Recently, the Netherlands Authority for the Financial Markets (AFM) warned investors against making decisions based on tips from financial influencers. Those influencers have become very popular, and they not only share knowledge about investing, but also about pensions, student loans and mortgages, for example. What does this advance mean for our financial well-being?

Trend watcher Farid Tabarki distinguishes two trends among financial influencers. "There is a large group that is involved in learning how to handle money properly. That makes me very enthusiastic." That is absolutely necessary, he says. For example, research by Nibud shows that 32 percent of Dutch households are dealing with payment arrears. "People who train each other financially seems to me to be a very positive development." On the other hand, there is a group of financial influencers who focus on making money, the trendwatcher explains. "Investment tips, cryptocurrency… That can be useful, but you never know for sure what someone's motives are for giving those tips. There may be revenue models behind it that are not in your favor." 'Too easy to call everything bad' Media scientist Roel Lutkenhaus can imagine that people are misled by financial influencers. "But I find it too easy to say: 'everything is bad'. There are also many people who give sincere tips. For example, I think the Young Investing podcast is very good. It falls into the category of someone who has stuck in the topic, and the podcast makes it to simply share his tactics and knowledge. I don't see any dark edges in that." But those dark edges are there. A good example of such an influencer is Madelon Vos, who, unhampered by experience and knowledge, provides her followers with one-sided information about Bitcoin in particular via her podcast every week. Week after week, her technical analyzes mislead her followers. Few can see through her chatter and seductive smile. Nor does she take any responsibility for her opinion. She never reflects on what she has said in previous episodes of her podcast. The most shocking part is that she discusses tweets from others and gives her one-sided opinion about them. Everyone wants to be successful, the behavioral scientist explains the popularity of financial influencers. "Making, getting rich, for example through crypto, is popular in youth cultures. People won't just take something from everyone, but certain financial influencers have built a strong relationship with their followers." Research by mobile broker BUX shows that one in five young people obtain investment knowledge from influencers. According to Lutkenhaus, the solution lies mainly in media literacy. "It's up to the government to make people resilient, so that they don't just fall prey to people who may not have the best intentions for their followers." Fishing out the bad apples isn't always easy. "I always tell myself: if it sounds too good to be true, it probably isn't. If people promise you golden mountains based on a few mouse clicks, it's not very credible. Don't take such influencers to seriously."

0 Comments

Thailand now in Pole Position for 2021

In fact, with China and Russia now ‘officially’ out of the market for buying gold since 2019 and early 2020, respectively, this Bank of Thailand gold buying is the largest short-term gold accumulation operation by any central bank sovereign since the Polish central bank bought 100 tonnes of gold in London during the first half of 2019 and promptlyto Warsaw. Thailand’s 90 tonnes addition in its gold reserves over April and May comprised a 43.5 tonnes increase in during April, and another 46.5 tonnes increase during May, taking its total gold reserves from 154 tonnes to 244 tonnes, a 58.4% increase. While the Polish and Hungarian gold purchases were announced in official press releases and attracted plenty of media attention, the same cannot be said of Thailand’s 90 tonnes purchase. In fact, apart from the publication of updates to its international reserve data position (both on its website and in an IMF database), there has been no comment from the Thai central bank that they have made this massive gold purchase. Media coverage of Thailand’s gold buying has also been thin on the ground, with only a few references to Thailand’s April gold buying, and as of yet, practically nothing about the Bank’s gold buying during May. The Data – Discreet Updates The first place where additions to Thailand’s gold reserve position are published is in the Bank of Thailand’s weekly ‘International Reserves’ report, which can be accessed here. Since this report only shows Thailand’s gold reserves reported in ‘millions of US dollars’, the number of fine ounces held has to be inferred. In early May, this report (based on LBMA afternoon gold prices on month end dates) showed that Thailand’s gold holdings had risen from 4,948,620 ozs on 26 March, to 6,351,976 ozs on 30 April, i.e. a 43.65 tonnes increase. In early June, this report showed that Thailand was reporting gold holdings of 7,862,528 ozs of gold, a 46.98 tonnes increase on the end of May, and a cumulative 90.6 tonnes increase on the end of March. When central banks publish reserve data updates, they sooner or later then report the same data to the International Monetary Fund (IMF), which in turn publishes these updates in its International Financial Statistics (IFS) database. As a verification source, you could argue that when central bank gold reserve holdings data appears in the IMF database, then you can assume its valid, since it is this IMF source which organisations such as the World Gold Council in turn use to produce their global central bank gold holdings rankings. Turning to the IMF IFS data tables, and running an extract for Official Reserve Assets of Thailand over March, April and May 2021 (which includes the variable Volume in Millions of Fine Troy Ounces), we find that the figures check out nearly exactly as per the Bank of Thailand website, with month-end reported gold holdings in the IFS table of 4.95 million ozs in March, 6.35 million ozs in April, and 7.85 million in May. This equates to a 1.4 million ozs gold purchase in April, and a 1.5 million oz gold purchase in May, for a total of 2.9 million ozs. Which is equivalent to additions of 43.54 tonnes in April and 46.65 tonnes in May (or 90.2 tonnes in total). So that’s incredibly close to the inferred figures from the Bank of Thailand weekly report.

This has not been a good week for cryptocurrency investors. They’ve seen about a quarter of the value of all crypto assets wiped out amid a crackdown on crypto mining and transactions in China. The price of bitcoin, the dominant crypto asset, plunged below $US30,000 on Tuesday before recovering to trade above $US33,000. Last Friday, it was still trading at $US40,000. Bitcoin’s market capitalisation has plunged from nearly $US1.2 trillion ($1.6 trillion) at its peak two months ago to about $US630 billion in an overall crypto market, whose value has shrunk from $US2.5 trillion earlier this year to $US1.35 trillion. "The implosion in crypto prices in response to China’s actions is the latest demonstration of what has been a permanent feature of crypto assets - their violent volatility." The latest implosion in the volatile bitcoin price – a year ago it was trading at only $US9300 – came after China followed up a crackdown on crypto mining last month by ordering its major banks and digital payments giant Alipay not to provide services related to cryptocurrency transactions. The anti-crypto push in China is unlikely to be unique as governments and central banks around the world have been increasingly concerned about the implications of the explosion in crypto assets and their value. While China’s actions have been the most dramatic, the US passed new anti-money laundering legislation earlier this year that will enable the US Treasury to regulate cryptocurrencies. The Biden administration has foreshadowed new regulations to prevent digital currencies from undermining its anti-money laundering laws. That’s consistent with views in Europe and other developed economies, concerned about tax evasion and the use of crypto assets in criminal activities.

There are also concerns about financial stability, given the vastly increased acceptance of crypto assets as an alternate investment category and the longer-term threat that they might pose to conventional central bank-issued money. China’s motivations for its assault on cryptocurrencies include concerns about money-laundering, which is a particular issue for a country that imposes stringent capital controls and exerts pervasive and intrusive scrutiny and control over the activities of its citizens. The authorities have also been clamping down on the dominant digital payments companies, concerned about their growing power within the economy and financial system, the anonymity of transactions and the implications for financial stability. They have sought access to the fintech’s customers’ data. China effectively pulled the rug from under what would have been the world’s largest initial public offering earlier this year, Ant Group’s $US300 billion-plus float, as part of a broader effort to more intensely regulate its previously lightly regulated or unregulated fintechs. The directives to its banks and Alipay fit within that larger push to tighten central control over all financial activity. The restrictions on bitcoin mining had different drivers. In May, the government imposed a severe crackdown on crypto mining which, given that an estimated 65 per cent to 70 per cent of all bitcoin mining capacity was based in China, represents a massive threat to the cryptocurrency.  The commodities boom has taken a knock this month, and while there are many reasons to still bet on a so-called supercyle, it’s unlikely to be plain sailing. Vast amounts of stimulus, economies reopening from the pandemic and strong Chinese demand have driven a surge in raw-material prices this year, some to record highs. Yet they’ve slumped in the past two weeks – with some wiping out gains for the year – on a more hawkish U.S. monetary policy tone, China’s bid to cool inflation pressures and better weather for crops.

While that’s blown away some of the speculative froth from the market, the big question is whether the latest commodities bull run has passed its peak or is just taking a breather. Either way, the direction may not be broad based, with each market having its own individual levers pushing and pulling. Copper traders need to balance a short-term cooling in China with long-term green-energy prospects. Oil’s dip could be limited by falling stockpiles and supply concerns, iron ore is being whipsawed by Chinese policies, while gold will largely be at the mercy of when Federal Reserve tapering starts. “I can still see a lot of inflationary pressures in the supply chain, and the reality is that it’s going up,” said Michael Widmer, head of metals research at Bank of America Merrill Lynch in London. “From a commodity-price perspective, I can see the structural argument still for prices to stay elevated or go higher going forward.” Copper The year-long rally to a record in May was sparked by surging Chinese demand, but there are signs orders from manufacturers are starting to wane. Bulls are confident that the rest of the world will pick up the slack as renewable energy and electric-vehicle investment creates a step-change in demand in Europe and North America. Still, it could be a while before that spending makes its way to factory order books, and softer demand in the meantime could embolden bears who say current high prices aren’t justified by fundamentals. Gold Bullion is more susceptible to Federal Reserve actions than perhaps any other commodity. It tumbled to the lowest since early May after the U.S. central bank signaled monetary policy tightening could start earlier than expected and the dollar jumped. Although the precious metal is often bought as a hedge against inflation, the Fed signaled this week that higher-than-expected inflation would not be allowed to persist, opening up the door for faster stimulus tapering. That weighs on the appeal of non-interest bearing gold. UBS Group AG forecasts prices at $1,600 an ounce by year-end, compared with about $1,780 now.

From 24 March 2023, cash will no longer be accepted as a means of payment in Sweden. Coins and banknotes will not disappear completely in the beginning. But no one will be able to use them and they will end up as collectibles in museum collections. Today, about 80% of Swedes use cards. 58% of payments are made by card and only 6% by cash, according to the Swedish Central Bank. Online payments have risen sharply with more restaurants and shops no longer accepting cash payments. Most Swedish banks have stopped allowing customers to make cash transactions at checkouts. Many bank branches across the country have closed. Cash management is extremely expensive due to the high security systems.

The entire population in Sweden has mobile coverage and in recent years, almost all purchases have been made electronically: via debit / credit card using chip and Pin, through contactless transaction technology, or via mobile such as the Swish app designed by its six largest banks country to facilitate their customers. The same trend is observed in other Nordic countries, such as Finland, Norway, Denmark and Iceland. Both the banks and the Swedish government are encouraging people to adopt a cashless economy. Today, Swish is used by more than 50% of the population, while less than 13% of the population trades in cash. Swedish banks issue debit cards to citizens aged seven and over (with parental leave), which translates to more than 97% of the population. In this way, young citizens become familiar with the idea of a cashless society that will be the future. Cash accounts for less than 1% of total transactions in Sweden. More than 99% of merchants accept debit cards and cash payments account for less than 20% of total transactions. Sweden has always been one of the first countries to adopt new technologies. In 1661, it was the first country in Europe to introduce banknotes, and in recent years the Nordic country has been at the forefront of banking innovation. The first automatic cash machine in the country was installed and ready for use in July 1967. Reducing bank robberies and drug and arms sales was also one of the reasons Sweden decided to abolish cash. Bank robberies have dropped significantly in recent years, as most banks in Sweden do not have cash, and branches continue to close one after another. Finally, the Central Bank of Sweden is testing its own digital currency, the e-Krona, which is expected to accelerate the country’s transition to a cashless society. The e-Krona pilot program started in 2019 and will be adopted throughout the country in 2021.

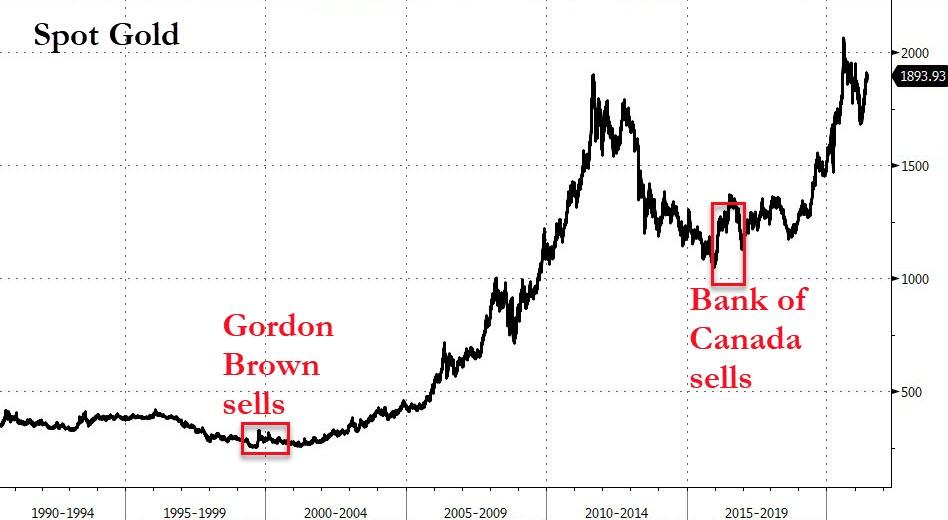

"The peculiarity of Africa is that it does not have the financial means today to protect and revive its economy like all the other continents have done," French Finance Minister Bruno Le Maire told RFI radio in May." World finance chiefs agreed in April to boost reserves (SDR) at the International Monetary Fund (IMF) by $650 billion and extend a debt-servicing freeze to help developing countries deal with the pandemic, although only $34 billion will be allocated to Africa. "France wants this to go much further by reallocating SDRs that are (scheduled) for developed countries," an official from the French presidency briefed reporters ahead of the summit." Macron has said he believes Africa needs a "New Deal" to give the continent a breath of fresh air. And today, he called on G7 nations to find an agreement as part of efforts to reallocate $100 billion in IMF Special Drawing Rights (SDR) to African states. So how do we pay for the bailout? Macron told a news conference he would like the sale of gold reserves to help finance this planned aid for Africa. So is Macron about to join the hall of fame of infamous leaders selling gold at just the wrong time? Will the spotprice of Gold be affected as when Gordon Brown, UK Chancellor, sold gold in 1999? Or do you remember the effect of the sell of gold in 2016 by The Bank of Canada? Just look down at the grpah below.   The first gold coin ever minted in the United States is set for a huge private sale. There are many people who love to collect things that are old, rare, or valuable. For a select few, combining the three is ideal. That’s why the first gold coin ever made in the US is being offered for private sale with an asking price of $15 million, according to a recent report by Bloomberg News. The coin is the Brasher Doubloon, and it was struck in 1787. It was created the same year the Constitution was written, and five years before there was such an entity as a federal mint. The coin was made by a metalsmith named Ephraim Brasher, George Washington’s next-door neighbor in New York. Brasher privately minted a small number of coins, and he marked his initials on the breast of the eagle of the first of them. Given the timing and proximity, it’s very likely Washington himself handled the coin at some point. The coin’s actual purpose is a bit of a mystery. No one knows if it was made as a prototype or souvenir, or if it was made to be circulated. Brasher made seven of the doubloons, but his initials are on the eagles’ wings on the other six coins.

Thirteen stars are arranged over the eagle’s head, no doubt to refer to the thirteen colonies, and the phrase ‘E pluribus unum’ runs around the periphery, separated by stars. The date it was struck, 1787, is below that. The other shows a scene of the sun rising over a mountain. Despite the fact that Brasher stamped his initials on the eagles, most scholars seem to agree that the ‘face’ is actually the side showing the landscape. ‘Brasher’ is inscribed below the landscape, and the legends ‘Nova Eborac,’ ‘Excelsior,’ and ‘Columbia’ can be seen around the periphery of the coin, separated by quatrefoils.

China is eyeing to further boost the technological application and industrial development of blockchain over the next decade, according to a guideline released by industrial development and cyberspace affairs authorities.

By 2025, the country aims to take the comprehensive strength of its blockchain industry to the most advanced level in the world, said a document jointly released by the Ministry of Industry and Information Technology and the Office of the Central Cyberspace Affairs Commission. The country's blockchain industry and its industrial standard system shall begin to take shape by 2025, with the blockchain technology applied to multiple economic and social fields, the document noted. In the next five years, China shall support the establishment of three to five backbone enterprises with international competitiveness, as well as a number of innovation-driven enterprises and three to five blockchain industrial clusters. By 2030, the blockchain industry shall see further expansion in both comprehensive strength and industrial scale, and deepen integration with next-generation information technologies such as big data and artificial intelligence, the document added. Currently, there are around 75,000 blockchain-related enterprises in China, according to data from corporate information provider Tianyancha.

Canada, home to some of the world's largest gold-mining companies, recently announced that it had in effect liquidated all of the country's holdings of the shiny metal and is moving to what a government spokesperson described as "easily tradeable" assets. It has been a long process. Canada held 1088 tons of gold in 1955. By 2000, it was down to 46 tons. Today, just 77 ounces remain.  This puts Canada in last place - well behind Albania, Haiti, Trinidad and Tobago, and Papua New Guinea - in the most up-to-date compilation of data on gold reserves compiled by an industry group, the World Gold Council.

Canada's explanation for the sell-off is reasonable enough: actual bullion bars cannot be liquidated as easily as, say, government bonds. And over the long term, central banks and governments have generally gotten a better return by investing in safe assets such as US Treasuries. But the real question is not why Canada has sold its gold; it's why other countries remain so wedded to maintaining - even accumulating - stocks of the precious metal despite the fact that it no longer plays any role in the money supply. The reason some countries hold on to gold may have little to do with sound fiscal policy. Instead, the practice reflects the less tangible or rational weight of history. A look at which countries own the metal - and which countries do not - presents an unexpected pattern. Countries that possess significant reserves tend to have some history as global hegemons, imperial powers or economic powerhouses - or aspirations to such status. In a fascinating paper from 2012, two economists at the University of Santa Cruz, Joshua Aizenman and Kenta Inoue, crunched some numbers and found that "the intensity of holding gold is correlated with 'global power' - by the history of being a past empire". This, they said, is especially true of "countries that are or were the suppliers of key currencies". The US remains No.1, just as it remains the world's biggest economy and the issuer of the most common reserve currency. But the pattern reaches into the distant past. The Netherlands was an imperial heavyweight in the 17th century, but it lost that status long ago. Nonetheless, it holds the 10th largest gold reserves, even though it has a population of only 17 million. Portugal, a country that once possessed an empire that stretched from Brazil to Angola to Macau, has 382 tons of gold, yet only has a population of about 11 million. The better-known imperial powers - Germany, Italy, France, Russia, and of course, Britain, all have gold holdings in the global top 20. The trend extends beyond Europe. Japan, which sought to conquer much of the Pacific in the 20th century, and later became the world's second-largest economy, is ranked No.9 in gold holdings. Taiwan, which became an economic powerhouse in the second half of the 20th century, is ranked 14. Likewise, European powers without a significant history of imperial ambition don't seem to have much interest in gold. Finland, for example, is stuck between Argentina and Bolivia in its current holdings of gold. Ireland is even lower, sandwiched between Latvia and Lithuania. These nations are used to living in the shadow of a much bigger imperial power, and share a common history of having been conquered by those bigger neighbours. But there are newcomers in the top 20, too. As Aizenman and Inoue point out, it's no accident that two countries that have moved from bit players to powerhouses have been buying up gold. China is now ranked No. 6, having accumulated 1762 tons. India is ranked No.11, having amassed 557 tons. China and Indian's gold reserves, the researchers note, "increased in tandem with the sharp rise of their economic power". In other words, they're the latest countries to buy into an unspoken dogma that if you're going to be a heavyweight, you need some heavy metal. Which brings us back to Canada. It has been the plaything of empires, but has never harboured imperial ambitions of its own. And its policymakers have never felt a need to proclaim their greatness by accumulating piles of gold. As they would say to the rest of us who cling to this imperial relic: it's all in your head. |

Thank you for choosing to make a difference through your donation. We appreciate your support.

Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed