China’s central bank purchased gold for its reserves for a 17th straight month in March, extending a buying spree that has helped the precious metal surge to a record.

Bullion held by the People’s Bank of China rose 0.2% to 72.74 million troy ounces last month, according to official data released Sunday. It’s the smallest increase in the run of monthly purchases that began in November 2022. The precious metal has been on a tear in the past two months, hitting a procession of records on expectations that lower US interest rates are on the horizon. Central bank buying has also been a significant driver of its strength since 2022. Global central banks, led by China and India, continued adding to their gold reserves in February, marking a ninth straight month of growth, according to the World Gold Council. However, the figure for February showed a 58% decline from the previous month, stemming in part from a higher volume of sales. China’s official reserve assets in March rose to the highest since November 2015. The country’s foreign exchange reserves rose to $3.2457 trillion, the highest since December 2021, as the central bank aims to maintain stable holdings to fend off risks. They rose 0.6% from February and were up 1.9% from a year earlier. Gold’s scorching run to an all-time high may seem easy to explain from a distance, given the fractious geopolitical climate and murky outlook for the global economy. A few weeks ago, when the gold price hit a record high, no one besides a few gold bugs seemed to care. After a long day of berating the Chinese government about overcapacity in their economy, US Treasury Secretary Janet Yellen joined China’s Vice Premier He Lifeng for a boat cruise on the Pearl River on Friday evening in the southern megacity of Guangzhou.

0 Comments

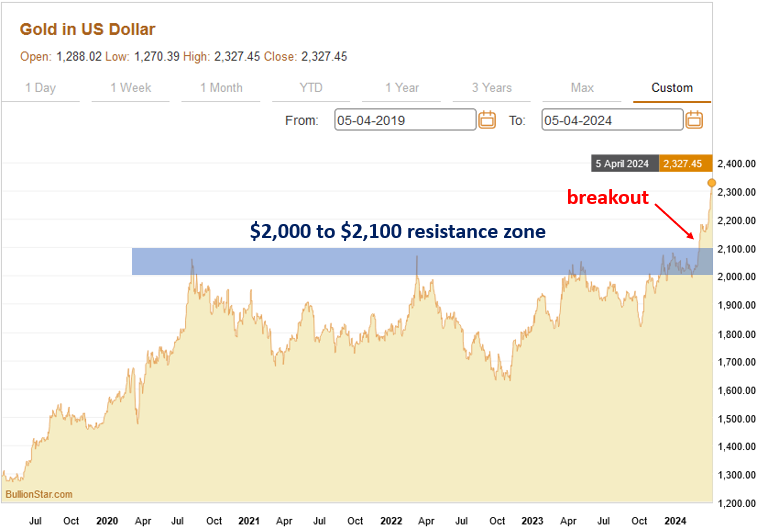

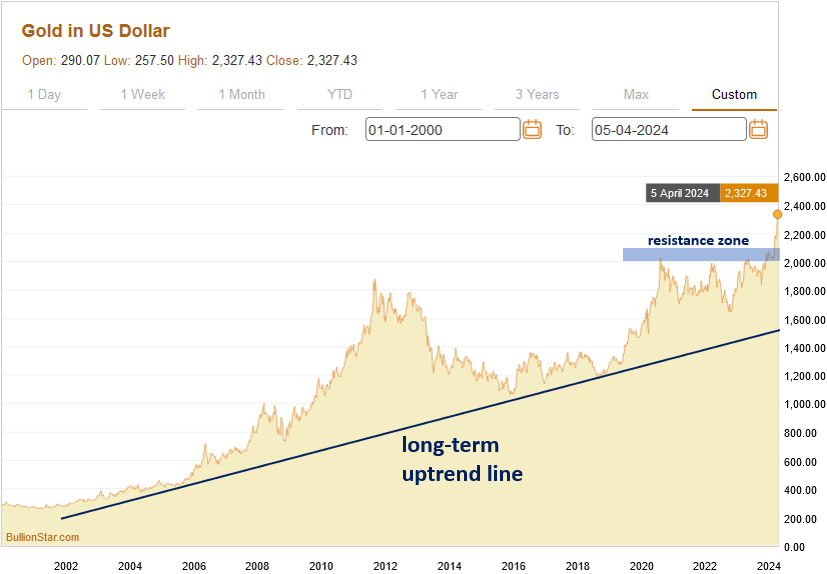

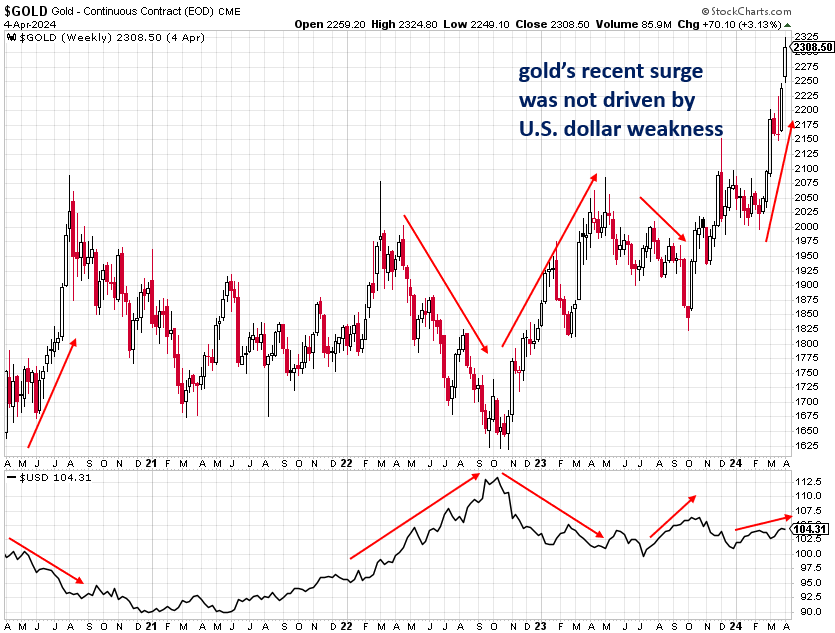

After more than three years of stagnation, gold has awakened with a vengeance since early-March and has promptly surged by nearly $300 an ounce or 14% to an all-time high $2,330 -- a sharp move for a safe-haven asset that has a reputation for its slow and steady trends. Gold’s powerful rally came seemingly out of the blue and has confounded the majority of investors and commentators who have been much more focused on trendy speculative stocks and cryptocurrencies as of late. In this piece, I will explain several of the technical and fundamental factors that are driving gold to all-time highs, what is likely ahead for gold, and how investors can best take advantage of the yellow metal’s resurgence. A Look at the Technicals The chart of gold over the past year shows how it suddenly sprang to life over the past month. There was an important technical resistance zone from $2,000 to $2,100 that had been acting as a price ceiling for gold since the middle of 2020. Gold’s successful close above that zone signified that a new rally had begun even though the fundamental drivers of it weren’t exactly apparent just yet.  Gold’s multi-decade chart shows that it has been steadily climbing an uptrend line that began in the early-2000s as the U.S. and other countries kicked off an unprecedented debt binge that shows no signs of stopping whatsoever:  Gold is Rising Despite the Strong U.S. Dollar What’s particularly interesting and notable about gold’s surge over the past month is how it has occurred independently of the action in the U.S. dollar. Gold and the U.S. dollar have a long-established inverse relationship, which means that strength in the dollar typically causes weakness in gold, while dollar weakness typically causes the price of gold to rise. The chart below compares gold (the top chart) to the U.S. Dollar Index (the bottom chart) and shows how action in the dollar often causes an opposite trend in gold. Gold’s recent surge took place while the dollar was trending slightly higher, which is a sign of gold’s strength due to its ability to buck the negative influence of the strengthening dollar.  Mainstream Investors & Journalists Missed Gold’s Rally What is also worth noting is how gold’s surprising recent rally has received very little mainstream attention by a press that is much more enamoured with hot AI stocks as well as Bitcoin and other cryptocurrencies that have recently benefited from the U.S. government’s approval of a number of Bitcoin exchange-traded funds (ETFs), which has resulted in tremendous inflows from institutional investors and retail investors alike. As the chart below shows, investors have pulled billions of dollars worth of funds from gold ETFs in order to re-invest in Bitcoin ETFs, which is ironic considering its timing shortly before gold’s lift-off (and is confirmation of contrarian investing principles). The continuation of gold’s bull market will likely lead to funds flowing back into gold ETFs, providing additional fuel for the rally. Central Banks Are Steadily Accumulating Gold Though Western retail investors (who are often considered to be the “dumb money" in the market) have been sleeping on gold before and even during its surge of the past month, central banks -- particularly those in Russia, China, Turkey, and India -- have been steadily accumulating practically all of the gold that they can get their hands on. According to the World Gold Council, central banks purchased a healthy 1,037.4 metric tons of gold in 2023 in an effort to diversify out of the U.S. dollar and other fiat currencies that are being debased at an alarming rate and into a hard asset with a six-thousand year history as sound money that cannot be printed. Chinese Investors Are Buying Up Gold Chinese investors who are seeking refuge from the country’s sinking property and stock markets are another important driver of gold’s nascent rally. Starting in the mid-2000s, China’s property and stock markets embarked on a seemingly unstoppable bull market as the country’s economy grew rapidly and the country began to increasingly flex its economic and geopolitical muscles on the world stage. Unfortunately, like Japan in the 1980s and the U.S. in the mid-2000s, China’s asset boom was actually an unsustainable bubble that was driven by copious amounts of debt and reckless speculation. As all bubbles eventually do, China’s property and stock market bubbles have burst over the past year causing at least hundreds of billions of dollars worth of losses -- including $100 billion alone from the country’s property tycoons. As faith in China’s economy and financial markets sinks, investors are turning to the old standby, gold, which has thousands of years of history in China as a superb store of value in good and bad times alike. When complex financial systems and products fail, as they currently are in China, savers and investors appreciate the simplicity and straightforward nature of physical gold. As the famous financier J. P. Morgan once said, “Gold is money. Everything else is credit." According to the World Gold Council, consumer demand for gold in China increased by a stout 16% in 2023, while demand for gold bars and coins rose by an even more impressive 27%. Retail gold buying in China has been dominated by the younger generations who face a difficult job market and are largely priced out of the country’s unaffordable housing market but find physical gold to be attainable -- even if it means buying tiny amounts of it at a time as funds allow. Indeed, one of the most popular gold bullion products among young Chinese are gold beans that weigh as little as one gram and cost approximately 600 yuan (USD$83).  Gold beans are becoming popular with young Chinese investors

Cocoa prices have roughly doubled since the start of last year. Experts attribute the spike to poor crops in Cote d’Ivoire and Ghana, the countries together responsible for two-thirds of the world’s cocoa beans. Both countries have been struggling with extreme weather changes and cocoa pod diseases for months. Shipments of cocoa from Cote d’Ivoire were down by roughly 39% from the previous year over the period of October 2023 to February 2024, at 1.04 million metric tons, Euronews reported. Exports from Ghana also plunged by some 35% to 341,000 metric tons during the period of September 2023 through January 2024. A Reuters cocoa poll last week projected the global cocoa bean deficit reaching 375,000 tons in the current agricultural season. Industry analysts note that bean costs are likely to keep growing due to the threat to global supply posed by the weather phenomenon El Nino, which caused draughts in West Africa during the third quarter of 2023, and is expected to continue at least until April.

Chocolate manufacturers have been warning that rising cocoa bean costs may force them to pass on the changes to consumers. On an earnings call on Thursday, the CEO of US candy giant Hershey, Michele Buck, said she expects “historic cocoa prices” to limit earnings growth in 2024 and translate into price rises on products. “We will be using every tool in our toolbox, including pricing, as a way to manage the business,” Buck stated. The company Mondelez, the owner of candy maker Cadbury, last month also warned that it would be hiking prices as a “last resort” to manage costs. Earlier this week, the head of the European Cocoa Association, Paul Davis, warned that the global cocoa market is likely to remain tight for another 18 months to three years. “We’ve got headwinds all over the place at the moment. Very expensive fertilizers, tough conditions for farmers, tough conditions for consumers… We are in a very tight balance. There is no cavalry that’s coming to the rescue,” he stated, as cited by the Business Insider.  Chinese investors and households were major gold consumers in 2023 amid strong global demand for the safe-haven metal, the World Gold Council’s quarterly report has shown.

According to the publication, Chinese investment demand for gold – spanning bars and coins – jumped 28% last year to 280 tons. Jewelry consumption was also up 10% to 630 tons. Overall, gold purchases reached nearly 960 tons in 2023. “China was key to a lot of what was happening last year,” said Louise Street, senior market analyst at the WGC. “When you look at the consumer sector, China is not the price-setting factor but it is providing a floor.” The world’s second-biggest consumer, India, saw total gold purchases slide to 748 tons in 2023. It was followed by the US (249 tons), Türkiye (201.6 tons), and Iran (71.8 tons). The top ten also included Russia, Germany, Egypt, Vietnam, and Saudi Arabia. The report indicated that together with “blistering” demand from global central banks, Chinese consumer demand helped push the yellow metal’s price to record highs in December and keep it above $2,000 per troy ounce this year. According to the WGC, total worldwide gold demand in 2023 was the highest on record at 4,899 tons, with annual bar and coin investment seeing a mild contraction and annual jewelry consumption holding steady at 2,093 tons.  Gold Gains Amidst Fed Rate Cut Prospects Gold (XAU/USD) prices are inching higher on Wednesday. The precious metal has remained consistently above the crucial $2,000 level for a week, buoyed by the anticipation of interest rate cuts from the Federal Reserve next year. This sentiment is further fueled by the Fed’s recent signals indicating a possible end to its tightening phase and a shift towards rate reductions in 2024. Treasury Yields and US Dollar Response The prospect of these rate cuts has rippled through financial markets, notably impacting U.S. Treasury yields. The 10-year yield has retreated, aligning with the Fed’s unexpectedly dovish pivot. Concurrently, the U.S. dollar is experiencing a slump against major currencies, trading lower as markets bet on imminent rate cuts. This weakening of the dollar has been a contributing factor to the gold market’s current trajectory. Global Inflation and Monetary Policies The global inflation landscape is also influencing market sentiments. The U.K., for instance, reported a more significant than expected drop in inflation, reaching its lowest annual rate since September 2021. This decline has implications for the Bank of England’s monetary policy, which maintained a hawkish stance in its last meeting, emphasizing the need for a restrictive policy for an extended period. Short-Term Market Outlook In the short term, the market outlook appears cautiously optimistic for gold. The combination of a weakening dollar, declining Treasury yields, and shifting global inflation rates presents a favorable environment for gold prices. Investors, however, remain vigilant, awaiting the U.S. November PCE index report, which will offer further insight into the inflation trajectory and potentially influence the Fed’s policy decisions in the upcoming year. Technical Analysis  Gold (XAU/USD) is currently trading at 2044.90, positioned above both its 200-day moving average of 1957.36 and 50-day moving average of 1989.19. This indicates a generally bullish trend. The price is hovering between the minor support at 2009.00 and minor resistance at 2067.00, suggesting a potential consolidation phase. However, it remains below the main resistance level of 2149.00. Given its stance above key moving averages and near minor resistance, the market sentiment for gold appears cautiously bullish. Investors might watch for a breakout above the minor resistance to confirm a stronger bullish trend, or a pullback towards the main support for potential buying opportunities.

Central banks have continued their gold buying spree, with reported net monthly purchases totaling 42 tons in October, the World Gold Council (WGC) has revealed.

According to a report published last week, the figure was 41% lower than September’s revised total of 72 tons, but still 23% above the January-September monthly average of 34 tons. The People’s Bank of China (PBoC) remained the largest bullion buyer, reporting purchases of 23 tons of gold in the 12th consecutive monthly addition to its reserves. This reportedly brings the PBoC’s net purchases to 204 tons during 2023, with its overall reserves amounting to 2,215 tons. “Despite the significant increase, reported gold reserves still account for just 4% of the bank’s total international reserves,” the WGC wrote. The Central Bank of Türkiye also made a significant purchase during the month, buying 19 tons to increase its official gold reserves (central bank plus Treasury holdings) to 498 tons. Beyond these two banks, buying was more modest, the report noted. The National Bank of Poland reportedly continued adding to its gold stockpile, buying another six tons. Its holdings of the yellow metal have now risen by over 100 tons this year, to 340 tons in total. The Reserve Bank of India, the Czech National Bank, the National Bank of the Kyrgyz Republic, and the Qatar Central Bank were the other significant buyers in October. The report also noted that central bank gold purchases have heavily outweighed sales of the metal so far this year. “Even before October’s net buying, we noted that 2023 was likely to be another colossal year of central bank buying. Having started Q4 positively, this year’s central bank demand looks set to climb even higher,”  With less than 20 trading days left until the end of 2023, we have just witnessed a series of record-breaking price developments in the international gold price, as well as heightened gold price volatility, and the price moving in a $120 range intraday.

While a new all-time high monthly close in the US dollar gold price was achieved on Thursday 30 November at $2040/oz, and new all-time highs on the weekly close and daily close were achieved on Friday 01 December at $2072/oz, these new record highs were in hindsight, overshadowed by what happened subsequently. For following the weekend pause of Saturday and Sunday (when gold market venues around the world are closed,) the gold market re-opened into the new trading week with a shock and awe surge to $2143, the speed and magnitude of which has not been seen for many years. As the gold market opened at 6 pm New York time on Sunday 3 December (11 pm Sunday London time, 7 am Monday morning Singapore / Shanghai time), this price surge began to take shape a mere 15 minutes after opening, with the gold price blasting up by $70 from $2073 to $2143 in a little over 20 minutes – that’s a 3.38% surge in the gold price in a mere 20 minutes – shattering all resistance levels in a flash, and breaking through the psychologically important $2100 level. Equally spectacularly, after this price spike to $2143, the gold price went down again, as first violently, and then over the next 12 hours in a very controlled fashion. For the record, here are the details, using New York times as the reference point. Note that the ‘gold market’ opens on Sunday evening New York time when the CME’s Globex electronic trading platform opens for gold futures trading. This is a time of relatively low liquidity as none of the world’s major gold markets are officially ‘at their desks’, although its just before the Shanghai Gold Exchange (SGE) begins trading. Starting at 6:15 pm New York time on Sunday evening, the spot gold price rose over a 5 minute period from $2074 to $2088. Between 6:19 pm and 6:24 pm, the price then rose again from $2088 to $2112. Then between 6:24 pm and 6:29 pm, the price increased again from $2112 to $2124. Finally, between 6:29 pm and 6:34 pm, the gold price accelerated even further from $2124 to $2143.37. To reiterate, that was a $70 surge in a 20-minute period.  Oil prices began to retreat on Thursday afternoon as it became clear that OPEC+ members were agreeing to voluntary cuts beginning in the new year, and that those cuts would be announced only by each member country instead of by the group as a whole.

OPEC+ announced during the full OPEC+ meeting on Thursday that because all the cuts agreed to today were voluntary, they would be announced not by the group, but by the individual member states. Immediately following the meeting’s kickoff, it was also announced that Brazil would join the OPEC+ group effective in January. Three weeks ago, OPEC’s Secretary General HE Haitham al-Ghais said that the group’s door was open should Brazil wish to join. Brazil has a goal of substantially increasing its crude oil production to become the world’s fourth-largest producer by 2030. In September, Brazil exported $3.92 billion in crude oil, while importing $681 million, according to OEC data. This level of exports is a 13% increase year over year, with China as the primary destination. Brent crude oil prices, which had been trading up around 1.5% during the JMMC meeting, sank to +0.16% on the day in the absence of an announced production strategy from the group’s leadership. WTI slipped into the red with a loss of 3.43% on the day following the full meeting. The specifics of what was agreed to for the first quarter of 2024 among the OPEC+ members:

Angola not only didn’t announce an additional voluntary cut, but it publicly rejected its current quota, and reiterated its proposal for a 1.18 million barrel quota beginning in January. It added that it will not stick to the new OPEC quota. Not including cut extensions from Saudi Arabia and Russia, the additional voluntary cuts beginning in January and carrying through to the end of March is 684,000 bpd. All together, the total voluntary cuts for the first quarter is 2.184 million bpd. The next OPEC+ meeting is scheduled for June 1, 2024.  Gold prices could soon reach a record $2,500 per ounce, driven by safe-haven investor demand in the wake of global uncertainty and geopolitical tensions, some analysts are now projecting.

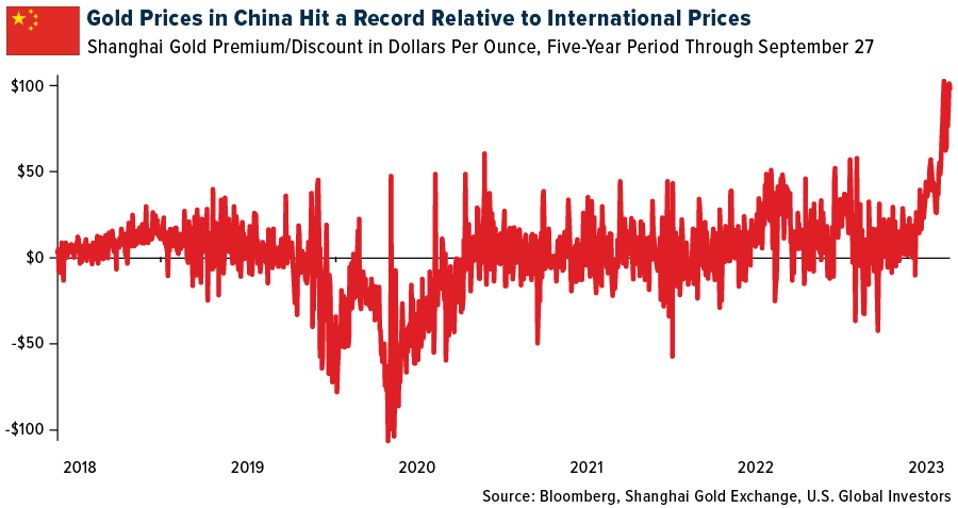

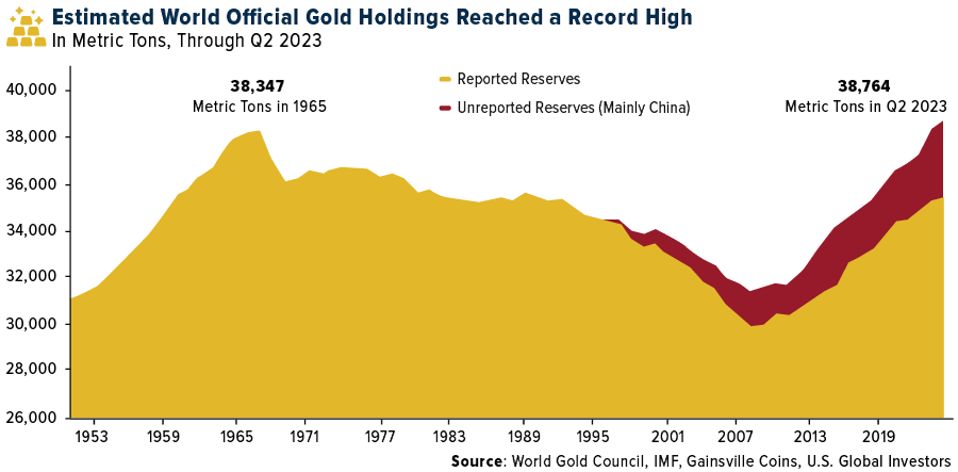

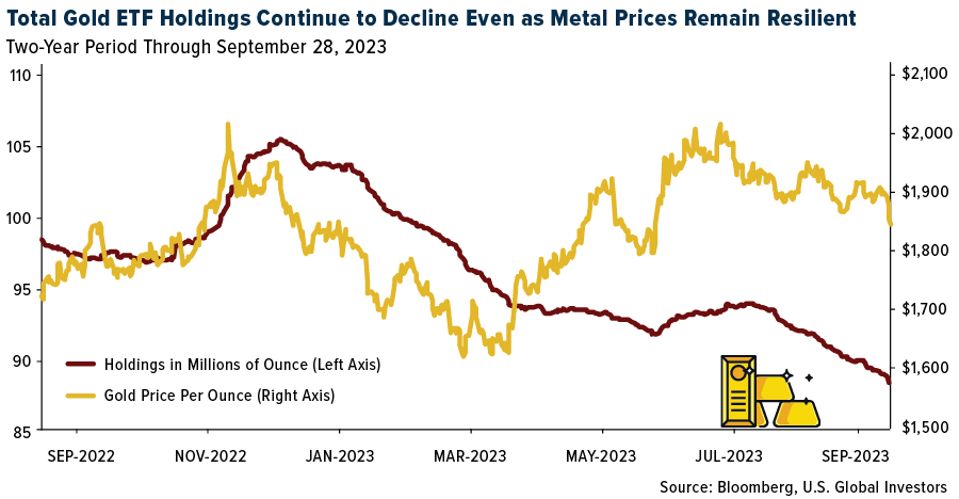

Futures have risen 3% in the past couple of weeks, briefly breaching the key psychological threshold of $2,000 per ounce on Tuesday. The rise marked the highest daily close so far this month, and any move above $2,006.37 per ounce this week would make it the highest weekly close since the spring, researcher Fundstrat’s technical analyst Mark Newton wrote in a note on Wednesday seen by Business Insider. “This is quite positive technically, and I expect that gold has begun its push back to new all-time highs,” wrote Newton. He believes a rise past $2,009.41 per ounce should lead to gold entering the $2,060-2,080 range. Newton told Business Insider that a breach of resistance at $2,080 would signal a “definite technical breakout,” which he expects to quickly drive gold even higher. “My technical target for gold is $2,500/oz, and it looks appealing to be long precious metals given falling real rates, rising cycles and ongoing geopolitical conflict,” he said. The analyst later clarified that his timeline for $2,500 isn't necessarily for the end of the year but is an “intermediate target.” Bullion has been rallying since the attack by Palestinian armed group Hamas on Israel on October 7. Experts and traders expect the escalation and uncertainty in the Middle East to continue driving gold prices higher. Investors traditionally turn to gold in times of market uncertainty to hedge risks and as a store of value. Bullion has been seen as a safe haven during periods of economic instability, stock market crises, military conflicts, and pandemics.  The Chinese yuan has lost nearly 6% of its value against the U.S. dollar this year, while Shanghai-listed stocks are off about 8% from their 2023 high, set back in May. There’s an ongoing property crisis, with shares of Evergrande Group—China’s second-largest property developer and the world’s most indebted—halting trading last Thursday after its founder and chairman was reportedly taken into police custody for unknown reasons. Against this backdrop, gold has emerged as a preferred investment alternative, acting as a hedge against financial volatility. Gold prices in China have soared as a result, hitting a historic relative high with a more than $100 premium per ounce over metal prices in New York or London, according to Bloomberg. Data showing a 40% hike in withdrawals from the Shanghai Gold Exchange and a 15% increase in imports in August further underscore this trend.  Gold prices in China hit a record relative to international prices Looking ahead, analysts predict sustained demand for the yellow metal amid not just a depreciating yuan and shaky real estate market but also falling bond yields. The gold buying spree appears to represent an investment move—sales of bars and coins are up 30% compared to last year—but rising prices are also tempting jewelry buyers to make early purchases ahead of the busy Lunar New Year buying season. Official Gold Reserves At A New Record High?It’s not just China’s retail investors. The People’s Bank of China also continues to diversify its reserves with gold, so much so that one expert believes total official gold holdings by central banks have touched a new all-time high. Jan Nieuwenhuijs, writing for Gainesville Coins, estimates that global gold reserves peaked at 38,764 metric tons in June, surpassing the previous 1965 record by as much as 400 tons.  Estimated world official gold holdings reached a record high Nieuwenhuijs’s estimate, which accounts for unreported purchases unlike the International Monetary Fund’s (IMF) calculations, shows a notable increase in gold holdings since the 2008 financial crisis, as you can see in the chart below. This reflects what he calls a “desire by central banks the world over to diversify away from the U.S. dollar with its ever more evident counterparty risks.”  Total gold ETF holdings continue to decline even as metal prices remain resilient Costco—Yes, That Costco—Is Selling Out Of Gold Bars. Why Not Gold ETFs? Costco has recently added one-ounce gold bars to its online inventory, selling out within hours of restocking. According to CNBC, the retail behemoth offers bars from South Africa’s Rand Refinery and Swiss supplier PAMP Suisse, at prices slightly below the market rate of around $1,900. The offer is available only to the company’s 66 million paying members, creating an exclusive buying opportunity. During the most recent earnings call, Costco CFO Richard Galanti said that the gold bars were selling like hotcakes, commenting that as soon as they’re listed on the company’s website, “they’re typically gone within a few hours, and we limit two per member.” Interestingly, the enthusiastic demand from Costco buyers contrasts significantly with dwindling holdings found in total known physical gold-backed ETFs. As I shared with you recently, holdings have continued to decline since June—and, before that, since April 2022—even as the price of the yellow metal has held up admirably against a strong U.S. dollar and sky-high bond yields. Last week, the price of gold dipped below $1,900 for the first time since August, but if Treasury yields continue to soar through October, it could discourage casual gold investors, potentially driving prices down toward the $1,800 mark. But then, the last time yields were this high—in September 2007—gold was trading at around $750. So again, the metal has been remarkably resilient in a very challenging monetary environment.

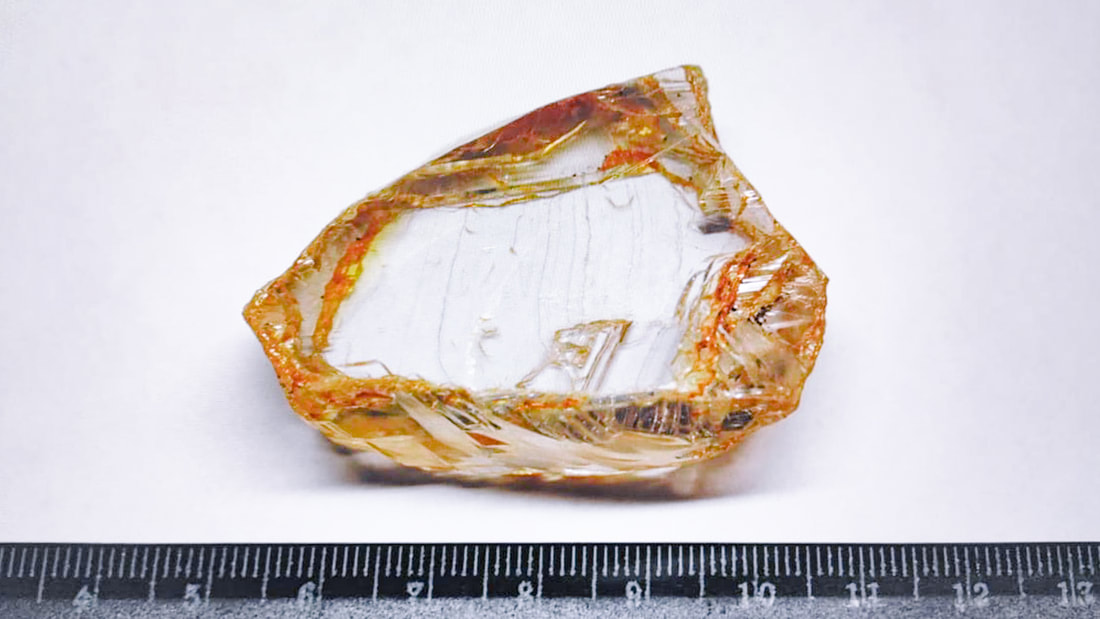

The diamond conglomerate Alrosa announced on Monday the discovery of the largest diamond in Russia in the past decade. The gem came from a mine in the Anabar district of the Republic of Sakha, also known as Yakutia.

“Experts have yet to study in detail and evaluate the potential and the characteristics of the mined diamond, but without a doubt, this is a record holder both for our company and for the country’s diamond industry,” said Alrosa General Director Pavel Marinychev, calling the find “an excellent finale to the 2023 mining season.” The diamond is 390.7 carats in size and was discovered on September 9 by the Anabar Diamonds company, an Alrosa subsidiary operating the Mayat mine in northeastern Siberia. According to Alrosa, the find happened during the night-time washing of the diamond-bearing sands. A photo posted by Alrosa shows a crystal with an irregular shape and a yellow-brownish halo, which is a very rare combination. The yet-unnamed gem is slightly smaller than the 401-carat diamond found in 2013.Another diamond found in the same batch is a 37.7-carat gem with the classic octahedral shape, Alrosa said. Both have been sent to morphologists for evaluation. Alrosa is the world’s largest diamond producer, accounting for 30% of the $80 billion annual global trade in rough precious stones. It mines the alluvial deposits in Russia’s Arctic, both in Yakutia and Arkhangelsk Region. The work is limited by harsh climate conditions, but accounts for four percent of the world’s production of diamonds in the rough.  The issue of the creation of a BRICS reserve currency has taken on particular significance in recent months after President Putin declared that the creation of such a currency was in the process of discussion. This was followed by a series of statements coming from Russia’s legislative branch on the expediency of creating a new reserve currency — most recently from the Federation Assembly speaker Valentina Matvienko. While the debate on the possibility of creating such a reserve currency is only starting in Russia and more broadly across the global economy, the implications of such a move on the part of the BRICS could have transformational consequences for the global financial system.

Initially, the proposal to create a new reserve currency based on a basket of currencies of BRICS countries was formulated by the Valdai Club back in 2018 — the idea was to create an SDR-type currency basket composed of BRICS countries’ national currencies as well as potentially some of the other currencies of BRICS+ circle economies. The choice of BRICS national currencies was due to the fact that these were the among the most liquid currencies across emerging markets. The name for the new reserve currency — R5 or R5+ — was based on the first letters of the BRICS currencies all of which begin with the letter R (real, ruble, rupee, renminbi, rand). The recent debates concerning the prospects for the creation of a new reserve currency focused more on the risks, fragilities and outright impossibility of the R5 project. Less attention has been accorded to estimating the benefits (including in terms of hard figures) to BRICS economies and EM more generally. There has also been scant attention with respect to the actual modalities of launching the BRICS reserve currency. What is clear at this stage is that the BRICS reserve currency will not be created to replace the national reserve currencies of the BRICS economies — rather it will complement these national currencies and will serve to improve the possibilities for more EM currencies to attain reserve status. Accordingly, the attainment of high trading shares among the BRICS economies is a desirable but not altogether an indispensable condition for launching the new reserve currency. In fact, the new BRICS currency does not have to service all trade transactions among BRICS economies in the very near term. Initially, the new BRICS currency could perform the role of an accounting unit to facilitate transactions in national currencies. In the longer run, the R5 BRICS currency could start to perform the role of settlements/payments as well as the store of value/reserves for the central banks of emerging market economies. Within the composition of the R5 currency basket the share of the Chinese renminbi may be initially set at a relatively high level in order to take advantage of the already advanced reserve status of the Chinese currency. This share may be reduced progressively in stages later on along with the inclusion of new EM national currencies. Outside of the BRICS economies some of the potential candidates that with time could be included into the R5+ currency basket may feature the Singaporean dollar or the UAE’s dirham. One of the potential risks associated with the use of EM currencies in reserves is their high volatility. The basket mechanism of the BRICS reserve currency will allow for reducing some of this volatility via averaging out the exchange rate dynamics of currencies that follow different market trends — if the currencies of Russia, South Africa and Brazil follow the commodity cycle, the opposite is true with respect to commodity importers such as India and China. Importantly, the scope for employing the new reserve currency in the world economy is sizeable given the tremendous potential for de-dollarization. The new BRICS reserve currency can act in concert with the stronger role performed by BRICS national currencies to take on a greater share of the total pie of currency transactions in the world economy. This greater role can be gradually extended from servicing foreign trade transactions to investment flows across the developing world. In line with the original R5 concept developed by Valdai Club in 2018 one of the possible venues for boosting the use of national currencies and the BRICS reserve currency could be the creation of a platform for regional development banks in which BRICS economies are members. Such a platform could develop a portfolio of common/integration projects that may be financed in national currencies. In the end, the launching of a new reserve currency if successful will impart a transformational effect on the international financial system. The Central Banks in the global economy are experiencing a notable shortage of reserve currencies in managing their reserve holdings. In this respect, the emergence of additional reserve currencies from among the EM economies will serve to expand the possibilities for diversifying reserve holdings and reducing the vulnerabilities associated with the dependence on a narrow range of currencies. The R5 project can thus become one of the most important contributions of emerging markets to building a more secure international financial system.  Ghana’s government is working on a new policy to buy oil products with gold rather than US dollar reserves, Vice President Mahamudu Bawumia has said on Facebook. The move, announced on Thursday, is meant to tackle dwindling foreign currency reserves coupled with demand for dollars by oil importers, which is weakening the local cedi and increasing living costs. Ghana’s Gross International Reserves stood at around $6.6bn at the end of September 2022, equating to less than three months of imports cover. That is down from around $9.7bn at the end of last year, according to the government. If implemented as planned for the first quarter of 2023, the new policy “will fundamentally change our balance of payments and significantly reduce the persistent depreciation of our currency”, Bawumia said.

Using gold would prevent the exchange rate from directly impacting fuel or utility prices as domestic sellers would no longer need foreign exchange to import oil products, he explained. “The barter of gold for oil represents a major structural change,” he added. The proposed policy is uncommon. While countries sometimes trade oil for other goods or commodities, such deals typically involve an oil-producing nation receiving non-oil goods rather than the opposite. Ghana produces crude oil, but it has relied on imports for refined oil products since its only refinery shut down after an explosion in 2017. Bawumia’s announcement was posted as Finance Minister Ken Ofori-Atta announced measures to cut spending and boost revenues in a bid to tackle a spiralling debt crisis. In a 2023 budget presentation to parliament on Thursday, Ofori-Atta warned that the West African nation was at high risk of debt distress and that the cedi’s depreciation was seriously affecting Ghana’s ability to manage its public debt. The government is negotiating a relief package with the International Monetary Fund as the cocoa, gold and oil-producing nation faces its worst economic crisis in a generation.  Oil tanker at a port terminal operated by China Petrochemical Corporation (Sinopec Group) in Zhoushan, Zhejiang Province, China Both LNG and oil deliveries have surged since the start of the year, Chinese customs data shows. Russian shipments of gas and oil to China grew significantly over January-October of this year compared to the same period in 2021, China’s General Administration of Customs reported on Sunday.

According to its data, liquefied natural gas (LNG) deliveries jumped by 32% in annual terms, to 4.98 million tons. In dollar terms, the increase was 157% and exceeded $5.3 billion. Russia is currently China’s fourth-largest LNG supplier after Australia, Qatar, and Malaysia. While data shows that China’s imports of the fuel from Qatar also grew over the first ten months of the year, shipments from both Australia and Malaysia have been dropping. While the customs agency does not currently list the physical volume of China’s pipeline gas imports, its data shows that the value of pipeline gas flows from Russia in January-October 2022 soared by 182% compared to the same period in 2021, to $3.1 billion. This makes Russia the second largest supplier of pipeline gas to the Asian nation after Turkmenistan ($8.23 billion). China’s oil imports from Russia also surged over this period, rising by about 9.5% to 71.97 million tons. Deliveries were up 53% to $49.19 billion in dollar terms. As follows from the published data, in both October and September Russia was China’s second largest oil supplier. Saudi Arabia remains the leader, having sold 73.76 million tons of the fuel to China for $55.5 billion over January-October. China has been boosting energy imports from Russia, having taken advantage of discounts Moscow offered earlier this year in an attempt to secure buyers for Russian oil and gas. This came as many traditional importers began shunning supplies from the country amid Ukraine-related Western sanctions.  The Argentine foreign ministry has confirmed that Chinese mining company Tibet Summit Resources will invest $2.2 billion in two lithium exploration projects in the South American country. The Shanghai-based company is expected to create around 10,000 jobs in Argentina, according to the statement released on Friday. The ministry noted that the plans were shared by Jianrong Huang, the president of Tibet Summit Resources, with Argentine ambassador Sabino Vaca Narvaja at the China International Import Expo in Shanghai. Under the plan, the Chinese firm will invest around $700 million into the Salar de Diablillos project in Salta province, which is expected to produce 50,000 tons of battery-grade lithium carbonate starting next year. Meanwhile, another $1.5 billion will be used for construction of a plant at the Arizaro salt flat, also located in Salta, which is expected to produce between 50,000 and 100,000 tons of lithium carbonate by 2024.

Argentina, along with Bolivia and Chile, is part of the Lithium Triangle, a region of the Andes that accounts for around 54% of the world’s white metal reserves. Globally, the South American nation is ranked the fourth biggest lithium producer, after Australia, Chile and China, according to a report from the Argentine Chamber of Mining Entrepreneurs (CAEM). |

Thank you for choosing to make a difference through your donation. We appreciate your support.

Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed