Ruling party Pheu Thai’s boldest pledge, the 10,000 baht digital wallet handout, will be funded solely by the fiscal budget and all eligible Thais should have the money by the fourth quarter. After the National Digital Wallet Policy Committee met on Wednesday, Prime Minister Srettha Thavisin said the scheme, which will cost about 500 billion baht, will be solely funded by the 2024-2025 fiscal year budget instead of loans. “I am able to fulfil the promise I gave to people. This [handout] adheres to laws and aligns with fiscal regulations,” said the premier, who also doubles as finance minister. Deputy Finance Minister Julapun Amornvivat explained that the funding will come from three budgetary sources: 152.7 billion baht from the 2025 fiscal budget, 172.3 billion baht from the Bank for Agriculture and Agricultural Cooperatives 2025 budget, and 175 billion baht from the 2024 fiscal budget. He said the handout will be given to registered Thai citizens aged 16 and above who earn no more than 840,000 baht per tax year and have no more than 500,000 baht in their bank accounts. Recipients can use this digital wallet at specific stores within their home districts, he said, adding that these stores can use the money earned to buy goods from other stores without location restrictions.  The digital wallet cannot be used to purchase “sin” goods, fuel, services or online products, he added. Stores wishing to be part of this campaign should have a presence in the tax system, he said, adding that the money earned via this scheme cannot be withdrawn immediately. Registration procedures for both users and stores will be available in the third quarter. Julapun said the 10,000 baht will be distributed via a “super app” created by the Digital Economy and Society Ministry, which can be used by all banks in an open-loop model. He insisted that the entire process would be transparent. The government also plans to set up a committee, chaired by the National Police chief, which will include members of the Cyber Crime Investigation Bureau, to prevent fraudulent activities. It is believed that this digital wallet handout will provide a 1.2-1.6% boost to the country’s GDP, which has been badly affected by geopolitical tensions and a slow recovery from the pandemic.

0 Comments

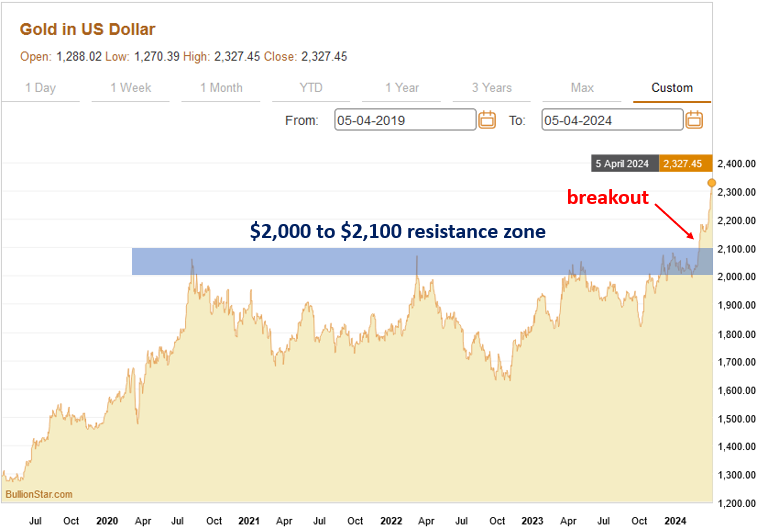

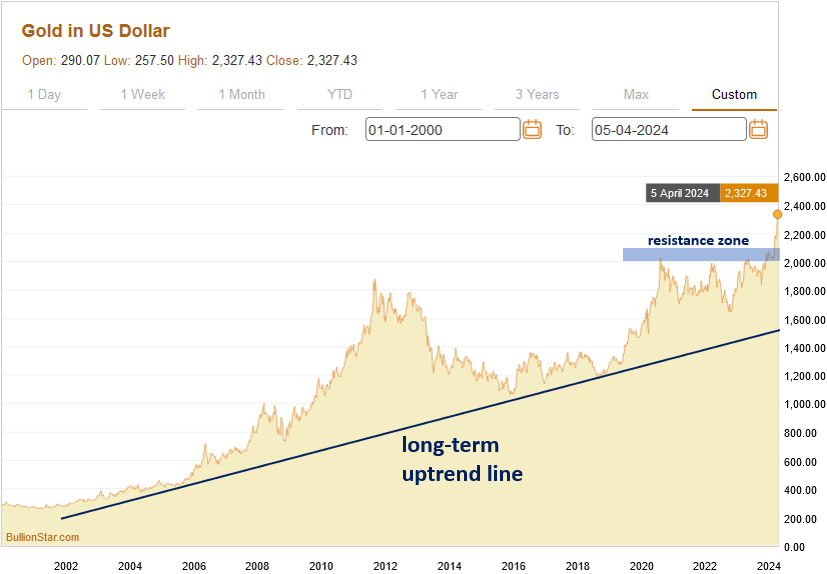

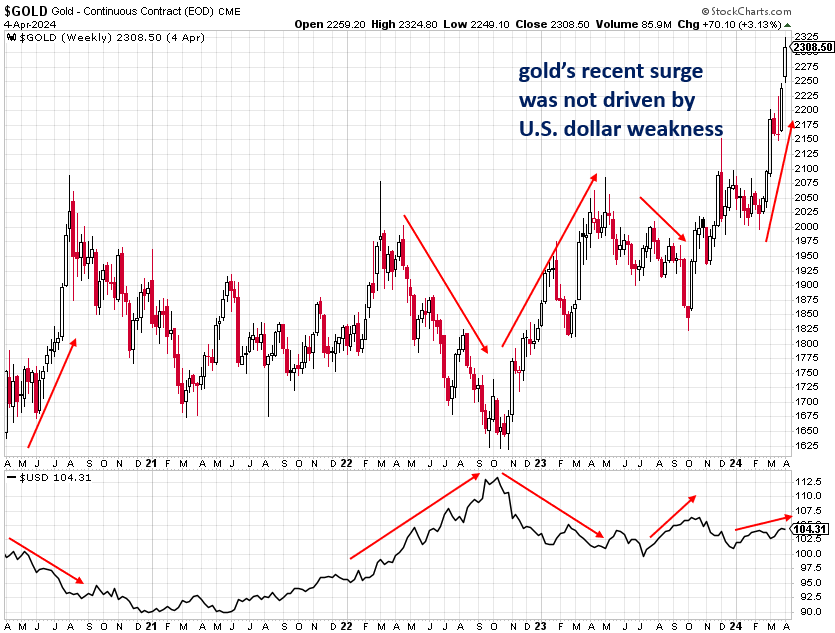

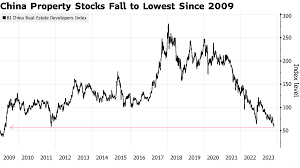

After more than three years of stagnation, gold has awakened with a vengeance since early-March and has promptly surged by nearly $300 an ounce or 14% to an all-time high $2,330 -- a sharp move for a safe-haven asset that has a reputation for its slow and steady trends. Gold’s powerful rally came seemingly out of the blue and has confounded the majority of investors and commentators who have been much more focused on trendy speculative stocks and cryptocurrencies as of late. In this piece, I will explain several of the technical and fundamental factors that are driving gold to all-time highs, what is likely ahead for gold, and how investors can best take advantage of the yellow metal’s resurgence. A Look at the Technicals The chart of gold over the past year shows how it suddenly sprang to life over the past month. There was an important technical resistance zone from $2,000 to $2,100 that had been acting as a price ceiling for gold since the middle of 2020. Gold’s successful close above that zone signified that a new rally had begun even though the fundamental drivers of it weren’t exactly apparent just yet.  Gold’s multi-decade chart shows that it has been steadily climbing an uptrend line that began in the early-2000s as the U.S. and other countries kicked off an unprecedented debt binge that shows no signs of stopping whatsoever:  Gold is Rising Despite the Strong U.S. Dollar What’s particularly interesting and notable about gold’s surge over the past month is how it has occurred independently of the action in the U.S. dollar. Gold and the U.S. dollar have a long-established inverse relationship, which means that strength in the dollar typically causes weakness in gold, while dollar weakness typically causes the price of gold to rise. The chart below compares gold (the top chart) to the U.S. Dollar Index (the bottom chart) and shows how action in the dollar often causes an opposite trend in gold. Gold’s recent surge took place while the dollar was trending slightly higher, which is a sign of gold’s strength due to its ability to buck the negative influence of the strengthening dollar.  Mainstream Investors & Journalists Missed Gold’s Rally What is also worth noting is how gold’s surprising recent rally has received very little mainstream attention by a press that is much more enamoured with hot AI stocks as well as Bitcoin and other cryptocurrencies that have recently benefited from the U.S. government’s approval of a number of Bitcoin exchange-traded funds (ETFs), which has resulted in tremendous inflows from institutional investors and retail investors alike. As the chart below shows, investors have pulled billions of dollars worth of funds from gold ETFs in order to re-invest in Bitcoin ETFs, which is ironic considering its timing shortly before gold’s lift-off (and is confirmation of contrarian investing principles). The continuation of gold’s bull market will likely lead to funds flowing back into gold ETFs, providing additional fuel for the rally. Central Banks Are Steadily Accumulating Gold Though Western retail investors (who are often considered to be the “dumb money" in the market) have been sleeping on gold before and even during its surge of the past month, central banks -- particularly those in Russia, China, Turkey, and India -- have been steadily accumulating practically all of the gold that they can get their hands on. According to the World Gold Council, central banks purchased a healthy 1,037.4 metric tons of gold in 2023 in an effort to diversify out of the U.S. dollar and other fiat currencies that are being debased at an alarming rate and into a hard asset with a six-thousand year history as sound money that cannot be printed. Chinese Investors Are Buying Up Gold Chinese investors who are seeking refuge from the country’s sinking property and stock markets are another important driver of gold’s nascent rally. Starting in the mid-2000s, China’s property and stock markets embarked on a seemingly unstoppable bull market as the country’s economy grew rapidly and the country began to increasingly flex its economic and geopolitical muscles on the world stage. Unfortunately, like Japan in the 1980s and the U.S. in the mid-2000s, China’s asset boom was actually an unsustainable bubble that was driven by copious amounts of debt and reckless speculation. As all bubbles eventually do, China’s property and stock market bubbles have burst over the past year causing at least hundreds of billions of dollars worth of losses -- including $100 billion alone from the country’s property tycoons. As faith in China’s economy and financial markets sinks, investors are turning to the old standby, gold, which has thousands of years of history in China as a superb store of value in good and bad times alike. When complex financial systems and products fail, as they currently are in China, savers and investors appreciate the simplicity and straightforward nature of physical gold. As the famous financier J. P. Morgan once said, “Gold is money. Everything else is credit." According to the World Gold Council, consumer demand for gold in China increased by a stout 16% in 2023, while demand for gold bars and coins rose by an even more impressive 27%. Retail gold buying in China has been dominated by the younger generations who face a difficult job market and are largely priced out of the country’s unaffordable housing market but find physical gold to be attainable -- even if it means buying tiny amounts of it at a time as funds allow. Indeed, one of the most popular gold bullion products among young Chinese are gold beans that weigh as little as one gram and cost approximately 600 yuan (USD$83).  Gold beans are becoming popular with young Chinese investors  The Chinese economy is expected to grow by 5.3% this year as the property sector recovers and external demand improves, the ASEAN+3 Macroeconomic Research Office (AMRO) said on Monday.

In its latest report, the Singapore-based group noted that stabilization in China’s property sector along with ongoing policy support will boost real estate investment and drive growth in the ASEAN+3 region, which consists of Southeast Asian nations plus Japan, China, and South Korea. AMRO’s projection is higher than China’s official growth target of about 5% and Bloomberg’s forecast, which expects the country’s economy to grow 4.6% this year. “China will continue to be a powerhouse in the region and the main driver of growth,” AMRO chief economist Hoe Ee Khor told Bloomberg. Weakness in the real estate sector “will take a bit of time to overcome, but it will happen and we expect the drag on growth will bottom out maybe this year.” The Chinese property sector crisis was sparked by the financial distress of major real estate developers, including property giants China Evergrande Group and Country Garden, which have defaulted on their debt. AMRO also revised upwards its overall growth outlook for ASEAN nations, predicting an expansion of 4.5% this year from 4.3% last year. According to the report, domestic demand is likely to remain resilient, underpinned by recovering investment and firm consumer spending. Within ASEAN specifically, its six major economies will continue to anchor growth. Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam are expected to contribute an average of 10% to global growth between 2024 and 2030, experts said. The organization also forecast the semiconductor industry to rebound from a multiyear slump driven by a “brisk” recovery in chips demand from China. Global semiconductor sales are expected to rise by 9.5% a year on average in 2025–2026, the group said.  In times of conflict or war, nations often undergo a significant transformation in their economic structures, transitioning towards what is commonly known as a "war economy."

This economic model is characterized by a reorientation of resources, industries, and policies to prioritize military production and defence. While such measures may be deemed necessary for national security, the consequences of a war economy can have profound impacts on both regular citizens and the countries as a whole. A war economy refers to an economic system that is heavily geared towards supporting and sustaining the efforts of a nation during times of war or conflict. In a war economy, resources, industries, and policies are mobilized to prioritize military production, defense, and logistics over other sectors of the economy. Impact on Regular People One of the most immediate and tangible consequences of a war economy is its impact on regular citizens. As resources are diverted towards military needs, shortages of consumer goods and everyday necessities can occur. Rationing may be implemented to ensure equitable distribution, leading to reduced access to essential items for ordinary people. In addition, the disruption of labor markets due to mobilization for military service or diversion to defense industries can result in unemployment and economic hardship for individuals and families. Moreover, the psychological toll of living in a state of war, with its uncertainty and fear, can lead to anxiety, stress, and trauma among the civilian population.

Impact on Countries War economies can also have far-reaching consequences for the countries involved. The significant increase in military spending can strain national finances, leading to budget deficits and debt accumulation. This economic strain may persist long after the conflict has ended, creating challenges for economic recovery and reconstruction. Moreover, countries heavily reliant on defense industries may become dependent on continued military spending for economic growth, making it difficult to transition to peacetime economies. Socially, war economies can exacerbate inequalities and divisions within society, as certain groups may benefit disproportionately from wartime contracts and opportunities, while others bear the brunt of economic hardship and sacrifice.

In conclusion, war economies represent a fundamental reorientation of a nation's economic priorities towards military production and defence. While such measures may be deemed necessary for national security during times of conflict, the consequences for regular people and countries can be profound and long-lasting. From economic hardship and social disruption to psychological trauma and dependency on military spending, the impacts of war economies are multifaceted and complex. As such, it is essential for policymakers to consider not only the short-term imperatives of war, but also the long-term consequences for the well-being and prosperity of their citizens and nations.  Sheltering from the sun on a street corner, Kridsada Ahjed rues the day he got involved with the loan sharks who now gobble up most of his daily earnings.

“I went to the loan sharks because people like me – with no assets or savings – cannot qualify to get help from legitimate banks,” Ahjed, a 40-year-old motorcycle taxi driver said. “Now almost everything I make in a day goes towards paying the interest on my debt.” Kridsada is far from alone. Thailand’s household debt reached nearly 87 percent of gross domestic product last year, according to the Bank of Thailand, among the highest on earth. Nearly $1.5bn of that debt is estimated to be made up of high-interest informal loans. Kridsada’s personal crisis is part of a wider malaise that has gripped Thailand’s economy. After decades of solid growth, Thailand is displaying all of the hallmarks of the middle-income trap, analysts say, where a combination of low productivity and poor education leaves much of the workforce stuck in low-paid, low-skilled work. “Thailand suffers not only from the slow return of demand from major export markets, but also from the changing nature of globalisation that hurts its competitiveness,” Pavida Pananond, a professor of international business at Thammasat Business School, said. “International trade is being driven more by value-added services that require higher local skills and capabilities. This requires a systemic upgrading of the labour force and local firms’ sophistication beyond short-term handouts and investment incentives.” Whereas other Southeast Asian countries are bouncing back strongly from the economic shock of the COVID-19 pandemic, Thailand has faltered. Thailand’s economy grew just 1.9 percent last year, according to state economic planners, compared with growth of 5 percent or higher in the Philippines, Indonesia and Vietnam. Even neighbouring Malaysia, a significantly more developed economy with lower expectations for growth, registered a 3.7 percent expansion. Despite the recovery of Thailand’s key tourism sector, which accounts for about one-fifth of the economy, its prospects are not looking much better in 2024. The World Bank on Monday said it expected the Thai economy to grow 2.8 percent this year, slightly better than Bangkok’s own estimates. The Philippines, Indonesia, Vietnam and Malaysia are expected to see growth of between 4.3 and 5.8 percent. Thai Prime Minister Srettha Thavisin, who came to office in August after nearly a decade of military rule, has declared the economic situation a “crisis”. Srettha, a property mogul-turned-politician, proudly calls himself the “salesman” of Thailand. Since taking power in a compromise with the royalist establishment to block the reformist Move Forward Party, the 62-year-old political neophyte has travelled the world to seek out free trade deals and promote the country as a base for global manufacturing supply chains. But after years of Bangkok shirking from fundamental economic reforms, there are fears the economy may be resistant to a quick fix. Critics say that Thailand’s military leaders for years turned off global investors, became too reliant on China’s economic rise and squandered the potential of young Thais by neglecting to fund an education system capable of producing a workforce suited to the digital era. The World Bank said in a report released last month that two-thirds of Thai youth and adults were “below the threshold levels of foundational reading literacy”, while three-quarters had poor digital literacy skills. Meanwhile, Thailand’s English language proficiency ranks among the lowest in the Association of Southeast Asian Nations (ASEAN). To stimulate the economy, Srettha has proposed providing a 10,000-baht ($280) cash handout to virtually every Thai aged more than 16 – a policy economists and political rivals have slammed as wasteful – expanding visa-free entry to more countries, and legalising casinos.  Former US President Donald Trump is now richer than billionaire financier George Soros, after his social media company’s successful debut on Nasdaq this week added billions of dollars to his fortune.

According to the Bloomberg Billionaires Index, Trump’s net worth has soared by more than $4 billion this year to an estimated $7.8 billion. Trump ranked 328th on the list at Wednesday’s market close, while the 93-year-old Soros was down in 375th with an estimated $7.2 billion net worth. A hedge fund manager, Soros shot to infamy for crashing the British pound in 1992. Meanwhile, Trump’s increased wealth also placed him above the likes of billionaire entrepreneur and ABC ‘Shark Tank’ star Mark Cuban ($7.3 billion), Home Depot cofounder Bernie Marcus ($6.9 billion), oil-dynasty heir Gordon Getty ($6.2 billion), and Netflix cofounder Reed Hastings ($5.9 billion). The former US president’s net worth more than doubled this year thanks to his 58% stake in Trump Media & Technology Group, which effectively went public this week after merging with Digital World Acquisition Corp. Trump Media stock, whose new ticker corresponds to the former president’s initials, has attracted significant attention, gaining nearly 60% in the first half hour of trading on Monday. This comes as Trump faces hundreds of millions of dollars in growing legal fees and penalties as a result of numerous lawsuits, which the presumptive Republican presidential nominee has denounced as spurious and politically motivated. As part of a process in which New York State Attorney General Letitia James accused Trump’s business of fraud, Judge Arthur Engoron last month demanded a $454 million bond for the former president to even file an appeal. James was preparing to seize Trump’s Manhattan properties when an appeals court announced on Monday that it would reduce the bond to $175 million and extend the filing deadline by ten more days. Earlier this month, Trump was forced to raise a bond of $91.6 million to appeal a defamation judgment against E. Jean Carroll. Trump is still appealing the $5 million judgment a jury awarded to Carroll last May after determining the former president had sexually abused her.  Even before the recent turbulences around Evergrande and other property developers, the Chinese government has already been worried about a potentially overheating real estate market for several years now. In this Executive Briefing, we are providing some background on the issue and introduce one of the most impactful policy measures that has been introduced so far to reduce risks: the Three Red Lines Policy.

As China’s real estate industry accounts for around 29% of economic output, a crash of the industry could highly damage the health of the financial system and heavily affect the livelihoods of many Chinese people, who have most of their net worth invested in real estate. Taking this into account, the People’s Bank of China and the Ministry introduced the Three Red Lines Policy in August 2020, with the aim to improve the financial health of the real estate sector by reducing developers’ leverage, improving debt coverage, and increasing liquidity. Under this framework, selected large real estate developers are assessed against three criteria, after which they will be categorized into the colors green, orange, yellow, and red, deciding the extend they are allowed to grow their debt in the next year.

Three Red Lines Criteria:

What does it mean for developers? As of the beginning of 2020, only 6.3% of rated real estate developers were able to comply with all policy criteria. But since the launch of the new regulation, companies have made efforts to control their financial performance, and credit health improvements were clearly visible in 2020 H2 earning reports. In the period of June 2020 and December 2020, 90% of the companies saw an improvement in their liability to asset ratio, 81% in their net gearing ratio, and 86% in their cash to short-term debt ratio, leading to several rating upgrades of real estate developers. This trend is believed to be directly related to the introduction of the Three Red Lines Policy. Companies are actively trying to lower their liabilities by reducing the amounts of borrowings, while developers are becoming less aggressive in their expansion plans as they scale back on their land acquisition and are disposing assets not related to their core development business. In the future, this might push out smaller developers, with the real estate market being concentrated on a few dominating players. Given a transition period of three years, developers have until mid of 2023 to meet all three criteria. What is next? In recent months, China has further implemented measures to tighten the credit environment and regulate the heated real estate market. In December 2020, China’s Central Bank issued a regulation to cap property loans by banks to control real estate investment and curb housing price speculations. Divided into five categories, banks are subject to different caps on their loans and have a grace period of 4 years to meet the regulatory requirements. Another guideline for improving order in the real estate market was announced by eight government departments in July 2021, which focuses on strengthening supervision in the areas of real estate development, rental housing, brokerage, and related services over the course of the next three years. Under the principle ‘housing is for living in, not for speculation’, the government strives to clean up irregularities in the property market, with this trend expected to continue to grow in the future.  China Evergrande Group’s (恆大集團) alleged US$78 billion revenue overstatement escalates the legal peril of founder Hui Ka Yan (許家印), who now stands at the center of one of the biggest financial fraud cases in history.

The nation’s top securities regulator said the developer’s onshore unit inflated revenue by recognizing sales in advance in the two years through 2020 that led up to its default. It imposed a 4.18 billion yuan (US$581 million) fine against the unit. Evergrande’s alleged fraud dwarfs that of Luckin Coffee Inc (瑞幸咖啡) and Enron Corp, dealing a blow to the reputation of its former auditor PricewaterhouseCoopers LLP and the country’s financial oversight. It fuels concern about how widespread such accounting issues are, just as the new China Securities Regulatory Commission (CSRC) chairman is trying to tighten oversight. The fine also means Evergrande, with about US$332 billion in liabilities, will have even less money to pay off global creditors, despite a Hong Kong court ordering the company to be liquidated in late January. “The alleged fraud is shocking in its scale,” said Brock Silvers, managing director at private equity firm Kaiyuan Capital. “Hui became an expected civil and criminal target as soon as Evergrande was ordered into liquidation.” The allegations mark the latest blow for Hui, once among Asia’s richest tycoons, who oversaw a sprawling empire that spanned real estate to electric vehicles. Evergrande was one of China’s biggest developers, taking on massive debt to expand across the country as condo sales boomed. The CSRC’s action may pave the way for more serious charges against Hui, who was detained by police last year due to “suspicion of illegal crimes.” No criminal charges against Hui have been made public and his whereabouts aren’t known. The levies are administrative penalties. Regulators allege Hui instructed other personnel to “falsely inflate” annual results. The onshore unit Hengda Real Estate Group (恆大地產集團) boosted its 2019 revenue by about 214 billion yuan, and another 350 billion yuan in 2020, the regulator said. The inflated figures accounted for half of Hengda’s total revenue in 2019, and 79 percent in 2020. As the supervisor in charge, Hui used particularly “egregious” means, the regulator said. Hengda also used these inflated figures in marketing to issue a combined 20.8 billion yuan in bonds, the regulator said. Evergrande used to recognize revenue from apartments including those that were presold but yet to be delivered. The developer said last year that it changed its approach in 2021 to book revenue after the units were completed or occupied by their owners. Hengda’s auditor in 2019 and 2020 was PricewaterhouseCoopers Zhong Tian LLP (普華永道中天會計師事務所), a mainland entity affiliated with PwC’s network. PwC resigned as Evergrande’s auditor in January last year due to audit disagreements. PwC has also resigned as auditor for other Chinese developers including Sunac China Holdings Ltd (融創中國控股) and Shimao Group Holdings Ltd (世茂集團) In Hong Kong, the city’s Financial Reporting Council said in 2022 that it was looking into Evergrande’s financial statements for 2020 and expanding an investigation of an audit carried out by PwC. “The more alarming question is — given than many other real estate developers have faced financial distress — who else relied on accounting gimmickry to buy them time,” said Joel A. Gallo, an adjunct professor at New York University in Shanghai. “Regulators should pose tough questions to the industry and their auditors.” “To improve investor confidence in a sector that has weighed down the market, transparency, which has been murky so far, needs to be demonstrated,” Gallo added. The CSRC’s fine against Hengda, while among the largest ever in China, trails that of the 7.1 billion yuan slapped on fintech giant Ant Group Co (螞蟻集團) for policy violations. Hui was fined 47 million yuan for the falsified results and other alleged violations, and banned for life from capital markets activities. Other former executives Xia Haijun (夏海鈞) and Pan Darong (潘大榮) were also among people punished with fines and market bans. Once Asia’s second-richest man, worth US$42 billion at his peak in 2017, Hui has seen his wealth plummet to about US$1 billion after the developer defaulted in 2021. Evergrande’s stock has tumbled and was eventually suspended from trading. Why China’s frustrated Youth are Ready to ‘let it rot’ Early this month China’s president Xi Jinping encouraged the country’s youth to establish “great ideals” and incorporate their personal goals into the “bigger picture” of the Chinese nation and people. “‘China’s hope lies in youth,” he said in a major speech.

But on China’s internet, some young people say their “ideals” simply cannot be achieved and many of them have given up on trying. Frustrated by the mounting uncertainties and lack of economic opportunities, they are resorting to a new buzzword – bai lan (摆烂, or let it rot in English) – to capture their attitude towards life. The phrase, bai lan, which has its origin in NBA games, means a voluntary retreat from pursuing certain goals because one realises they are simply too difficult to achieve. In American basketball, it often refers to a team’s deliberate loss of a game in order to get a better draft pick. On Weibo, the bai lan-related topics have generated hundreds of millions of reads and discussions since March. Netizens also created different variations of the bai lan attitude. “Properties in Shanghai too expensive? Fine, I’ll just rent all my life, as I can’t afford it if I only earn a monthly salary anyway,” one grumbled. In recent days, this phrase – and more previously ‘tang ping’ (lying flat, 躺平), which means rejecting gruelling competition for a low desire life – gained popularity as severe competition and high social expectations prompted many young Chinese to give up on hard work. But bai lan has a more worrying layer in the way it is being used by young people in China: to actively embrace a deteriorating situation, rather than trying to turn it around. It is close to other Chinese phrases, for example ‘to smash a cracked pot’ (破罐破摔) and ‘dead pigs are not afraid of boiling water’ (死猪不怕开水烫). State media have taken note of this trend. “Why modern young Chinese like to ‘bai lan’?” one recent article in official media outlet asked. “In fact, this is as a result of negative auto suggestion, repeatedly telling oneself I cannot make it… And this kind of mentality often leads people to adopt the ‘bai lan’ attitude.” But the reality is not quite as state media suggested, says Sal Hang, a 29-year-old creative industry professional in Beijing. He says that for his generation of young Chinese, this attitude of letting things rot is likely to be caused by a lack of social mobility and increased uncertainty in today’s China. “Unlike my parents’ generation, young Chinese today have much bigger expectations, but there are many more uncertainties for us, too. For example, we cannot make any long-term plans for our lives any more, because we do not know what is going to happen to us even five years down the road.” After working as a flight engineer in south-western China, Hang moved to Beijing three years ago to work in music, his passion. But the workplace reality changed his initial ambition. “My boss often sets unrealistic targets for me. But however hard I try to meet his KPIs, I always fail. So in the end, I lose my motivation and just do my bare minimum.” Prof Mary Gallagher, director of the Centre for Chinese Studies at the University of Michigan, says ‘bai lan’ is not necessarily a sentiment unique to China. “It is a bit like the ‘slacker’ generation in America in the 1990s. And like ‘tang ping’ last year, it is also a rejection against the ultra-competitiveness of today’s Chinese society.” But in today’s China, the sense of hopelessness among the young is further exacerbated by shrinking economic opportunities, she says. In the past few months, while hundreds of millions of Chinese people were confined to their homes due to Covid lockdowns, the world’s second-largest economy also found itself struggling to boost growth. More than 18% of young Chinese people aged between 16 and 24 were jobless in April – the highest since the official record began. “Hard to find a job after graduation this year? Fine, I’ll just bai lan – stay at home and watch TV all day,” wrote one netizen who struggled to find work, despite China’s top leader urged young people to fight for the future. Kecheng Fang, a media professor at the Chinese University of Hong Kong, says young Chinese use ‘bai lan’ or ‘tang ping’ to show they are not cooperating with the official narrative. “All these popular phrases reflect a shared social emotion of the day. When people use them, they are not just expressing themselves, but looking for a connection with those who have the same feeling,” he says. “Despite the grand official narrative from the leaders, in real life, we are all in the same situation, after all.”  The start of a New Year is a good time to scrutinize a portfolio and make some adjustments including adding undervalued stocks. Stocks that enjoyed big runs last year may cool off, requiring investors to search out securities they can buy low in hopes of eventually selling at a higher price. Fortunately, there are still a lot of undervalued stocks available despite the market rally that occurred in 2023. Stock market returns over the past year were uneven, with about 70% of the stocks in the S&P 500 lagging the index. Growth stocks outpaced value equities and most of the big gains were concentrated in mega-cap technology stocks. This presents investors with an opportunity to buy quality names on the cheap before they too move higher. Here are seven of the most undervalued stocks to buy for 2023.

The company’s shares are now trading at 26 times future earnings estimates, which is low by historic standards and presents a window of opportunity for investors to take a position while the price is favorable. In November, Starbucks reported better-than-expected third-quarter financial results, and subsequently announced details of a new strategic plan that will see the retail coffee chain open 17,000 new locations by 2030 even as it cuts $3 billion in costs. While ambitious, the growth strategy has done little to help lift SBUX stock. The share price is being weighed down by ongoing concerns about sales in China, where the economy is struggling, and unionization activity at home in the U.S.

The company also said that it will buy back $10 billion of its own stock over the next year and reinstated its 2023 earnings guidance. However, even with the latest move higher, GM stock still looks undervalued. The company’s shares are currently trading at just five times future earnings estimates, which is why its among the more attractive undervalued stocks. Also, the stock is up only 7% in the last 12 months and is currently trading at the same level it was at a decade ago. A note of caution that it will likely be awhile before GM recovers from last fall’s strike by the United Auto Workers union, a job action the company says cost it $800 million in lost vehicle production.

Long-term investors who are blessed with patience may want to do some bottom fishing after Nike’s latest financial results. In truth, Nike’s recent print was better-than-expected. It was the forward guidance that spooked investors. The company reported quarterly earnings per share of $1.03 versus 85 cents that had been expected among analysts. Q2 revenue was $13.39B, slightly below the forecasted $13.43B. Nike’s gross margins increased for the first time in 18 months, and inventories dropped 14% to $8 billion. Unfortunately, Nike said that it now expects full-year revenue to grow 1%, compared to a prior outlook of up mid-single digits. For the just completed fourth quarter of 2023, Nike expects revenue to be slightly negative. That news sunk NKE stock. But there is a buy-the-dip opportunity here.

However, the stock is only trading at 14 times future earnings estimates, which is low for a company of its size, and it offers a dividend payment that yields 2%. FedEx reported earnings per share of $3.99 compared to $4.18 that was expected. Despite the miss, the company’s earnings were up more than 25% from a year earlier due largely to cost-cutting initiatives. Revenue in the latest quarter declined 3% to $22.17 billion from a year earlier, also missing analysts’ estimates. Looking ahead, FedEx said that it expects a low-single-digit decline in revenue for the entire fiscal year, down from a previous forecast of flat sales. It was the second consecutive quarter that FedEx lowered its sales outlook, citing weakening demand. However, the company said that its operating income should improve in the months ahead due to its ongoing cost-cutting plan.

Light-emitting diodes (LEDs) have revolutionized modern lighting and display technology, offering energy efficiency, durability, and versatility. Among the myriad colors they can emit, the blue LED holds particular significance due to its pivotal role in advancing LED technology. This essay explores the fascinating history and development of the blue LED, tracing its journey from theoretical conception to practical realization and its transformative impact on various industries.

Early Discoveries The journey towards the blue LED began with fundamental research into semiconductor physics and materials science. In the 1950s and 1960s, scientists were exploring the properties of different materials and experimenting with semiconductor junctions to understand their behavior. It was in this era that researchers first observed electroluminescence, the phenomenon of a material emitting light when subjected to an electric current. In 1972, Herbert Paul Maruska and Jacques Pankove at RCA Laboratories achieved the first demonstration of a blue-emitting LED using zinc-doped gallium nitride (GaN:Zn). However, the efficiency and practicality of these early blue LEDs were limited, and they remained a scientific curiosity rather than a commercially viable technology. Breakthroughs in Materials Science The quest for a commercially feasible blue LED gained momentum in the 1980s and 1990s as researchers delved deeper into materials science and semiconductor engineering. Shuji Nakamura, a Japanese engineer working at Nichia Corporation, made significant breakthroughs in this field. Nakamura focused on developing gallium nitride (GaN) based semiconductors, which had the potential to emit blue light when appropriately doped and fabricated. In 1993, Nakamura succeeded in creating the first high-brightness blue LED using gallium nitride. He achieved this breakthrough by inventing a new method for growing high-quality GaN crystals, known as metalorganic chemical vapor deposition (MOCVD). This innovation significantly improved the efficiency and reliability of blue LEDs, paving the way for their commercialization. Commercialization and Applications The commercialization of blue LEDs marked a turning point in the lighting industry. Blue LEDs, when combined with red and green LEDs, enabled the creation of white light, opening up new possibilities for energy-efficient lighting solutions. The development of blue LED backlighting also revolutionized the display industry, leading to thinner, brighter, and more vibrant displays in devices such as smartphones, televisions, and laptops. Moreover, blue LEDs found applications beyond lighting and displays. They became essential components in optical storage devices like Blu-ray discs, which utilize blue laser diodes for high-density data storage. Additionally, blue LEDs have been instrumental in the advancement of medical and scientific instrumentation, including fluorescence microscopy and photodynamic therapy. Recognition and Impact In recognition of his pioneering work on blue LEDs, Shuji Nakamura was awarded the Nobel Prize in Physics in 2014, alongside Isamu Akasaki and Hiroshi Amano, who also made significant contributions to LED technology. Their groundbreaking research not only revolutionized lighting and display technology but also contributed to energy conservation and sustainability efforts worldwide. The history and development of the blue LED exemplify the power of scientific inquiry, technological innovation, and interdisciplinary collaboration. From humble beginnings as a scientific curiosity to becoming an indispensable component of modern technology, the blue LED has illuminated our world in more ways than one. As we continue to push the boundaries of materials science and engineering, the legacy of the blue LED serves as a beacon of inspiration for future innovations yet to come.  Yemen’s Houthi rebels have attempted to use a submersible drone for the first time, but it was destroyed in yet another wave of US-led coalition attacks over the weekend, the US Central Command has claimed.

The US Navy conducted a series of five strikes, hitting three Houthi cruise missiles, an unmanned surface vessel (USV), and one unmanned underwater vessel (UUV) on Saturday, CENTCOM announced on X (formerly Twitter) on Sunday. “This is the first observed Houthi employment of a UUV since attacks began in Oct. 23,” the US military wrote, claiming it presented an “imminent threat” to US Navy ships and commercial vessels in the area. Since the beginning of the Israeli military operation in Gaza, the Houthi militants, who are in control of a large portion of Yemen, have harassed multiple vessels sailing the Red Sea. In solidarity with the Palestinians in Gaza, the Houthis vowed to attack any ships they find to be linked to Israel until the siege of Gaza stops. In response, the US launched an international maritime coalition to patrol the Red Sea called ‘Prosperity Guardian’, with the stated goal of protecting shipping lanes. Since mid-January, the US and UK have carried out air- and sea-launched attacks against “multiple underground storage facilities, command and control, missile systems, UAV storage and operations sites, radars, and helicopters” in Yemen in an attempt to “degrade Houthi capabilities” to attack military vessels and merchant ships. The Houthis vowed to “meet escalation with escalation” and expanded their list of potential targets to include US- and UK-owned merchant vessels. While no Houthi missiles have hit a US Navy vessel thus far, the group has launched scores of missiles and drones against the US-led coalition ships in the Red Sea. The attacks on Suez Canal freight – a route which normally accounts for around 15% of the world’s commercial shipping – have forced major companies to avoid the Red Sea altogether and sail around the coast of Africa, facing increased costs and spiking insurance premiums. On Sunday, another vessel sailing off the coast of Yemen was hit, according to the United Kingdom Maritime Trade Operations. The master of the ship reported an “explosion in close proximity of the vessel resulting in damage,” adding that all crew members were safe.  The British economy fell into recession in the final quarter of 2023, according to official figures released on Thursday.

GDP dropped by 0.3% in the fourth quarter following a 0.1% decline in the previous quarter, the Office for National Statistics (ONS) has said. A technical recession is typically defined as two successive quarters of contracting output. All three main sectors of the economy – services, production, and construction – posted declines in the fourth quarter, according to the ONS. For the whole of 2023, the economy is estimated to have increased by 0.1%, which the ONS described as “the weakest annual change in real GDP since the financial crisis in 2009,” excluding the pandemic year of 2020. In 2022, growth stood at 4.3%. According to the government, high inflation has been the single biggest barrier to growth. Although price growth in the country has come down from the 11% peak recorded in 2022 and stood at 4% as of January, it’s still double the Bank of England’s 2% target. Some economists also partially attribute the weak economic performance to the effects of Brexit.The data released on Thursday represents a preliminary estimate and is subject to revision, the ONS note  The UK has paid a high price for Brexit, which has spurred inflation and trimmed the size of its economy, Bloomberg reported on Monday, citing economists from Goldman Sachs.

The country's departure from the EU has reduced Britain’s real GDP by about 5%, compared to the performance of its economic peers, according to Goldman’s chief European economist, Sven Jari Stehn. Seven years on from the referendum campaign, Britain has ended up with an underperforming economy and soaring cost of living due to reduced international trade, weak business investment, and a reduction in migrants coming from the EU, the UK’s largest trade partner, the experts noted. “The evidence points to a significant long-run output cost of Brexit,” Goldman Sachs’ economists wrote in a note. “The UK has significantly underperformed other advanced economies since the 2016 EU referendum.” Previous estimates from other observers also pointed to a long-term negative impact of Brexit. The UK’s National Institute of Economic and Social Research (NIESR) estimated in November that Brexit had reduced the size of the economy by 2-3%, an impact that is expected to rise to 5-6% by 2035. According to estimates made last year by the UK’s Office for Budget Responsibility, the exit from the EU likely reduced economic output by 4%. However, not all of the UK’s economic woes can be linked to the departure from the EU, according to the Goldman economists. Brexit headwinds come on top of the damage caused by the Covid-19 pandemic, the energy crisis triggered by the Ukraine conflict, and the high interest rates required to tame inflation, which is at historic highs in Britain. |

Thank you for choosing to make a difference through your donation. We appreciate your support.

Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed