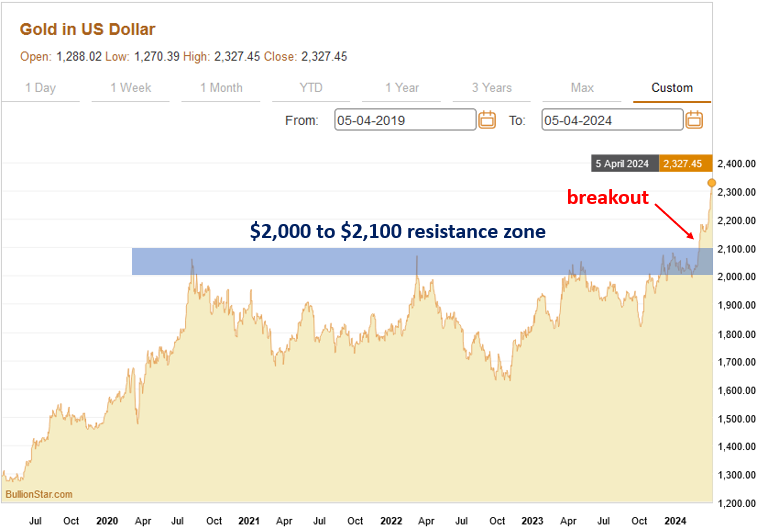

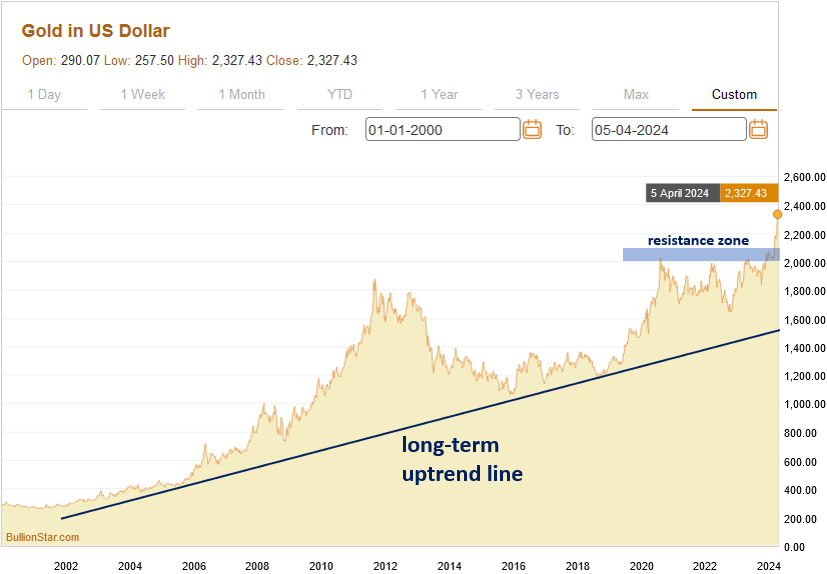

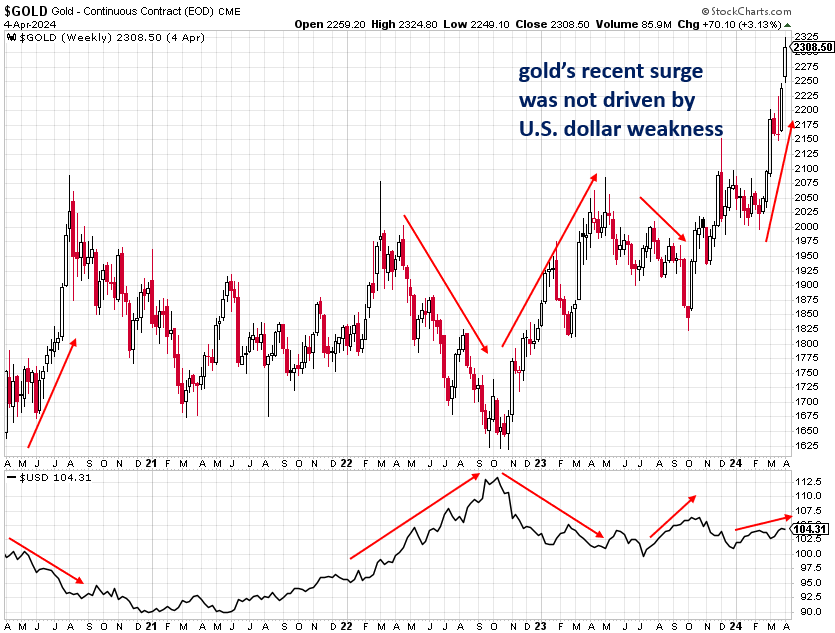

After more than three years of stagnation, gold has awakened with a vengeance since early-March and has promptly surged by nearly $300 an ounce or 14% to an all-time high $2,330 -- a sharp move for a safe-haven asset that has a reputation for its slow and steady trends. Gold’s powerful rally came seemingly out of the blue and has confounded the majority of investors and commentators who have been much more focused on trendy speculative stocks and cryptocurrencies as of late. In this piece, I will explain several of the technical and fundamental factors that are driving gold to all-time highs, what is likely ahead for gold, and how investors can best take advantage of the yellow metal’s resurgence. A Look at the Technicals The chart of gold over the past year shows how it suddenly sprang to life over the past month. There was an important technical resistance zone from $2,000 to $2,100 that had been acting as a price ceiling for gold since the middle of 2020. Gold’s successful close above that zone signified that a new rally had begun even though the fundamental drivers of it weren’t exactly apparent just yet.  Gold’s multi-decade chart shows that it has been steadily climbing an uptrend line that began in the early-2000s as the U.S. and other countries kicked off an unprecedented debt binge that shows no signs of stopping whatsoever:  Gold is Rising Despite the Strong U.S. Dollar What’s particularly interesting and notable about gold’s surge over the past month is how it has occurred independently of the action in the U.S. dollar. Gold and the U.S. dollar have a long-established inverse relationship, which means that strength in the dollar typically causes weakness in gold, while dollar weakness typically causes the price of gold to rise. The chart below compares gold (the top chart) to the U.S. Dollar Index (the bottom chart) and shows how action in the dollar often causes an opposite trend in gold. Gold’s recent surge took place while the dollar was trending slightly higher, which is a sign of gold’s strength due to its ability to buck the negative influence of the strengthening dollar.  Mainstream Investors & Journalists Missed Gold’s Rally What is also worth noting is how gold’s surprising recent rally has received very little mainstream attention by a press that is much more enamoured with hot AI stocks as well as Bitcoin and other cryptocurrencies that have recently benefited from the U.S. government’s approval of a number of Bitcoin exchange-traded funds (ETFs), which has resulted in tremendous inflows from institutional investors and retail investors alike. As the chart below shows, investors have pulled billions of dollars worth of funds from gold ETFs in order to re-invest in Bitcoin ETFs, which is ironic considering its timing shortly before gold’s lift-off (and is confirmation of contrarian investing principles). The continuation of gold’s bull market will likely lead to funds flowing back into gold ETFs, providing additional fuel for the rally. Central Banks Are Steadily Accumulating Gold Though Western retail investors (who are often considered to be the “dumb money" in the market) have been sleeping on gold before and even during its surge of the past month, central banks -- particularly those in Russia, China, Turkey, and India -- have been steadily accumulating practically all of the gold that they can get their hands on. According to the World Gold Council, central banks purchased a healthy 1,037.4 metric tons of gold in 2023 in an effort to diversify out of the U.S. dollar and other fiat currencies that are being debased at an alarming rate and into a hard asset with a six-thousand year history as sound money that cannot be printed. Chinese Investors Are Buying Up Gold Chinese investors who are seeking refuge from the country’s sinking property and stock markets are another important driver of gold’s nascent rally. Starting in the mid-2000s, China’s property and stock markets embarked on a seemingly unstoppable bull market as the country’s economy grew rapidly and the country began to increasingly flex its economic and geopolitical muscles on the world stage. Unfortunately, like Japan in the 1980s and the U.S. in the mid-2000s, China’s asset boom was actually an unsustainable bubble that was driven by copious amounts of debt and reckless speculation. As all bubbles eventually do, China’s property and stock market bubbles have burst over the past year causing at least hundreds of billions of dollars worth of losses -- including $100 billion alone from the country’s property tycoons. As faith in China’s economy and financial markets sinks, investors are turning to the old standby, gold, which has thousands of years of history in China as a superb store of value in good and bad times alike. When complex financial systems and products fail, as they currently are in China, savers and investors appreciate the simplicity and straightforward nature of physical gold. As the famous financier J. P. Morgan once said, “Gold is money. Everything else is credit." According to the World Gold Council, consumer demand for gold in China increased by a stout 16% in 2023, while demand for gold bars and coins rose by an even more impressive 27%. Retail gold buying in China has been dominated by the younger generations who face a difficult job market and are largely priced out of the country’s unaffordable housing market but find physical gold to be attainable -- even if it means buying tiny amounts of it at a time as funds allow. Indeed, one of the most popular gold bullion products among young Chinese are gold beans that weigh as little as one gram and cost approximately 600 yuan (USD$83).  Gold beans are becoming popular with young Chinese investors

0 Comments

Former US President Donald Trump is now richer than billionaire financier George Soros, after his social media company’s successful debut on Nasdaq this week added billions of dollars to his fortune.

According to the Bloomberg Billionaires Index, Trump’s net worth has soared by more than $4 billion this year to an estimated $7.8 billion. Trump ranked 328th on the list at Wednesday’s market close, while the 93-year-old Soros was down in 375th with an estimated $7.2 billion net worth. A hedge fund manager, Soros shot to infamy for crashing the British pound in 1992. Meanwhile, Trump’s increased wealth also placed him above the likes of billionaire entrepreneur and ABC ‘Shark Tank’ star Mark Cuban ($7.3 billion), Home Depot cofounder Bernie Marcus ($6.9 billion), oil-dynasty heir Gordon Getty ($6.2 billion), and Netflix cofounder Reed Hastings ($5.9 billion). The former US president’s net worth more than doubled this year thanks to his 58% stake in Trump Media & Technology Group, which effectively went public this week after merging with Digital World Acquisition Corp. Trump Media stock, whose new ticker corresponds to the former president’s initials, has attracted significant attention, gaining nearly 60% in the first half hour of trading on Monday. This comes as Trump faces hundreds of millions of dollars in growing legal fees and penalties as a result of numerous lawsuits, which the presumptive Republican presidential nominee has denounced as spurious and politically motivated. As part of a process in which New York State Attorney General Letitia James accused Trump’s business of fraud, Judge Arthur Engoron last month demanded a $454 million bond for the former president to even file an appeal. James was preparing to seize Trump’s Manhattan properties when an appeals court announced on Monday that it would reduce the bond to $175 million and extend the filing deadline by ten more days. Earlier this month, Trump was forced to raise a bond of $91.6 million to appeal a defamation judgment against E. Jean Carroll. Trump is still appealing the $5 million judgment a jury awarded to Carroll last May after determining the former president had sexually abused her.  Even before the recent turbulences around Evergrande and other property developers, the Chinese government has already been worried about a potentially overheating real estate market for several years now. In this Executive Briefing, we are providing some background on the issue and introduce one of the most impactful policy measures that has been introduced so far to reduce risks: the Three Red Lines Policy.

As China’s real estate industry accounts for around 29% of economic output, a crash of the industry could highly damage the health of the financial system and heavily affect the livelihoods of many Chinese people, who have most of their net worth invested in real estate. Taking this into account, the People’s Bank of China and the Ministry introduced the Three Red Lines Policy in August 2020, with the aim to improve the financial health of the real estate sector by reducing developers’ leverage, improving debt coverage, and increasing liquidity. Under this framework, selected large real estate developers are assessed against three criteria, after which they will be categorized into the colors green, orange, yellow, and red, deciding the extend they are allowed to grow their debt in the next year.

Three Red Lines Criteria:

What does it mean for developers? As of the beginning of 2020, only 6.3% of rated real estate developers were able to comply with all policy criteria. But since the launch of the new regulation, companies have made efforts to control their financial performance, and credit health improvements were clearly visible in 2020 H2 earning reports. In the period of June 2020 and December 2020, 90% of the companies saw an improvement in their liability to asset ratio, 81% in their net gearing ratio, and 86% in their cash to short-term debt ratio, leading to several rating upgrades of real estate developers. This trend is believed to be directly related to the introduction of the Three Red Lines Policy. Companies are actively trying to lower their liabilities by reducing the amounts of borrowings, while developers are becoming less aggressive in their expansion plans as they scale back on their land acquisition and are disposing assets not related to their core development business. In the future, this might push out smaller developers, with the real estate market being concentrated on a few dominating players. Given a transition period of three years, developers have until mid of 2023 to meet all three criteria. What is next? In recent months, China has further implemented measures to tighten the credit environment and regulate the heated real estate market. In December 2020, China’s Central Bank issued a regulation to cap property loans by banks to control real estate investment and curb housing price speculations. Divided into five categories, banks are subject to different caps on their loans and have a grace period of 4 years to meet the regulatory requirements. Another guideline for improving order in the real estate market was announced by eight government departments in July 2021, which focuses on strengthening supervision in the areas of real estate development, rental housing, brokerage, and related services over the course of the next three years. Under the principle ‘housing is for living in, not for speculation’, the government strives to clean up irregularities in the property market, with this trend expected to continue to grow in the future.  China Evergrande Group’s (恆大集團) alleged US$78 billion revenue overstatement escalates the legal peril of founder Hui Ka Yan (許家印), who now stands at the center of one of the biggest financial fraud cases in history.

The nation’s top securities regulator said the developer’s onshore unit inflated revenue by recognizing sales in advance in the two years through 2020 that led up to its default. It imposed a 4.18 billion yuan (US$581 million) fine against the unit. Evergrande’s alleged fraud dwarfs that of Luckin Coffee Inc (瑞幸咖啡) and Enron Corp, dealing a blow to the reputation of its former auditor PricewaterhouseCoopers LLP and the country’s financial oversight. It fuels concern about how widespread such accounting issues are, just as the new China Securities Regulatory Commission (CSRC) chairman is trying to tighten oversight. The fine also means Evergrande, with about US$332 billion in liabilities, will have even less money to pay off global creditors, despite a Hong Kong court ordering the company to be liquidated in late January. “The alleged fraud is shocking in its scale,” said Brock Silvers, managing director at private equity firm Kaiyuan Capital. “Hui became an expected civil and criminal target as soon as Evergrande was ordered into liquidation.” The allegations mark the latest blow for Hui, once among Asia’s richest tycoons, who oversaw a sprawling empire that spanned real estate to electric vehicles. Evergrande was one of China’s biggest developers, taking on massive debt to expand across the country as condo sales boomed. The CSRC’s action may pave the way for more serious charges against Hui, who was detained by police last year due to “suspicion of illegal crimes.” No criminal charges against Hui have been made public and his whereabouts aren’t known. The levies are administrative penalties. Regulators allege Hui instructed other personnel to “falsely inflate” annual results. The onshore unit Hengda Real Estate Group (恆大地產集團) boosted its 2019 revenue by about 214 billion yuan, and another 350 billion yuan in 2020, the regulator said. The inflated figures accounted for half of Hengda’s total revenue in 2019, and 79 percent in 2020. As the supervisor in charge, Hui used particularly “egregious” means, the regulator said. Hengda also used these inflated figures in marketing to issue a combined 20.8 billion yuan in bonds, the regulator said. Evergrande used to recognize revenue from apartments including those that were presold but yet to be delivered. The developer said last year that it changed its approach in 2021 to book revenue after the units were completed or occupied by their owners. Hengda’s auditor in 2019 and 2020 was PricewaterhouseCoopers Zhong Tian LLP (普華永道中天會計師事務所), a mainland entity affiliated with PwC’s network. PwC resigned as Evergrande’s auditor in January last year due to audit disagreements. PwC has also resigned as auditor for other Chinese developers including Sunac China Holdings Ltd (融創中國控股) and Shimao Group Holdings Ltd (世茂集團) In Hong Kong, the city’s Financial Reporting Council said in 2022 that it was looking into Evergrande’s financial statements for 2020 and expanding an investigation of an audit carried out by PwC. “The more alarming question is — given than many other real estate developers have faced financial distress — who else relied on accounting gimmickry to buy them time,” said Joel A. Gallo, an adjunct professor at New York University in Shanghai. “Regulators should pose tough questions to the industry and their auditors.” “To improve investor confidence in a sector that has weighed down the market, transparency, which has been murky so far, needs to be demonstrated,” Gallo added. The CSRC’s fine against Hengda, while among the largest ever in China, trails that of the 7.1 billion yuan slapped on fintech giant Ant Group Co (螞蟻集團) for policy violations. Hui was fined 47 million yuan for the falsified results and other alleged violations, and banned for life from capital markets activities. Other former executives Xia Haijun (夏海鈞) and Pan Darong (潘大榮) were also among people punished with fines and market bans. Once Asia’s second-richest man, worth US$42 billion at his peak in 2017, Hui has seen his wealth plummet to about US$1 billion after the developer defaulted in 2021. Evergrande’s stock has tumbled and was eventually suspended from trading.  The start of a New Year is a good time to scrutinize a portfolio and make some adjustments including adding undervalued stocks. Stocks that enjoyed big runs last year may cool off, requiring investors to search out securities they can buy low in hopes of eventually selling at a higher price. Fortunately, there are still a lot of undervalued stocks available despite the market rally that occurred in 2023. Stock market returns over the past year were uneven, with about 70% of the stocks in the S&P 500 lagging the index. Growth stocks outpaced value equities and most of the big gains were concentrated in mega-cap technology stocks. This presents investors with an opportunity to buy quality names on the cheap before they too move higher. Here are seven of the most undervalued stocks to buy for 2023.

The company’s shares are now trading at 26 times future earnings estimates, which is low by historic standards and presents a window of opportunity for investors to take a position while the price is favorable. In November, Starbucks reported better-than-expected third-quarter financial results, and subsequently announced details of a new strategic plan that will see the retail coffee chain open 17,000 new locations by 2030 even as it cuts $3 billion in costs. While ambitious, the growth strategy has done little to help lift SBUX stock. The share price is being weighed down by ongoing concerns about sales in China, where the economy is struggling, and unionization activity at home in the U.S.

The company also said that it will buy back $10 billion of its own stock over the next year and reinstated its 2023 earnings guidance. However, even with the latest move higher, GM stock still looks undervalued. The company’s shares are currently trading at just five times future earnings estimates, which is why its among the more attractive undervalued stocks. Also, the stock is up only 7% in the last 12 months and is currently trading at the same level it was at a decade ago. A note of caution that it will likely be awhile before GM recovers from last fall’s strike by the United Auto Workers union, a job action the company says cost it $800 million in lost vehicle production.

Long-term investors who are blessed with patience may want to do some bottom fishing after Nike’s latest financial results. In truth, Nike’s recent print was better-than-expected. It was the forward guidance that spooked investors. The company reported quarterly earnings per share of $1.03 versus 85 cents that had been expected among analysts. Q2 revenue was $13.39B, slightly below the forecasted $13.43B. Nike’s gross margins increased for the first time in 18 months, and inventories dropped 14% to $8 billion. Unfortunately, Nike said that it now expects full-year revenue to grow 1%, compared to a prior outlook of up mid-single digits. For the just completed fourth quarter of 2023, Nike expects revenue to be slightly negative. That news sunk NKE stock. But there is a buy-the-dip opportunity here.

However, the stock is only trading at 14 times future earnings estimates, which is low for a company of its size, and it offers a dividend payment that yields 2%. FedEx reported earnings per share of $3.99 compared to $4.18 that was expected. Despite the miss, the company’s earnings were up more than 25% from a year earlier due largely to cost-cutting initiatives. Revenue in the latest quarter declined 3% to $22.17 billion from a year earlier, also missing analysts’ estimates. Looking ahead, FedEx said that it expects a low-single-digit decline in revenue for the entire fiscal year, down from a previous forecast of flat sales. It was the second consecutive quarter that FedEx lowered its sales outlook, citing weakening demand. However, the company said that its operating income should improve in the months ahead due to its ongoing cost-cutting plan.

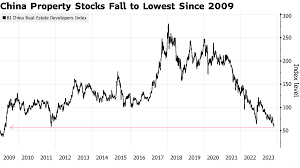

Last week, a Hong Kong court ruled that the largest indebted property developer in the world, Evergrande, would be liquidated, two years after the company defaulted on its debt in late 2021.

Much of the media reporting on the decision focused on whether foreign creditors would ever recoup their losses from Evergrande, as the Chinese government has already said it will prioritize completing the group’s existing projects, though how this will happen is less clear. But beyond the question of who will get repaid, Evergrande’s liquidation opens up a slew of larger and more profound questions about the future of the Chinese economy, especially the relationships between the central government, local governments, the private sector and households. The liquidation of Evergrande is not an accident. It is part of a larger crackdown on the private sector and government collusion that President Xi Jinping launched at the very start of his term, beginning in 2013 with the Anti-Corruption Campaign, which has become one of the most consequential and longest-running campaigns in the history of the People’s Republic of China. Taken as a whole, this crackdown has fundamentally changed the relationship between the Communist Party and the business community, creating deep distrust and fear, while leading to capital flight and a deep downturn in confidence. The Anti-Corruption Campaign was followed by other policies that put the private sector on notice that old patterns of behavior would no longer be tolerated. Xi’s “new normal” would include more discipline and oversight. Xi’s confidence in the ability of his government to implement this crackdown expanded enormously in late 2020 and early 2021, coinciding with the regime’s successful management of the COVID-19 pandemic before the arrival of the incredibly infectious omicron variant. Xi made numerous speeches and statements at the time about the importance of “common prosperity” and the need to crack down on “disorderly capital,” while also emphasizing his dislike of real estate development as investment, epitomized by his oft-quoted mantra that “houses are for living in.” The “three red lines” policy, which reined in debt-fueled property development and directly targeted firms like Evergrande that were enormously leveraged, dates back to this period. In addition to launching the attack on the over-leveraged property sector, Chinese authorities canceled the IPO of Ant Financial, forced the rewinding of Didi’s listing on the N.Y. Stock Exchange, banned private tutoring and nationalized gray rhinos, as large firms that create systemic risk, such as Anbang Insurance and HNA, are known. At the same time, in his speeches on “common prosperity,” Xi vaguely alluded to new forms of taxation and redistribution so that China would eventually become an “olive-shaped society” with a large middle class and relatively few rich and poor. But crackdowns alone cannot substitute for the deep structural reform that the Chinese economy desperately needs. Any viable solution to the property crisis and to local government’s fiscal health requires that China’s central government take on more responsibility and more accountability. Xi must shift from being a disciplinarian to accepting that these problems are not only rooted in the bad behavior of corrupt officials, greedy capitalists or overextended households. All of these actors were responding to incentives set up by China’s development model, which grew increasingly dependent on real estate and land development for growth. So while Xi talks frequently about high-quality development as the “hard truth” of his administration, this is unlikely to be achieved without a fundamental shift in responsibility upward toward the central government. In other words, it’s not just local governments and private entrepreneurs who must change their behavior—the central government must as well. Given the scale of the current crisis—over 1.5 million home purchasers are still waiting for residences that they have already paid Evergrande for—it’s possible that local governments will still be held responsible for finding other viable real estate developers to take over the unfinished projects in their regions. But local governments are themselves deeply in debt for both related and unrelated reasons. Local governments were caught up in the same frenzy of real estate development and land sales for years. But they are also reeling from debt related to COVID-19 management and testing, as well as from the basic structure of their fiscal relations with the central government, which leaves them with many mandates to fund social security and public goods like education, but without enough resources to do so. This fiscal imbalance is one of the primary reasons that local governments became so reliant on land speculation and real estate development in the first place, because in a period of ever-rising property prices, it provided much-needed revenue. It was also, not coincidentally, an excellent mechanism for local officials to collude with real estate developers to become personally wealthy. As a result, local governments are implicated in the accumulated problems of overinvestment and corruption. But any long-term solution will require changes to the tax system, so that they have sufficient tax revenue to pay for the disproportionate amount of governance they are tasked with. This will by necessity include more directly taxing both the wealthy and property, and directing more tax revenue to localities instead of the central government. Requiring local governments to find “viable developers” to take over Evergrande’s unfinished homes also ignores how Evergrande’s problems are only the tip of the iceberg of real estate development debt. It is not even clear which developers are viable enough to take on the burden of finishing the homes Evergrande has already been paid for, while also attempting to make money on new development, given China’s significant overbuilding and declining property values. A new International Monetary Fund report on the Chinese economy estimates that China’s fundamental demand for housing will decrease by 50 percent over the next decade, even as media reports indicate a current oversupply in excess of 50 million homes. The real estate sector cannot deal with these problems alone, but most local governments are in no position to help. An effective solution will require that the central government allow for substantial restructuring of existing firms and perhaps direct bailouts to households currently left holding the bag. The IMF estimates that such measures will cost about 5 percent of GDP but will be offset by avoiding longer-term losses. For households, the real estate sector’s unraveling is hitting their pocketbooks directly. Because of China’s presale model of development, households have already paid for the promised properties, so they cannot be expected to pay more, especially when the value of these future properties are going down. Meanwhile, investments in existing property are the most important source of wealth for China’s urbanites, representing about 70 percent of household wealth. So the contraction in the real estate sector, while necessary, will make many Chinese poorer. Employment opportunities have also worsened, as the real estate decline affects not just construction, but everything else tied to property, from landscaping to interior design. All of these impacts will exacerbate the problem of consumer confidence, inducing households to save rather than spend, an incentive structure that is already reinforced by China’s weak social safety net. This in turn means that China will be forced to look to external markets to absorb excess capacity in everything from building materials to electric vehicles, further exacerbating imbalances that are complicating China’s relations with trade partners. Once again, any effective policy to address the problem of consumer confidence will similarly require more support from the central government and improvements to China’s underfunded and shallow welfare state. The risk of social unrest is still low due to strong state capacity to repress street protests. But Chinese households have already shown ingenious ways to express their displeasure through inaction, such as not paying mortgages and not seeking employment—the practice known as lying flat. Beijing has accomplished much with Xi’s dramatic crackdowns as he seeks to shift China’s development in a new and more sustainable direction. But the crackdowns are only the first step. They need to be followed by increased support for local governments from the central government. So far, Xi has deftly yielded sticks. Much will depend on whether he can now do the same with carrots.  China’s troubled real-estate giant the Evergrande Group has been ordered to liquidate, a move that could deal a new blow to confidence in the world’s second-largest economy. A Hong Kong court made the ruling on Monday after the company failed to convince a judge it had a workable plan to restructure some $300bn in debts. “It would be a situation where the court says enough is enough,” judge Linda Chan said. “I consider that it is appropriate for the court to make a winding up order against the company, and I so order.” The ruling follows 18 months of legal wrangling after creditor Top Shine, in 2022, filed a petition to wind up the developer in a bid to recoup its losses.  Evergrande, the world’s most indebted developer, had been granted a brief reprieve in December after arguing it needed time to refine its restructuring plan. Chan said the court had in December “made it very clear it expected to see a fully formulated and viable proposal”. Evergrande Executive Director Shawn Siu called the ruling regrettable but said the group would do “everything possible to safeguard the stability of its domestic business and operation”, which he said is independent of its Hong Kong arm. Evergrande’s default on repayments to international investors in 2021, after Beijing began cracking down on excessive borrowing for real estate, sent shockwaves through China’s property sector, which accounts for an estimated 15-30 percent of the economy. More than 50 Chinese real-estate developers have defaulted or missed payments during the past three years, according to credit ratings agency Standard and Poor’s (S&P).

Hong Kong-listed shares in Evergrande plunged by more than 20 percent following the ruling on Monday, before the city’s stock exchange halted trading in the stock. The move is the latest in a series of warning signs for China’s $18 trillion economy, whose post-COVID recovery is facing challenges ranging from crackdowns on private industry to a declining population and an exodus of foreign capital. China’s official gross domestic product (GDP) growth of 5.2 percent last year was the worst performance in decades, excluding the COVID-19 pandemic. “Evergrande’s liquidation will pose more challenges to itself and other developers, but it will only have a limited impact on the already battered property sector and the macroeconomy,” Gary Ng, an economist at Natixis in Hong Kong, said. “Household sentiment is already very cautious of units from troubled developers, and it is unlikely to worsen further. However, it may still delay the recovery of the home market and the weaker confidence may linger longer.” After Monday’s ruling in Hong Kong, the fate of Evergrande’s asset sheet is uncertain. While China signed an agreement with Hong Kong to recognise insolvency and restructuring proceedings in the Chinese cities of Shenzhen, Shanghai and Xiamen, it is unclear whether mainland courts would sanction liquidators seizing the developer’s assets in the country. Hong Kong’s common law system, adopted during the British colonial era, is distinct from China’s Communist Party-controlled courts. In 2021, a Shenzhen court recognised insolvency proceedings in Hong Kong for the first time when it accepted the standing of liquidators for the paper manufacturing firm Samson Paper. “As most of Evergrande’s assets are in mainland China, there are uncertainties about how the creditors can seize the assets and the repayment rank of offshore bondholders,” Ng said.  Gold Gains Amidst Fed Rate Cut Prospects Gold (XAU/USD) prices are inching higher on Wednesday. The precious metal has remained consistently above the crucial $2,000 level for a week, buoyed by the anticipation of interest rate cuts from the Federal Reserve next year. This sentiment is further fueled by the Fed’s recent signals indicating a possible end to its tightening phase and a shift towards rate reductions in 2024. Treasury Yields and US Dollar Response The prospect of these rate cuts has rippled through financial markets, notably impacting U.S. Treasury yields. The 10-year yield has retreated, aligning with the Fed’s unexpectedly dovish pivot. Concurrently, the U.S. dollar is experiencing a slump against major currencies, trading lower as markets bet on imminent rate cuts. This weakening of the dollar has been a contributing factor to the gold market’s current trajectory. Global Inflation and Monetary Policies The global inflation landscape is also influencing market sentiments. The U.K., for instance, reported a more significant than expected drop in inflation, reaching its lowest annual rate since September 2021. This decline has implications for the Bank of England’s monetary policy, which maintained a hawkish stance in its last meeting, emphasizing the need for a restrictive policy for an extended period. Short-Term Market Outlook In the short term, the market outlook appears cautiously optimistic for gold. The combination of a weakening dollar, declining Treasury yields, and shifting global inflation rates presents a favorable environment for gold prices. Investors, however, remain vigilant, awaiting the U.S. November PCE index report, which will offer further insight into the inflation trajectory and potentially influence the Fed’s policy decisions in the upcoming year. Technical Analysis  Gold (XAU/USD) is currently trading at 2044.90, positioned above both its 200-day moving average of 1957.36 and 50-day moving average of 1989.19. This indicates a generally bullish trend. The price is hovering between the minor support at 2009.00 and minor resistance at 2067.00, suggesting a potential consolidation phase. However, it remains below the main resistance level of 2149.00. Given its stance above key moving averages and near minor resistance, the market sentiment for gold appears cautiously bullish. Investors might watch for a breakout above the minor resistance to confirm a stronger bullish trend, or a pullback towards the main support for potential buying opportunities.

Central banks have continued their gold buying spree, with reported net monthly purchases totaling 42 tons in October, the World Gold Council (WGC) has revealed.

According to a report published last week, the figure was 41% lower than September’s revised total of 72 tons, but still 23% above the January-September monthly average of 34 tons. The People’s Bank of China (PBoC) remained the largest bullion buyer, reporting purchases of 23 tons of gold in the 12th consecutive monthly addition to its reserves. This reportedly brings the PBoC’s net purchases to 204 tons during 2023, with its overall reserves amounting to 2,215 tons. “Despite the significant increase, reported gold reserves still account for just 4% of the bank’s total international reserves,” the WGC wrote. The Central Bank of Türkiye also made a significant purchase during the month, buying 19 tons to increase its official gold reserves (central bank plus Treasury holdings) to 498 tons. Beyond these two banks, buying was more modest, the report noted. The National Bank of Poland reportedly continued adding to its gold stockpile, buying another six tons. Its holdings of the yellow metal have now risen by over 100 tons this year, to 340 tons in total. The Reserve Bank of India, the Czech National Bank, the National Bank of the Kyrgyz Republic, and the Qatar Central Bank were the other significant buyers in October. The report also noted that central bank gold purchases have heavily outweighed sales of the metal so far this year. “Even before October’s net buying, we noted that 2023 was likely to be another colossal year of central bank buying. Having started Q4 positively, this year’s central bank demand looks set to climb even higher,”  Gold prices could soon reach a record $2,500 per ounce, driven by safe-haven investor demand in the wake of global uncertainty and geopolitical tensions, some analysts are now projecting.

Futures have risen 3% in the past couple of weeks, briefly breaching the key psychological threshold of $2,000 per ounce on Tuesday. The rise marked the highest daily close so far this month, and any move above $2,006.37 per ounce this week would make it the highest weekly close since the spring, researcher Fundstrat’s technical analyst Mark Newton wrote in a note on Wednesday seen by Business Insider. “This is quite positive technically, and I expect that gold has begun its push back to new all-time highs,” wrote Newton. He believes a rise past $2,009.41 per ounce should lead to gold entering the $2,060-2,080 range. Newton told Business Insider that a breach of resistance at $2,080 would signal a “definite technical breakout,” which he expects to quickly drive gold even higher. “My technical target for gold is $2,500/oz, and it looks appealing to be long precious metals given falling real rates, rising cycles and ongoing geopolitical conflict,” he said. The analyst later clarified that his timeline for $2,500 isn't necessarily for the end of the year but is an “intermediate target.” Bullion has been rallying since the attack by Palestinian armed group Hamas on Israel on October 7. Experts and traders expect the escalation and uncertainty in the Middle East to continue driving gold prices higher. Investors traditionally turn to gold in times of market uncertainty to hedge risks and as a store of value. Bullion has been seen as a safe haven during periods of economic instability, stock market crises, military conflicts, and pandemics.  The once-glorified clean-energy stocks are now facing their darkest days, plunging the industry into a financial abyss that threatens America’s ambitious environmental aspirations. The much-touted green revolution is looking more like a red alert as the sector hemorrhages tens of billions in market value. Sure, we’re told that hundreds of billions is still pouring into renewable energy projects, despite the fact that the stock market seems to have declared a resounding “no thanks” to these ventures. The iShares Global Clean Energy ETF (Exchange-Traded Fund), the poster child for the industry, has nosedived by over 30% this year and a whopping 50% since the dawn of 2021. Not to be outdone, specific sectors are getting their fair share of punishment. The Invesco Solar ETF is down over 40% in 2023, while the First Trust Global Wind Energy ETF is witnessing losses of about 20% this year and a grim 40% since January 2021. It seems the wind has been knocked out of their sails. Blame it on rising interest rates, the industry’s newfound nemesis. These higher rates have not only increased costs but also put a damper on consumer enthusiasm, leading to a nosedive in stock valuations for companies that once promised a green utopia but are now struggling to turn a profit. Solar companies such as SolarEdge and Enphase Energy are feeling the burn as demand for their products dwindles. Meanwhile, wind energy giant Orsted is singing the blues, with shares plummeting after revealing potential multibillion-dollar write-downs on its offshore wind projects in the US. In Germany, after the Nord Stream sabotage, because, you know, energy geopolitics and straightforward plans always go hand in hand, a whopping 77% of skeptics are shaking their heads, expressing disbelief that the nation will magically conjure up 80% of electricity from renewables by 2030. I guess turning skepticism into solar power hasn’t quite hit the mainstream yet. Switzerland, the poster child for phasing out nuclear power, is now flexing its green muscles by entertaining the idea of keeping nuclear plants running longer, because who needs a clear exit strategy when you can just extend the atomic party until 2040? Biden’s green dreams are melting faster than his favorite ice cream in the sun In the US, the demise of two New Jersey wind projects is just the tip of the iceberg, with inflation, sky-high interest rates, and a supply chain in shambles throwing a wrench into the gears of Joe’s climate ambitions. Despite a whopping $369 billion in federal aid from his climate law, clean energy projects are dropping like flies. Even the postponement of a Kentucky EV battery plant by Ford and General Motors trimming their EV plans couldn’t escape the economic tempest. It seems the only thing rising faster than hopes for a clean energy revolution is the cost. But hey, who needs affordable, reliable energy when we’ve got grand climate goals, right? Biden’s green plans are becoming a chilling reality check, and it’s not just the polar ice caps feeling the heat. It’s ironic, isn’t it? Not too long ago, clean energy was hailed as the savior of our planet, but now it seems the green agenda is drowning in a sea of red ink. The S&P Global Energy index, once a shining star, has seen its value halved since 2020 – a spectacular fall from grace. Fast forward to the present, and we witness the mighty green stocks taking a severe beating. Despite the EU and US governments offering billions in tax credits and subsidies to support the so-called green transition from Russian oil and gas, investors are losing confidence faster than you can say “renewable.”

The S&P Global Clean Energy Index has experienced a gut-wrenching 30% freefall in 2023, with the biggest quarterly outflow of $1.4 billion. The once-booming sector now holds a 23% decline in total assets under management, a far cry from its heyday just a few months ago. Blame it on the current economic climate, they say – high interest rates, soaring costs, and supply chain woes are the villains of this melodrama. And let’s not forget China, the puppet master of the solar supply chain, flooding the market with cheap alternatives, undermining the EU’s dreams of a local green market. As utility stocks struggle to convert to green energy, the sector’s operating margins are squeezed. The final nail in the coffin? NextEra Energy Partners cutting its growth target by half, sending shockwaves through the renewable industry. I dismiss the sell-off as overblown, but the damage is done, and confidence in renewables has hit rock bottom. So, what’s the moral of this green tale? It turns out, going green is not just about saving the planet; it’s an expensive affair. As the renewable energy stocks hit rock bottom, analysts are left wondering: is it time to buy, or is the green dream truly over? In a deliciously ironic plot twist, Greta Thunberg is currently sizzling in the crucible of criticism for daring to support Gaza. It seems our climate crusader is now facing a cancel-culture bonanza, much like the tweet she swiftly deleted – you know, the one prophesying Armageddon and cautioning that climate change might just “wipe out humanity” unless we magically halt fossil fuel usage by the grandiose deadline of 2023. The irony is thicker than Beijing’s smog, folks. Seems like even the green warriors can’t escape the unforgiving reality of the market.  Shares in the UK’s Metro Bank were briefly suspended from trading twice on Thursday, after the stock plunged nearly 30% over reports of urgent fundraising efforts to shore up the bank’s balance sheet.

Metro Bank shares have now fallen more than 60% since September 12, when it revealed that UK regulators had failed to approve a plan that would allow Metro to run its mortgage business at a lower cost. The London Stock Exchange confirmed to CNBC that the brief suspensions were triggered by its circuit breaker mechanisms because of Metro Bank’s stock crash. The bank, which was reportedly attempting to raise £600 million ($727 million) in debt and equity, said in a statement on Thursday that it is currently considering “how best to enhance its capital resources.” The options include asking investors to help refinance $424 million worth of debt before it falls due in 2025, as well as raising hundreds of millions of pounds through the sale of debt, shares, or assets. “No decision has been made on whether to proceed with any of these options,” Metro Bank stated. Rating agency Fitch placed Metro on negative watch on Wednesday, citing increased risks to its business model, capital position, and funding. Founded by US billionaire Vernon Hill in 2010, Metro Bank became the UK’s first new high-street bank in more than a century. In 2019, it was hit by a misreporting scandal that led to the exit of its chair and chief executive.  Both the White House and the US Treasury Department raised objections on Tuesday to the decision by credit rating company Fitch to downrank the long-term US rating from AAA to AA+.

We strongly disagree with this decision,” White House press secretary Karine Jean-Pierre told reporters, claiming it “defies reality” because President Joe Biden has led the American economy to a “robust recovery.”Treasury Secretary Janet Yellen also “strongly disagreed” with Fitch’s decision, arguing it was “arbitrary and based on outdated data” and that US Treasury securities remained the world’s “preeminent safe and liquid asset.” Fitch is one of the big three US credit rating agencies, next to Moody’s and Standard & Poor’s. On Tuesday afternoon, it announced that Washington’s “long-term foreign-currency issuer default rating” would be downgraded, citing issues with governance, rising deficits, and a looming recession, among other things. The decision “reflects the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance” relative to other countries with the similar rating over the past 20 years, “that has manifested in repeated debt limit standoffs and last-minute resolutions,” Fitch said. The company predicted a growing government deficit, noting that the US debt-to-GDP ratio was currently at 100.1%, two and a half times higher than the AAA-rated countries’ median of 39.3%. Fitch also cited the Federal Reserve’s recent credit rate hikes, “weakening business investment, and a slowdown in consumption” to predict a “mild recession” in the fourth quarter of 2023 and the first quarter of 2024.

|

Thank you for choosing to make a difference through your donation. We appreciate your support.

Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed