Even before the recent turbulences around Evergrande and other property developers, the Chinese government has already been worried about a potentially overheating real estate market for several years now. In this Executive Briefing, we are providing some background on the issue and introduce one of the most impactful policy measures that has been introduced so far to reduce risks: the Three Red Lines Policy.

As China’s real estate industry accounts for around 29% of economic output, a crash of the industry could highly damage the health of the financial system and heavily affect the livelihoods of many Chinese people, who have most of their net worth invested in real estate. Taking this into account, the People’s Bank of China and the Ministry introduced the Three Red Lines Policy in August 2020, with the aim to improve the financial health of the real estate sector by reducing developers’ leverage, improving debt coverage, and increasing liquidity. Under this framework, selected large real estate developers are assessed against three criteria, after which they will be categorized into the colors green, orange, yellow, and red, deciding the extend they are allowed to grow their debt in the next year.

Three Red Lines Criteria:

What does it mean for developers? As of the beginning of 2020, only 6.3% of rated real estate developers were able to comply with all policy criteria. But since the launch of the new regulation, companies have made efforts to control their financial performance, and credit health improvements were clearly visible in 2020 H2 earning reports. In the period of June 2020 and December 2020, 90% of the companies saw an improvement in their liability to asset ratio, 81% in their net gearing ratio, and 86% in their cash to short-term debt ratio, leading to several rating upgrades of real estate developers. This trend is believed to be directly related to the introduction of the Three Red Lines Policy. Companies are actively trying to lower their liabilities by reducing the amounts of borrowings, while developers are becoming less aggressive in their expansion plans as they scale back on their land acquisition and are disposing assets not related to their core development business. In the future, this might push out smaller developers, with the real estate market being concentrated on a few dominating players. Given a transition period of three years, developers have until mid of 2023 to meet all three criteria. What is next? In recent months, China has further implemented measures to tighten the credit environment and regulate the heated real estate market. In December 2020, China’s Central Bank issued a regulation to cap property loans by banks to control real estate investment and curb housing price speculations. Divided into five categories, banks are subject to different caps on their loans and have a grace period of 4 years to meet the regulatory requirements. Another guideline for improving order in the real estate market was announced by eight government departments in July 2021, which focuses on strengthening supervision in the areas of real estate development, rental housing, brokerage, and related services over the course of the next three years. Under the principle ‘housing is for living in, not for speculation’, the government strives to clean up irregularities in the property market, with this trend expected to continue to grow in the future.

0 Comments

China Evergrande Group’s (恆大集團) alleged US$78 billion revenue overstatement escalates the legal peril of founder Hui Ka Yan (許家印), who now stands at the center of one of the biggest financial fraud cases in history.

The nation’s top securities regulator said the developer’s onshore unit inflated revenue by recognizing sales in advance in the two years through 2020 that led up to its default. It imposed a 4.18 billion yuan (US$581 million) fine against the unit. Evergrande’s alleged fraud dwarfs that of Luckin Coffee Inc (瑞幸咖啡) and Enron Corp, dealing a blow to the reputation of its former auditor PricewaterhouseCoopers LLP and the country’s financial oversight. It fuels concern about how widespread such accounting issues are, just as the new China Securities Regulatory Commission (CSRC) chairman is trying to tighten oversight. The fine also means Evergrande, with about US$332 billion in liabilities, will have even less money to pay off global creditors, despite a Hong Kong court ordering the company to be liquidated in late January. “The alleged fraud is shocking in its scale,” said Brock Silvers, managing director at private equity firm Kaiyuan Capital. “Hui became an expected civil and criminal target as soon as Evergrande was ordered into liquidation.” The allegations mark the latest blow for Hui, once among Asia’s richest tycoons, who oversaw a sprawling empire that spanned real estate to electric vehicles. Evergrande was one of China’s biggest developers, taking on massive debt to expand across the country as condo sales boomed. The CSRC’s action may pave the way for more serious charges against Hui, who was detained by police last year due to “suspicion of illegal crimes.” No criminal charges against Hui have been made public and his whereabouts aren’t known. The levies are administrative penalties. Regulators allege Hui instructed other personnel to “falsely inflate” annual results. The onshore unit Hengda Real Estate Group (恆大地產集團) boosted its 2019 revenue by about 214 billion yuan, and another 350 billion yuan in 2020, the regulator said. The inflated figures accounted for half of Hengda’s total revenue in 2019, and 79 percent in 2020. As the supervisor in charge, Hui used particularly “egregious” means, the regulator said. Hengda also used these inflated figures in marketing to issue a combined 20.8 billion yuan in bonds, the regulator said. Evergrande used to recognize revenue from apartments including those that were presold but yet to be delivered. The developer said last year that it changed its approach in 2021 to book revenue after the units were completed or occupied by their owners. Hengda’s auditor in 2019 and 2020 was PricewaterhouseCoopers Zhong Tian LLP (普華永道中天會計師事務所), a mainland entity affiliated with PwC’s network. PwC resigned as Evergrande’s auditor in January last year due to audit disagreements. PwC has also resigned as auditor for other Chinese developers including Sunac China Holdings Ltd (融創中國控股) and Shimao Group Holdings Ltd (世茂集團) In Hong Kong, the city’s Financial Reporting Council said in 2022 that it was looking into Evergrande’s financial statements for 2020 and expanding an investigation of an audit carried out by PwC. “The more alarming question is — given than many other real estate developers have faced financial distress — who else relied on accounting gimmickry to buy them time,” said Joel A. Gallo, an adjunct professor at New York University in Shanghai. “Regulators should pose tough questions to the industry and their auditors.” “To improve investor confidence in a sector that has weighed down the market, transparency, which has been murky so far, needs to be demonstrated,” Gallo added. The CSRC’s fine against Hengda, while among the largest ever in China, trails that of the 7.1 billion yuan slapped on fintech giant Ant Group Co (螞蟻集團) for policy violations. Hui was fined 47 million yuan for the falsified results and other alleged violations, and banned for life from capital markets activities. Other former executives Xia Haijun (夏海鈞) and Pan Darong (潘大榮) were also among people punished with fines and market bans. Once Asia’s second-richest man, worth US$42 billion at his peak in 2017, Hui has seen his wealth plummet to about US$1 billion after the developer defaulted in 2021. Evergrande’s stock has tumbled and was eventually suspended from trading.  Last week, a Hong Kong court ruled that the largest indebted property developer in the world, Evergrande, would be liquidated, two years after the company defaulted on its debt in late 2021.

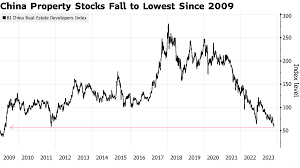

Much of the media reporting on the decision focused on whether foreign creditors would ever recoup their losses from Evergrande, as the Chinese government has already said it will prioritize completing the group’s existing projects, though how this will happen is less clear. But beyond the question of who will get repaid, Evergrande’s liquidation opens up a slew of larger and more profound questions about the future of the Chinese economy, especially the relationships between the central government, local governments, the private sector and households. The liquidation of Evergrande is not an accident. It is part of a larger crackdown on the private sector and government collusion that President Xi Jinping launched at the very start of his term, beginning in 2013 with the Anti-Corruption Campaign, which has become one of the most consequential and longest-running campaigns in the history of the People’s Republic of China. Taken as a whole, this crackdown has fundamentally changed the relationship between the Communist Party and the business community, creating deep distrust and fear, while leading to capital flight and a deep downturn in confidence. The Anti-Corruption Campaign was followed by other policies that put the private sector on notice that old patterns of behavior would no longer be tolerated. Xi’s “new normal” would include more discipline and oversight. Xi’s confidence in the ability of his government to implement this crackdown expanded enormously in late 2020 and early 2021, coinciding with the regime’s successful management of the COVID-19 pandemic before the arrival of the incredibly infectious omicron variant. Xi made numerous speeches and statements at the time about the importance of “common prosperity” and the need to crack down on “disorderly capital,” while also emphasizing his dislike of real estate development as investment, epitomized by his oft-quoted mantra that “houses are for living in.” The “three red lines” policy, which reined in debt-fueled property development and directly targeted firms like Evergrande that were enormously leveraged, dates back to this period. In addition to launching the attack on the over-leveraged property sector, Chinese authorities canceled the IPO of Ant Financial, forced the rewinding of Didi’s listing on the N.Y. Stock Exchange, banned private tutoring and nationalized gray rhinos, as large firms that create systemic risk, such as Anbang Insurance and HNA, are known. At the same time, in his speeches on “common prosperity,” Xi vaguely alluded to new forms of taxation and redistribution so that China would eventually become an “olive-shaped society” with a large middle class and relatively few rich and poor. But crackdowns alone cannot substitute for the deep structural reform that the Chinese economy desperately needs. Any viable solution to the property crisis and to local government’s fiscal health requires that China’s central government take on more responsibility and more accountability. Xi must shift from being a disciplinarian to accepting that these problems are not only rooted in the bad behavior of corrupt officials, greedy capitalists or overextended households. All of these actors were responding to incentives set up by China’s development model, which grew increasingly dependent on real estate and land development for growth. So while Xi talks frequently about high-quality development as the “hard truth” of his administration, this is unlikely to be achieved without a fundamental shift in responsibility upward toward the central government. In other words, it’s not just local governments and private entrepreneurs who must change their behavior—the central government must as well. Given the scale of the current crisis—over 1.5 million home purchasers are still waiting for residences that they have already paid Evergrande for—it’s possible that local governments will still be held responsible for finding other viable real estate developers to take over the unfinished projects in their regions. But local governments are themselves deeply in debt for both related and unrelated reasons. Local governments were caught up in the same frenzy of real estate development and land sales for years. But they are also reeling from debt related to COVID-19 management and testing, as well as from the basic structure of their fiscal relations with the central government, which leaves them with many mandates to fund social security and public goods like education, but without enough resources to do so. This fiscal imbalance is one of the primary reasons that local governments became so reliant on land speculation and real estate development in the first place, because in a period of ever-rising property prices, it provided much-needed revenue. It was also, not coincidentally, an excellent mechanism for local officials to collude with real estate developers to become personally wealthy. As a result, local governments are implicated in the accumulated problems of overinvestment and corruption. But any long-term solution will require changes to the tax system, so that they have sufficient tax revenue to pay for the disproportionate amount of governance they are tasked with. This will by necessity include more directly taxing both the wealthy and property, and directing more tax revenue to localities instead of the central government. Requiring local governments to find “viable developers” to take over Evergrande’s unfinished homes also ignores how Evergrande’s problems are only the tip of the iceberg of real estate development debt. It is not even clear which developers are viable enough to take on the burden of finishing the homes Evergrande has already been paid for, while also attempting to make money on new development, given China’s significant overbuilding and declining property values. A new International Monetary Fund report on the Chinese economy estimates that China’s fundamental demand for housing will decrease by 50 percent over the next decade, even as media reports indicate a current oversupply in excess of 50 million homes. The real estate sector cannot deal with these problems alone, but most local governments are in no position to help. An effective solution will require that the central government allow for substantial restructuring of existing firms and perhaps direct bailouts to households currently left holding the bag. The IMF estimates that such measures will cost about 5 percent of GDP but will be offset by avoiding longer-term losses. For households, the real estate sector’s unraveling is hitting their pocketbooks directly. Because of China’s presale model of development, households have already paid for the promised properties, so they cannot be expected to pay more, especially when the value of these future properties are going down. Meanwhile, investments in existing property are the most important source of wealth for China’s urbanites, representing about 70 percent of household wealth. So the contraction in the real estate sector, while necessary, will make many Chinese poorer. Employment opportunities have also worsened, as the real estate decline affects not just construction, but everything else tied to property, from landscaping to interior design. All of these impacts will exacerbate the problem of consumer confidence, inducing households to save rather than spend, an incentive structure that is already reinforced by China’s weak social safety net. This in turn means that China will be forced to look to external markets to absorb excess capacity in everything from building materials to electric vehicles, further exacerbating imbalances that are complicating China’s relations with trade partners. Once again, any effective policy to address the problem of consumer confidence will similarly require more support from the central government and improvements to China’s underfunded and shallow welfare state. The risk of social unrest is still low due to strong state capacity to repress street protests. But Chinese households have already shown ingenious ways to express their displeasure through inaction, such as not paying mortgages and not seeking employment—the practice known as lying flat. Beijing has accomplished much with Xi’s dramatic crackdowns as he seeks to shift China’s development in a new and more sustainable direction. But the crackdowns are only the first step. They need to be followed by increased support for local governments from the central government. So far, Xi has deftly yielded sticks. Much will depend on whether he can now do the same with carrots.  China’s troubled real-estate giant the Evergrande Group has been ordered to liquidate, a move that could deal a new blow to confidence in the world’s second-largest economy. A Hong Kong court made the ruling on Monday after the company failed to convince a judge it had a workable plan to restructure some $300bn in debts. “It would be a situation where the court says enough is enough,” judge Linda Chan said. “I consider that it is appropriate for the court to make a winding up order against the company, and I so order.” The ruling follows 18 months of legal wrangling after creditor Top Shine, in 2022, filed a petition to wind up the developer in a bid to recoup its losses.  Evergrande, the world’s most indebted developer, had been granted a brief reprieve in December after arguing it needed time to refine its restructuring plan. Chan said the court had in December “made it very clear it expected to see a fully formulated and viable proposal”. Evergrande Executive Director Shawn Siu called the ruling regrettable but said the group would do “everything possible to safeguard the stability of its domestic business and operation”, which he said is independent of its Hong Kong arm. Evergrande’s default on repayments to international investors in 2021, after Beijing began cracking down on excessive borrowing for real estate, sent shockwaves through China’s property sector, which accounts for an estimated 15-30 percent of the economy. More than 50 Chinese real-estate developers have defaulted or missed payments during the past three years, according to credit ratings agency Standard and Poor’s (S&P).

Hong Kong-listed shares in Evergrande plunged by more than 20 percent following the ruling on Monday, before the city’s stock exchange halted trading in the stock. The move is the latest in a series of warning signs for China’s $18 trillion economy, whose post-COVID recovery is facing challenges ranging from crackdowns on private industry to a declining population and an exodus of foreign capital. China’s official gross domestic product (GDP) growth of 5.2 percent last year was the worst performance in decades, excluding the COVID-19 pandemic. “Evergrande’s liquidation will pose more challenges to itself and other developers, but it will only have a limited impact on the already battered property sector and the macroeconomy,” Gary Ng, an economist at Natixis in Hong Kong, said. “Household sentiment is already very cautious of units from troubled developers, and it is unlikely to worsen further. However, it may still delay the recovery of the home market and the weaker confidence may linger longer.” After Monday’s ruling in Hong Kong, the fate of Evergrande’s asset sheet is uncertain. While China signed an agreement with Hong Kong to recognise insolvency and restructuring proceedings in the Chinese cities of Shenzhen, Shanghai and Xiamen, it is unclear whether mainland courts would sanction liquidators seizing the developer’s assets in the country. Hong Kong’s common law system, adopted during the British colonial era, is distinct from China’s Communist Party-controlled courts. In 2021, a Shenzhen court recognised insolvency proceedings in Hong Kong for the first time when it accepted the standing of liquidators for the paper manufacturing firm Samson Paper. “As most of Evergrande’s assets are in mainland China, there are uncertainties about how the creditors can seize the assets and the repayment rank of offshore bondholders,” Ng said.  Swedish home prices continued to slide in March as stubborn inflation and surging borrowing costs extend a housing market crunch in the country. Residential property prices in the largest Nordic economy declined by 0.8% last month, data from the state-owned mortgage lender SBAB published on Monday showed. The decline had slowed to 0.6% in February, but most experts say housing prices will continue to fall and may even surpass the forecast 20% drop-off. Housing prices plunged by 15% in nominal terms last year, driven by surging inflation and interest rate hikes by the central bank. The worst housing-price slump in three decades in Sweden has contributed to a surge in defaults, particularly in the construction industry, which is responsible for 11% of the country’s economic output. In March, bankruptcies in the sector surged 14%, which has suppressed investment in new dwellings.

The chief economist at SBAB, Robert Boije, called the March slide “surprisingly strong” adding that he expects “significantly weaker development going forward if the Riksbank continues to raise the policy rate and inflation continues to remain at high levels.” Sweden’s housing market is the most vulnerable in the EU due to the country’s rising interest rates. Although about 64% of Swedes own their homes, many have mortgages. However, because in most cases these are not long-term, fixed-rate mortgages, there is a high degree of exposure across the sector to rising interest rates, which are now at their highest levels in more than a decade following a series of hikes by the Riksbank. Industry experts say housing prices are also strongly affected by unusually high electricity prices and warn that the decline in the Swedish property market may last for years.  Fitch has become the first rating agency to declare that China Evergrande’s overseas bonds are in default after the world’s most indebted developer failed to make a crucial interest payment this week. The announcement marked the most significant moment yet in the developer’s marathon liquidity crisis that has spread to other businesses across the country’s vast real estate sector and fuelled global concerns about the potential impact on China’s economy. Evergrande, which has liabilities exceeding $300bn, missed a Monday deadline to repay bond coupons totalling $82.5m. The group had still not transferred the funds as of Wednesday in New York, according to people familiar with the matter. Fitch stated that the company did not respond to a request for confirmation on the coupon payments, and it was therefore assuming they had not been made. Neither the company nor the Chinese government has confirmed that Evergrande has defaulted on its debts, though the company said on Friday there was “no guarantee” it could meet its debt repayments as it entered a restructuring process with assistance from local government officials. Fitch also stated on Thursday that Kaisa, another heavily indebted developer that failed to repay a $400m bond that matured on Tuesday, was in restricted default. A person familiar with the situation said that Kaisa was close to signing non-disclosure agreements with advisers to investors.

Evergrande’s debt crisis has for months transfixed international bond markets, where it has borrowed heavily and has about $19bn outstanding, compared with $12bn for Kaisa. Evergrande has missed a series of interest payments since late September, but until this week had avoided default by transferring the funds before the end of 30-day grace periods. Separately on Thursday afternoon, Yi Gang, governor of the People’s Bank of China, told a seminar in Hong Kong that Evergrande’s failure to meet its obligations was a market event and that the rights of investors would be respected.  It has been teetering on the brink of collapse for weeks but China Evergrande, the country's second biggest property developer, could be facing up to doomsday as it admitted it may not be able to meet its financial obligations. With more than US$300 billion in debts, the property developer is dealing with several looming deadlines to pay up, as attempts to save it fall through. An offshore bond payment that China Evergrande initially missed on September 23, but got a 30-day grace period on, is set to expire on Saturday with US$100 million owing. There's another US$60m interest payment too, which wasn't paid when due on September 29, and the grace period is also set to run out. Discussions for a US$5b deal for Hong Kong-listed Chinese developer Hopson to take a majority stake has also fallen through. Credit rating service Moody's has basically given the property developer a junk rating, warning that there are "weak recovery prospects for Evergrande's creditors if there is a default". Experts believe that China Evergrande's collapse is all but inevitable. The Chinese government has been reluctant to bail out the ailing property developer and the People's Bank of China governor Yi Gang has claimed the risk to the economy could be contained. Yet there are 70,000 investors in Evergrande, which has also paused construction on homes for more than 1 million home buyers.

Alarming drop in house prices Clifford Bennett, chief economist at ACY Securities, warned that China has moved further along the US style global financial crisis (GFC) pathway. China uses the property market to prop up the economy with nearly a third of gross domestic product coming from the industry. Recently, two other Chinese developers, Sinic and Fantasia, have also defaulted on payments. In further bad news, home prices in China dropped in September for the first time in six years, while real estate investment has also tanked for the first time since last year. Evergrande said real estate sales plunged about 97 per cent during peak home-buying season, with the developer selling just US$571m ($791m) since September, a tiny fraction of the US$22b it recorded in the same period last year, reported Bloomberg. If Evergrande's properties flood the market, due to its collapse, it would further drive prices down across the market causing more problems. While the Evergrande situation was already a crisis, Bennett predicted things would get much worse if property prices were to experience even greater drops. "There are the very first signs of that actually happening with prices in the 70 largest cities just reported to have fallen 0.8 per cent. Not a big deal, except they used to rise steadily and impressively. Something is happening that is more profound than a short term situation of one or two large developers being in trouble," he explained. "They are the canary in the mine. They are faltering because the easy win path of the incredible China boom of past decades, is beginning to settle back into a more typical pattern of a mature capitalist economy." Situation continues to unravel Bennett added that China, the world's second largest economy, could well be having a US-style property speculation bubble burst experience. "In the original GFC, high lending to all kinds of construction and property investment (in the US) led to a global financial crisis. China was actually the backstay then to the global economy," he noted. He added that China's continued strong growth during the GFC and the impact that had on all of Asia and Australia, certainly supported the region during the severe US and European downturn. So China's potential downturn could spell bad news for Australia considering it makes billions from the relationship, despite the trade relationships being frosty at times. So wait for doomsday October 23, 2021.  On October 4, 2021, Chinese luxury real estate developer Fantasia Holdings fails to pay $206 million in debt due. On October 3, the $260 million dollar note from Jumbo Fortune Enterprises matured. The dollar note is guaranteed by China Evergrande Group and its unit Tianji Holding Ltd. On October 4, China Evergrande and Evergrande Property announced the temporary suspension of trading without prior warning before the opening of the Hong Kong stock market. Evergrande has defaulted on the maturity interest of two US dollar bonds in late September, involving amounts of US$83.5 million and US$47.5 million respectively. Of course, these are not the only ones that face such challenges. According to the "Times Weekly" report, as of September 5 this year, a total of 274 real estate companies in mainland China have issued bankruptcy announcements. In 2020, 408 real estate companies issued bankruptcy announcements. The reason for the bankruptcy of mainland real estate companies is generally because of the rupture of the capital chain, resulting in debt defaults.

In August last year, the Chinese authorities set "three red lines" for real estate companies and restricted their financing according to the number of red lines they stepped on. Secondly, at the end of last year, the authorities also set the ratio of bank loans to developers’ own funds for real estate projects; Furthermore, since the beginning of this year, the CCP has continuously upgraded its "control" on real estate industry, controlling the housing market from the demand side, causing the rapid cooling of the market. Thus, the desire of real estate companies to speed up the sale of properties to collect the money has been dashed. The financing of real estate companies is restricted, the method of lending the new to repay the old is also blocked, and properties are generally not easy to sell. Therefore, many real estate companies’ capital chains were broken. Most of China's real estate companies quickly expand up through a high borrowing and high turnover approach, their leverage ratios are relatively high. For example, the real estate company that ranked first in sales in September- Country Garden, starts project design immediately once it acquires land plots, opens for pre-sale within 4 months, achieves positive cash flow in the 5th month, and starts to rush into a new land acquisition in the 6th month. This kind of high turnover becomes the way to maximize the interests of real estate enterprises. Under this business philosophy, the net operating cash flow of real estate companies has always been negative as a whole. In 2014, the net cash flow of all real estate companies was as high as negative 884 Billion USD. Since then, China has been forced to start destocking to improve cash flow for the real estate industry. By 2018, the net cash flow was negative 590 billion USD. By 2020, the net cash flow has deteriorated again and reached a negative 714 billion. From January to August this year, the number is negative 512 billion, and it is expected to exceed negative 776 billion USD for the entire year. Driven by greed, real estate companies do everything they can to expand rapidly, and their cash flow has always been negative. How can these companies not collapse?  The Hong Kong Stock Exchange did not say why it has suspended trading in Evergrande shares, but there is speculation that another major developer may buy out the company's property management unit. Shares of the embattled Chinese developer Evergrande were suspended on the Hong Kong stock exchange early Monday amidst heightened speculation about a potential sale. "Due to the suspension of trading in the underlying shares, trading in Futures & Options for China Evergrande Group (EVG) have been suspended until further notice," the Hong Kong Stock Exchange said in a statement, without listing a reason. This is the first time that the shares of the company, once China's top-selling developer, have been suspended. Evergrande is currently the world’s most indebted real estate group with debts surmounting billions. It could face one of China's largest-ever restructurings. The latest development comes as a Chinese financial news service, Cailian, said Evergrande’s property management unit may be taken over by another major developer.

How much does Evergrande owe? According to reports, Chinese regulators requested Evergrande avoid a near-term default on its dollar bonds and the nearly $83.5 million (€71.1 million) in dollar-bond interest payments due last month. At the same time, reports also said the central government had alerted local governments that the property giant could collapse. The payments that were due were on a $2 billion offshore bond and a $47.5 million dollar-bond. Evergrande's bonds would default if the company fails to settle the interest payment it owes within 30 days. In total, the company owes $305 billion (€262.7 billion) in the next two years. Reports said Evergrande had stopped paying staff and factory suppliers in its electrical vehicle unit. |

Thank you for choosing to make a difference through your donation. We appreciate your support.

Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed