|

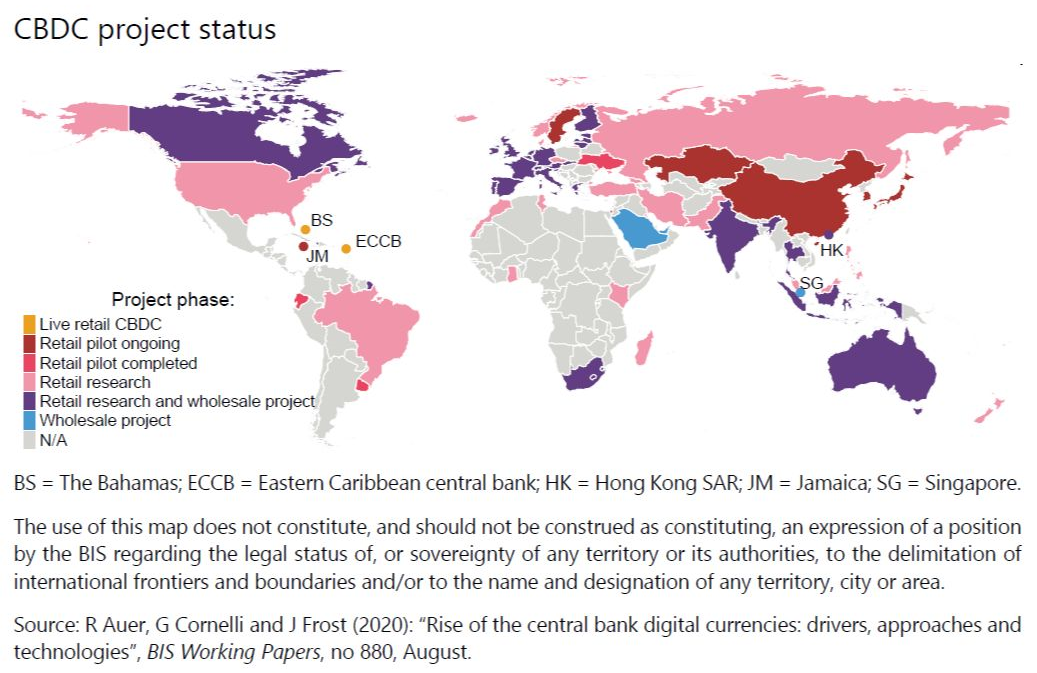

One of the most potentially far-reaching trends in the financial landscape right now is the imminent roll-out of Central Bank Digital Currencies (CBDCs), and the parallel attacks which central bankers are waging on private digital currencies and tokens as they tee up the launch of their CBDCs. First some clarifications. While the majority of central bank issued currencies (fiat currencies) in existence around the world are already in digital form, a fiat currency held in digital form is not the same as a Central Bank Digital Currency (CBDC).  What is a CBDC? A CBDC generally refers to electronic or virtual central bank (fiat) money that is created in the form of digital tokens or account balances which are digital claims on the central bank. CBDCs will be issued by central banks and will be legal tender. Many CBDCs that are being researched and developed employ Distributed Ledger Technology (DLT), with the recording of transactions on a blockchain. However unlike private cryptocurrencies which use a permissionless and open design, CBDCs that use DLT will use permissioned variants (deciding who has access to the network and who can view and update records in the ledger). Critically, as the name suggests, CBDCs will be centralized and governed by the issuing authority (i.e. a central bank). So, in their design and structure, CBDCs can be viewed as the very antithesis to decentralized private cryptocurrencies and tokens. Central banks have already working on two types of CBDCs, ‘wholesale’ digital tokens that would have access restricted to banks and financial entities to be used for activities like interbank payments and wholesale market transactions, and ‘general purpose’ (retail) CBDC for the general public to be used in retail transactions. It is this ‘general purpose’ CBDC which most people are referring to when they discuss central bank digital currencies, and it is these ‘general purpose’ CBDCs that will be most important to watch when central banks and governments begin to attempt their roll-outs to distribute CBDCs to billions of people across the world either through account-based CBDCs or ‘digital cash’ tokens. As you can guess, account-based CBDCs will be tied to user identities and Digital IDs, and straight off the bat they allow for total surveillance by the State and torpedo any chance of anonymity. For this reason, they are already a favourite among central banks. Given that CBDCs will be centralized ledgers and can be programmable, the ‘digital cash’ token option is not much better in terms of privacy and freedom. Many central banks will probably opt for a hybrid model of both account-based and token based digital cash. As an example, Canada, the one time liberal democracy, perhaps illustrates the account-based vs token based choices best, where Canada’s central bank, the Bank of Canada, in it’s design documentation for CBDCs shows that at the end of the day, it’s about surveillance and control, saying that : “anonymous token-based options would be allowable for smaller payments, while account-based access would be required for larger purchases.” Accelerating rollout CBDCs are not just a buzzword or a hazy innovation that may appear sometime in the distant future. They are actively being developed now, and in widespread fashion. In January 2020, the Bank for International Settlements (BIS) issued the result of a survey on CBDC's that it had conducted in the second half of 2019, and to which 66 central banks had responded. Strikingly, 10% of central bank respondents (which represented a fifth of the world’s population) said that they were likely to issue a ‘general purpose’ CBDC (for the general public) in the near future (within the next 3 years). Another 20% of central bank respondents said they would likely issue a ‘general purpose’ CBDC in the medium term (within 6 years). In August 2020, the BIS published a comprehensive working paper on CBDCs titled “Rise the central bank digital currencies drivers, approaches and technologies" one part of which analysed the BIS database of central banker speeches and found that between December 2013 and May 2020, there had been 138 central banker speeches mentioning CBDCs, with a dramatic increase in CBDC related speeches since 2016, a timeframe which coincided with central banks launching research projects on CBDCs. The same BIS report also highlighted that, (totally coincidentally) the Covid-19 ‘pandemic’ “accelerated work on CBDCs in some jurisdictions."

0 Comments

Leave a Reply. |

Thank you for choosing to make a difference through your donation. We appreciate your support.

Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed