referring to digital currencies like the one his administration has asked the Fed to step up its research and development of. For now, around 100 other countries are also working on so-called central bank digital currencies (CBDCs).

There is “significant momentum” behind the idea of a CBDC, which is essentially a cryptocurrency without the privacy implied by the term “crypto,” controlled by (and accessible by) the Fed, according to a source who spoke to Reuters about the matter earlier this week before the White House’s statement was made public. The language used in the announcement – which carefully avoids discussing ‘cryptocurrencies’ as such, preferring the vaguer blanket term “digital assets” – is unlikely to have any immediate effect on how crypto is regulated in the US, the administration claims. Instead, the order directs agencies like the Treasury Department and the Securities and Exchange Commission to “assess risks and opportunities involved in cryptocurrency use” and issue regulations from there. The administration hopes to have all government agencies on the same page regarding how they handle crypto and other digital assets both legal and otherwise. The aim of the new policy, Biden’s office said, is to keep the US in the centre of both technology and the global financial system. The US’ dollar hegemony has wobbled in recent years as the national debt and inflation skyrocket and other countries worry about being tied to an ever-shrinking ‘reserve currency’ whose orbit they can’t leave. As the price of gas soars due to sanctions on Russian energy imports, the petrodollar alliance that has held since the US left the gold standard in the 1970s appears more fragile than ever.  The Bank of Russia proposed slapping a ban on mining, issuing, circulating, and exchanging cryptocurrencies, including bitcoin, by any Russian players, crypto exchanges, crypto exchanges, and P2P platforms in Russia. The regulator agrees only to allow citizens to own cryptocurrency, but not to buy it from any Russian infrastructure. Experts told Vedomosti that a complete ban on operations with cryptocurrencies is not the best option to deal with any possible problems. The Bank of Russia wants to ban all financial institutions, banks or, for example, brokers from being intermediaries and providing their infrastructure for carrying out any operations with cryptocurrency. Financial institutions will not be able to invest in cryptocurrencies. The regulator believes that not only does direct ownership of cryptocurrencies but also investing in its derivative financial instruments hold risks. Tight regulation will only apply to cryptocurrencies, but not assets such as NFTs. The regulator proposed introducing fines for all these violations. So far, there are no specifics in the report of the Bank of Russia for public consultations.

The ban on cryptocurrencies in Russia means lost profits for the country's budget, CEO of ANO Digital Platforms Arseniy Shcheltsin told the newspaper. In addition, it would limit the development of Russian projects in this area and provide a signal to developers and professional users not to conduct business related to cryptocurrencies in Russia. The prohibition would not be appropriate either for investors or for the state, attorney at Criminal Defense Firm Daniil Gorky says. Imposing bans can lead to investors losing their crypto-currency assets, while Russia already today ranks third in the world in terms of cryptocurrency mining. KPMG Law Partner Olga Yasko believes that the risks named by the Bank of Russia are real, but it would be more effective to manage them through control mechanisms. The annual volume of operations involving cryptocurrency among Russians, according to the Central Bank, reaches around $5 bln, thereby demonstrating that Russians are one of the most active players on this market.  China's central bank on Friday announced a ban on all cryptocurrency payments and services, escalating its ongoing clampdown on bitcoin and other digital coins as it moves to roll out its own virtual currency.

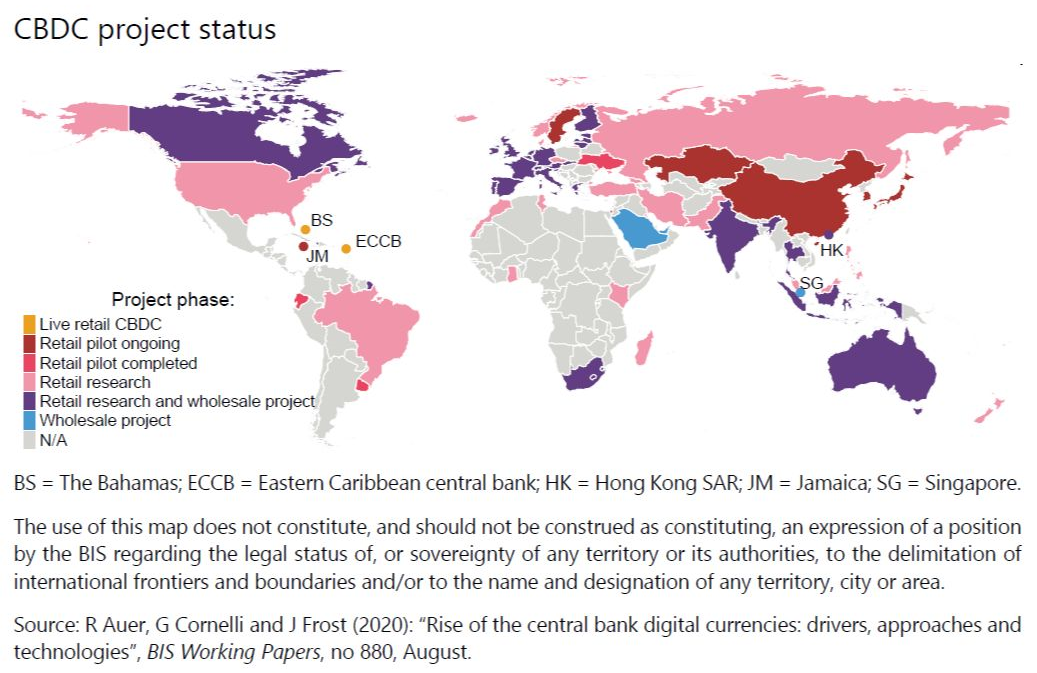

Chinese regulators' latest action "strictly prohibits" exchanging cryptocurrency for legal tender, providing information or pricing services, and trading in cryptocurrency derivatives. The measure also applies to overseas exchanges that provide services online within the country's borders. Violators will face criminal penalties. This marks Beijing's latest ratcheting up of restrictions on what it sees as a vehicle for capital flight and competition for its digital yuan, now set to roll out as early as 2022. The price of bitcoin, the world's leading virtual currency, fell by as much as 9% after the announcement to below $41,000 before paring its losses. The statement, signed by multiple authorities including the People's Bank of China, the Cyberspace Administration of China and the Supreme People's Court said virtual currencies had "disrupted the economic and financial order" and bred money laundering, illegal fundraising and fraud. Virtual currencies do not have the same legal status as legal tender, and may not be circulated in markets as currency, the document stated, naming specific examples including bitcoin and Ethereum. Takahide Kiuchi, executive economist at Nomura Research Institute and a former Bank of Japan policy board member, called the latest move an "extension" of measures to "ban all virtual currencies except central bank digital currency." China in June ordered five state-run banks including Industrial and Commercial Bank of China, Agricultural Bank of China, as well as mobile payments giant Alipay, to cut off cryptocurrency transactions. It also imposed a broad ban on virtual-currency mining that month, driving many miners overseas and slashing the country's share of digital coin creation, once above 80%. Also on Friday, the authorities announced even tougher mining restrictions, barring new operations and accelerating exits from existing projects. Supplying electricity to miners is prohibited, and such projects cannot receive financial, fiscal or tax support. The PBOC plans an official launch of the digital yuan as soon as 2022, following testing at the Winter Olympics. China plans to revise its laws to add it as legal tender and ban private-sector issuance of digital currencies, whose proliferation poses an oversight challenge for regulators. Capital flight is another factor. Cryptocurrencies have been used to circumvent Beijing's capital controls since before the coronavirus pandemic, and regulators have sought to close this loophole. The direct impact of the ban will be limited, as China's influence on virtual currency markets has diminished. But as the U.S. hammers out new regulations and other countries work toward their own digital currencies, market watchers are keeping an eye out for similar moves elsewhere. One of the most potentially far-reaching trends in the financial landscape right now is the imminent roll-out of Central Bank Digital Currencies (CBDCs), and the parallel attacks which central bankers are waging on private digital currencies and tokens as they tee up the launch of their CBDCs. First some clarifications. While the majority of central bank issued currencies (fiat currencies) in existence around the world are already in digital form, a fiat currency held in digital form is not the same as a Central Bank Digital Currency (CBDC).  What is a CBDC? A CBDC generally refers to electronic or virtual central bank (fiat) money that is created in the form of digital tokens or account balances which are digital claims on the central bank. CBDCs will be issued by central banks and will be legal tender. Many CBDCs that are being researched and developed employ Distributed Ledger Technology (DLT), with the recording of transactions on a blockchain. However unlike private cryptocurrencies which use a permissionless and open design, CBDCs that use DLT will use permissioned variants (deciding who has access to the network and who can view and update records in the ledger). Critically, as the name suggests, CBDCs will be centralized and governed by the issuing authority (i.e. a central bank). So, in their design and structure, CBDCs can be viewed as the very antithesis to decentralized private cryptocurrencies and tokens. Central banks have already working on two types of CBDCs, ‘wholesale’ digital tokens that would have access restricted to banks and financial entities to be used for activities like interbank payments and wholesale market transactions, and ‘general purpose’ (retail) CBDC for the general public to be used in retail transactions. It is this ‘general purpose’ CBDC which most people are referring to when they discuss central bank digital currencies, and it is these ‘general purpose’ CBDCs that will be most important to watch when central banks and governments begin to attempt their roll-outs to distribute CBDCs to billions of people across the world either through account-based CBDCs or ‘digital cash’ tokens. As you can guess, account-based CBDCs will be tied to user identities and Digital IDs, and straight off the bat they allow for total surveillance by the State and torpedo any chance of anonymity. For this reason, they are already a favourite among central banks. Given that CBDCs will be centralized ledgers and can be programmable, the ‘digital cash’ token option is not much better in terms of privacy and freedom. Many central banks will probably opt for a hybrid model of both account-based and token based digital cash. As an example, Canada, the one time liberal democracy, perhaps illustrates the account-based vs token based choices best, where Canada’s central bank, the Bank of Canada, in it’s design documentation for CBDCs shows that at the end of the day, it’s about surveillance and control, saying that : “anonymous token-based options would be allowable for smaller payments, while account-based access would be required for larger purchases.” Accelerating rollout CBDCs are not just a buzzword or a hazy innovation that may appear sometime in the distant future. They are actively being developed now, and in widespread fashion. In January 2020, the Bank for International Settlements (BIS) issued the result of a survey on CBDC's that it had conducted in the second half of 2019, and to which 66 central banks had responded. Strikingly, 10% of central bank respondents (which represented a fifth of the world’s population) said that they were likely to issue a ‘general purpose’ CBDC (for the general public) in the near future (within the next 3 years). Another 20% of central bank respondents said they would likely issue a ‘general purpose’ CBDC in the medium term (within 6 years). In August 2020, the BIS published a comprehensive working paper on CBDCs titled “Rise the central bank digital currencies drivers, approaches and technologies" one part of which analysed the BIS database of central banker speeches and found that between December 2013 and May 2020, there had been 138 central banker speeches mentioning CBDCs, with a dramatic increase in CBDC related speeches since 2016, a timeframe which coincided with central banks launching research projects on CBDCs. The same BIS report also highlighted that, (totally coincidentally) the Covid-19 ‘pandemic’ “accelerated work on CBDCs in some jurisdictions."   The central banks of Australia, Singapore, Malaysia and South Africa have announced a joint initiative to trial international settlements using central bank digital currencies (CBDC). The initiative, dubbed Project Dunbar, will prototype shared platforms enabling direct transfers between institutions using digital currencies issued by multiple central banks. The pilot’s findings will be used to inform the “development of global and regional platforms” in addition to supporting the G20’s roadmap for improving cross-border payments. Project Dunbar will be carried out in partnership with the Bank for International Settlements (BIS) Innovation Hub from its Singapore Center. The project will engage multiple partners to develop different distributed ledger technology (DLT) platforms and explore different designs that would enable central banks to share CBDC infrastructure. A joint announcement emphasizes the efficiency savings associated with DLT-based payments, stating: “These multi-CBDC platforms will allow financial institutions to transact directly with each other in the digital currencies issued by participating central banks, eliminating the need for intermediaries and cutting the time and cost of transactions.” Michele Bullock, assistant governor of the Reserve Bank of Australia (RBA), highlighted that “enhancing cross-border payments has become a priority for the international regulatory community,” adding that the RBA is “very focused” on the matter in its domestic policy work. “Project Dunbar brings together central banks with years of experience and unique perspectives in CBDC projects and ecosystem partners at advanced stages of technical development on digital currencies,” said Andre McCormack, head of the BIS Innovation Hub Singapore Centre. He added: “With this group of capable and passionate partners, we are confident that our work on multi-CBDCs for international settlements will break new ground in this next stage of CBDC experimentation and lay the foundation for global payments connectivity.” The RBA has consistently downplayed the need for a domestic CBDC, however, citing the success of the New Payments Platform, which allows instant digital transfers 24-hours a day.

The European Commission is considering a new registry to register all citizens' possessions. This should not only include properties in the form of real estate, land and shares, but also assets such as precious metals, cryptocurrencies, jewelry, works of art, cars and boats. This is evident from a new document entitled 'Feasibility Study for a European asset registry'. According to the European Commission, such a register is necessary to prevent tax evasion and money laundering. It provides the authorities with more information to map out money flows. From the text of the proposal: "Data collection and interconnection of registers is an important tool under EU law to speed up competent authorities' access to financial information and facilitate cross-border cooperation. Several possibilities researched to collect information with a view to establishing an asset register that can then be used for a future policy initiative. It will examine how to analyze information from different sources on asset ownership (e.g. land registers, company registers, trust and foundation registers, central securities depositories, etc.) and how the design, scope and challenges of such an asset register of the Union can look like. It will also be examined whether data on the ownership of other assets, such as cryptocurrencies, works of art, real estate and gold, can be included in the register." Financial repression Although this is only a proposal, this is a very worrying development. It gives governments even more insight into the wealth of citizens, on top of the information they already collect. It is striking that the proposal only focuses on the interests of governments, supervisors, banks and NGOs and does not take into account the interests of European citizens. The proposal also does not clarify why a more detailed registration of assets is necessary. Under the guise of money laundering and terrorism, such a register further affects the freedom and privacy of citizens. Governments use it as an excuse to exercise more control over their own population. The proposal is therefore strongly criticized from various quarters. According to the German politician Markus Ferber, the European Commission is passing its book. "These plans are completely disproportionate. The relationship between the citizen and the state reminds me of China, not EU member states, when these kinds of plans are made." Control State The German newspaper Die Welt concludes that with this register all assets of gold and bitcoins become traceable, while the Austrian newspaper Die Presse reminds of a chapter from Orwell 1984. According to the Austrian Kroner Zeitung, such a registration of assets is impracticable in practice. and also very expensive. According to the German magazine Focus, the EU wants to map the wealth of all people down to the last cent: "If this register were established, the consequences are obvious. For example, for politically unwelcome citizens - and not only criminals - it will be much more difficult in the future to continue their activities. investigative journalists or whistleblowers, who are threatened with more targeted reprisals. Controlling money flows, investments and assets is contrary to human dignity. Under the guise of preventing money laundering, we are all being vetted. Now is the time for civil disobedience. People have to take to the streets, like the yellow vests in France." Capability mapping is the next step in tightening control over citizens. Earlier, the European Commission advocated stricter supervision of cryptocurrencies. She wants to register all crypto addresses, so that anonymous transactions come to an end. The European Commission also issued a directive this summer to ban transactions over €10,000 in cash across the European Union. A worrying development, even for savers who have nothing to hide.

|

Thank you for choosing to make a difference through your donation. We appreciate your support.

Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed